A Generational Opportunity In The Energy Sector

It is not often you come across a sector that is cheap, has a favourable fundamental and macro backdrop whilst also looking attractive from a technical perspective.

Energy companies are highly cyclical and volatile. They tend to trade largely as a group and are effectively a leveraged play on the price of oil, similar to gold miners and gold. Within the sector itself, there are various subsectors defining the activities in which the energy companies engage. The exploration and production companies are involved in pumping the oil and gas from the ground, with ConocoPhillips, Phillips 66, EOG Resources and Marathon Petroleum being the largest companies who engage in such activities. The exploration and production companies tend to be the most sensitive to the price of oil relative to the refiners, transportation and integrated companies.

From a valuation perspective, the sector is cheap on both a relative and absolute basis. Within the S&P 500, the sector it trading at a 10-year cyclically adjusted P/E (Shiller P/E) ratio of just 11.7. This is relative to 32.3 for the S&P 500 as a whole. There is plenty of evidence to suggest energy would have a decent chance of outperforming the market on this metric alone.

On a relative basis, not only is energy exceedingly cheaper than any other sector, the sector itself now has the smallest weighting of any in the S&P 500, with Exxon Mobil’s market cap roughly equal to that of Zoom, even though the former is generating revenue 400x compared to the latter. This is a far cry from peak oil prices in the 1980s when energy was the largest sector within the S&P 500.

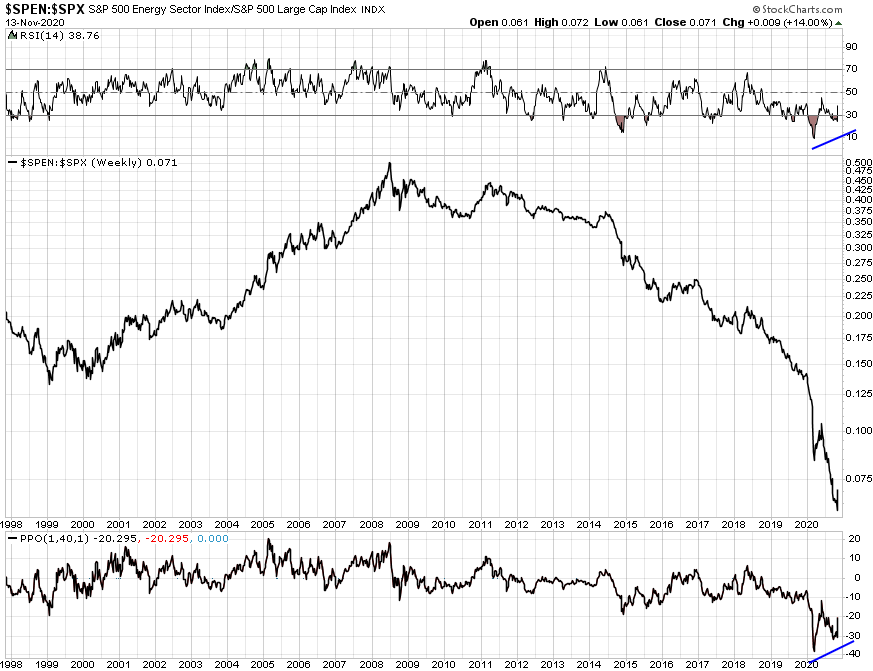

Source: StockCharts.com

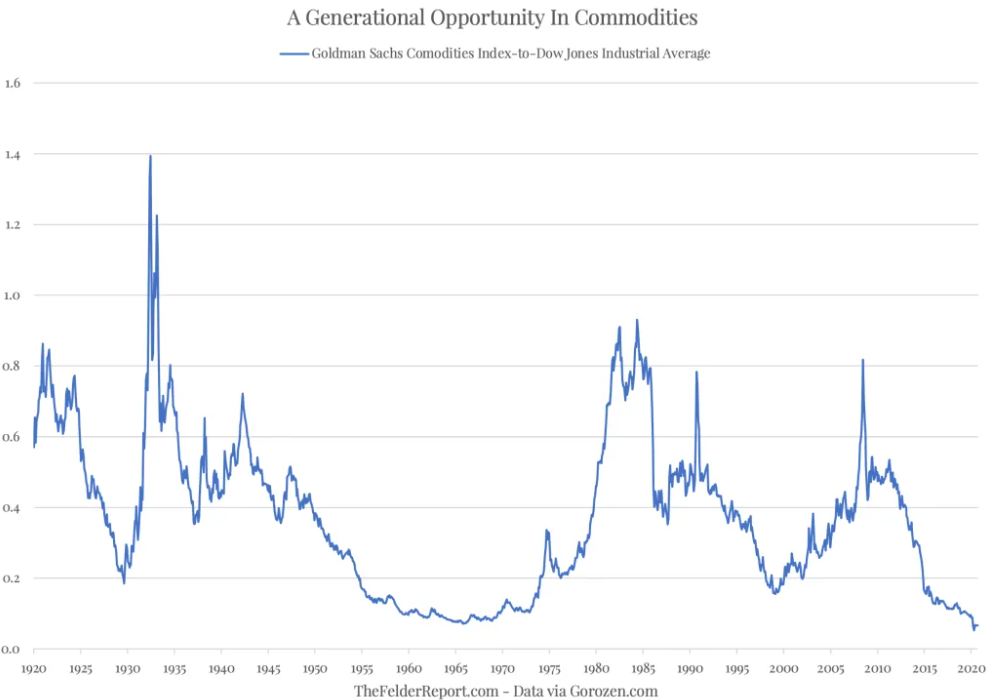

Commodities as a whole may have never been this cheap relative to financial assets, with energy companies being the epitome of this group. Such times throughout history presented excellent opportunities going forward.

The energy companies are indeed incredibly cheap. As a proxy, the largest integrated oil companies and largest exploration and production (E&P) companies are all trading at a Price-to-Tangible Book Value of less than ~1.5.

Source: Koyfin.com

Again, energy companies are cheap. Very cheap.

Furthermore, in a world where 10-year US treasuries are yielding 0.88% and 90% of the world’s government bond are trading at yields lower than 1%, the energy sector is offering terrific value in this regard with the spread between the energy sector dividend yield and US 10-year treasuries reaching record levels.

The XLE energy sector ETF itself is yielding roughly 12%, with Exxon Mobil yielding 9% and Chevron 6%. For yield starved investors there is plenty to like here.

From a fundamental perspective, energy stocks have been hammered this year, which given the extreme fall in demand for oil and its excess capacity comes as no surprise. However, during such times comes opportunity. Not only have many energy companies declared bankruptcy through this period, but the survivors and industry leaders have been forced to make significant changes to their business strategies in order to survive. They have been forced to become disciplined in how they allocate capital, only funding investments and capital expenditures with internally generated cash and a lesser reliance on external debt. This move to responsible capital allocation has been forced upon the industry in a way that capitalism is supposed to function. Likewise, as the industry becomes starved of external capital, the companies have undergone a painful process of depleting reserves and employee layoffs in order to stay solvent. As a result, the energy sector has become one of the few sectors independent of central bank manipulation and bailouts and thus undergone a thorough cleansing process.

Although painful, the sector has been able to fail and restructure, setting it up to capitalise on rising oil prices going forward in the most efficient and beneficial way possible.

One thing for certain is oil prices at their current levels are unsustainable. Whilst they may remain at these levels for the near to medium term, such prices are below the breakeven levels of the major oil producers, and thus cannot remain at these levels forever.

Given the current industry fundamentals, oil prices going forward will eventually have to rise. The excess supply of oil inventories during the first half of 2020 is beginning to subside, with the rig count in the US alone falling by approximately 75% in 2020 according to Leigh Goehring. Future supply will also continue to be impacted by the large retrenchment in drilling activity that has taken place.

Source: US Crude Oil Inventories - Investing.com

This move to a reduced supply of oil means that when demand eventually comes back online - largely contingent on lockdowns and travel restrictions around the world - we are likely to see prices rise significantly to levels sustainable for the oil producers at a minimum. Current (and future) supply will be insufficient to meet the increasing demand.

To illustrate how cheap oil has become, the gold to oil ratio has historically been a reliable indicator.

Over the past 150+ years, nearly every time the above reading has reached an extreme ratio (i.e. gold is incredibly expensive relative to oil), oil has risen dramatically in price and the ratio has thus fallen. If history is any guide then oil prices are set to rise over the coming years. What’s more, we now have a central bank who is committed to creating inflation my any means necessary. Due to their extremely low valuations, energy stocks are likely the best way to obtain any inflation protection going forward and capitalise on the next energy bull market.

The consensus view toward energy will tell you that as demand comes back on line, supply will easily match demand. Likewise, the bears will tell you that that oil’s structural demand going forward is only going to decline, driven by the ESG movement and increasing adoption of electric vehicles. Whilst this may be true over the long-term, we are a long way from living in a world of electric only vehicles and clean energy. Likewise, whilst the demand for oil in developed nations may be near its structural peak, demand in emerging economies will only continue to grow alongside their GDP’s. China has been the posterchild of this phenomenon over recent decades, with India being the next enormous economy to follow suit. Before electric vehicles and renewable energy do eventually take over, oil demand will continue to defy the bears.

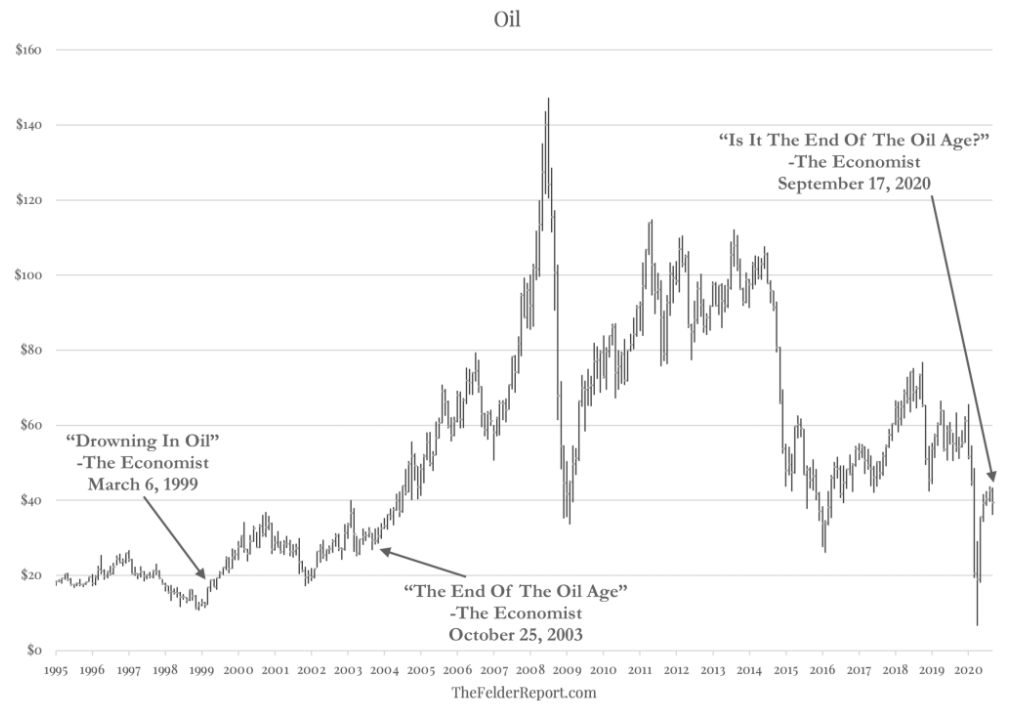

Energy and oil are very much the most hated assets on the planet at present. Sentiment is clearly more negative towards the energy sector than perhaps at any point throughout history. For the contrarian and long term investor, this backdrop represents a potentially generational buying opportunity. Jesse Felder summed this up perfectly in a recent post, noting how The Economist’s latest proclamation of the death of oil is reminiscent of such statements made in the late 1990s and early 2000s before the oil price would rise nearly sevenfold over the next decade.

The sector being labeled as “uninvestible” is akin to similar statements made about gold and gold related equities during the mid-2010s. Gold and gold related equities have gone on to significantly outperform the broad market since.

We can see this bearish sentiment towards the sector by also looking at how the energy equities have diverged negatively from the price of oil over the past several months, indicating how investors continue to want nothing to do with energy stocks even though oil itself has remained relatively stable.

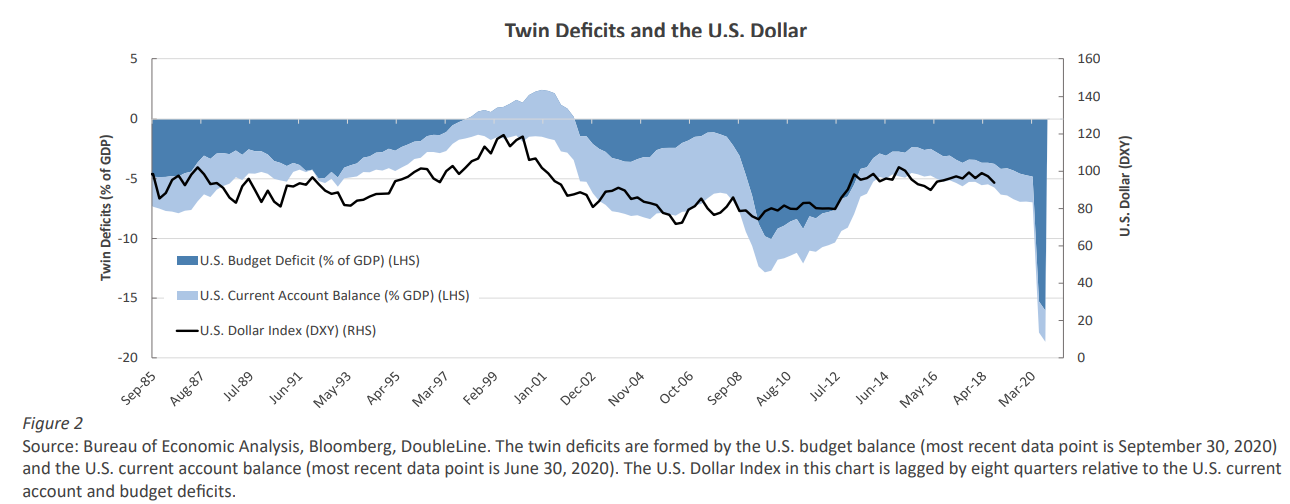

If we are going to see rising oil prices over the coming years, we would need to see a cyclical decline in the dollar as the two trade in an inverse manner over the long term. While my short-term expectation for the dollar is likely higher, this is primarily a function of the extreme negative sentiment towards it and the artificial demand for Eurodollars which would both likely need to resolve themselves (at least to some extent) before we see the dollar decline significantly.

Over the long-term, I am very much expecting at least a cyclical decline in the dollar. Whether it is set to lose its reserve currency status is unlikely anytime soon (a topic for a whole different conversation), I would expect to see at least some weakness in the dollar over the next five or so years as the bearish long-term case for the dollar has perhaps never been greater.

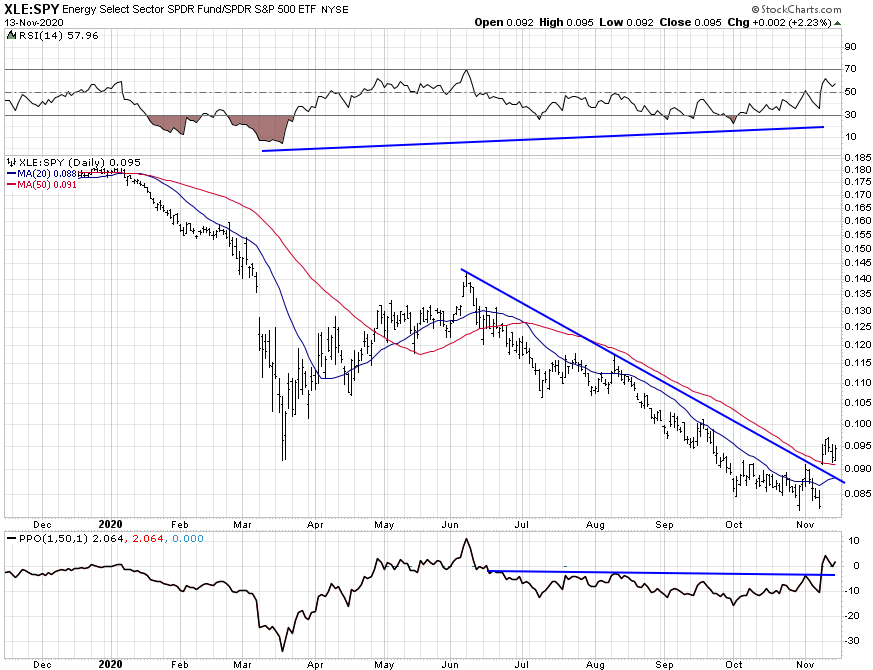

From a purely technical perspective, there are positive signs on both the longer term (pictured earlier) and shorter term charts, both on an absolute basis and relative to the S&P 500.

Firstly, relative to the broad market energy looks to potentially be readying for a reversal in trend. We are beginning to see strong long-term bullish divergences in RSI and money flow, along with monthly DeMark 9 and 13 sequential buy signals (which we are also seeing on the weekly and daily charts).

Source: TradingView.com

Indeed, the downtrend exhaustion looks to be even more pronounced on the daily chart, where we are also seeing bullish divergences in both RSI and momentum (as measured by price relative to its 50-day moving average), along with a breakout on the downtrend line which has been tested a number of times over recent months.

Looking at the sector on an absolute basis, the daily chart is showing a similar breakout of the downtrend line with bullish divergences in momentum and RSI.

On a longer term scale, there is a decent support level around the current levels dating back to the early 2000s. It would be difficult to see the sector falling much further from here.

In summary, it is not often that such an opportunity presents itself whereby the fundamentals, sentiment, technicals and macro variables all line up favourably. The energy sector may be offering an opportunity that only presents itself once in a generation. For me, the best way to take advantage of this is via the oil exploration and producers which as a group generally have the highest upside during an energy bull market.

The XOP and IEO ETF’s are cost effective ways to gain exposure to these companies. My preference would be to favour XOP, given its equal weighting constitution and thus has a higher weighting to the smaller companies in the sector. However, given I am an Australian based investor, investing is an ETF such as XOP would expose me to currency risk, which if oil is set to rise then the USD will need to fall., and subsequent rise in the AUD relative to the USD would eat into my potential returns. The FUEL ETF, which trades on the ASX, provides me with a on option to invest in the broad global energy sector, while hedging the currency back to AUD. As a result, I will likely split my allocations to the sector between XOP and FUEL to obtain a hedged and unhedged exposure. I may actively manage my currency risk on top of this too if deemed necessary.

I am still waiting for the price to confirm a reversal of trend, and when I see favourable enough technical setups I will commence entering my positions, at which point I will update below.

One caveat I would like to flag regarding the investing in the sector is how the rise of passive investing which I have wrote about previously will impact its potential performance. As I discussed, given passive is very much a momentum biased strategy which works is a self-reinforcing manner, it creates a dynamic whereby a greater level of external capital is required to be allocated to undervalued and under-represented sectors in order to outperform. While in all likelihood this will have impact on the potential upside for the sector, this dynamic is more pronounced within systematic value strategies and their continued underperformance relative to momentum, as opposed to absolute value such as energy, which given the reasons detailed throughout this article will likely to very well over the next few years. An effective way to manage this dynamic would be to perhaps allocated to a cap-weighted energy ETF such as XLE, which is the broad energy sector ETF (or FUEL), as opposed to an equal weighted alternative such as XOP, or perhaps a combination of both, which is my preference.

Nonetheless, I expect the energy sector to perform very well over the coming years.

Update: 19 November 2020

I have added a small starter position roughly equal to 1% in both FUEL and XOP respectively. The recent rally in energy over the past week has come quick and fast, I will look to build on my holdings if/when we have a pullback.