It may be time to get tactical in precious metals

Updated 23 November 2020

After its peak in early August and a healthy consolidation period since, it appears as though gold may finally be breaking out and ready to resume its march higher.

Source: StockCharts.com

From a fundamental perspective the case for precious metals has only grown during this consolidation period and remains by favourite investment for the foreseeable future. Indeed, the short-term bullish case for gold seems to be turning favourable. Given the contested election in the US and the civil unrest likely to continue as a consequence, it ought to be no surprise the breakout has occurred at such a time. Unless either presidential candidate were to concede defeat in the coming days (unlikely), the probable outcome of such events should be very bullish for gold over the coming months and could be the catalyst to propel gold on its next leg higher.

Likewise, the rising real rates headwind I have flagged in the past appears as though it may be weakening, if only for the short-term. With November’s core-CPI forecast to be around 1.8%, similar to October’s reading, unless nominal rates continue to rise (which I do not anticipate just yet), rising real rates may no longer be the headwind for gold they have been over the past few months. If real yields fall, no doubt implied real yields will follow suit and so too gold, silver and the miners.

Data source: St. Louis Fed, Investing.com

Focusing on nominal yields, the US 10-year looks poised to break lower, a scenario which would of course push real yields lower and is something I will be monitoring closely.

This would follow on from the recent breakdown lower seen in German yields, and would likely increase demand for US treasuries relative to German bunds given their yield differentials are back to their highest point since early March, a scenario that would push US yields lower.

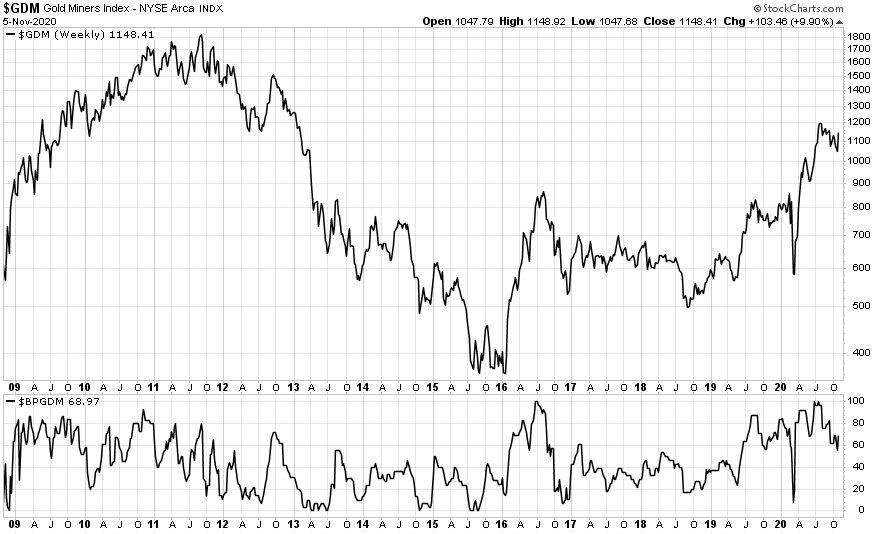

From a sentiment perspective - using the Gold Miners Bullish Percent index - looks to have been washed out to a level comparative to decent buying opportunities during the prior gold bull runs in 2009-2011 and 2016.

Likewise, if we look at commitment of traders data for money managers (made up of hedge funds and trend-following CTA’s), they currently have their smallest long position since early 2019. Money managers tend to be too long at the tops and too short at the bottoms, providing a fairly reliable sentiment indicator.

Source: BarChart.com

Whilst a further washout in sentiment would be ideal to get tactically overweight in precious metals, the long-term fundamental case at present is stronger than at any time during the 2000’s, and as a result unless we were to experience another extreme risk-off event in the like of what we experienced in February and March, a further washout in sentiment may be unlikely any time soon.

In summary, I will be monitoring the technicals closely for gold, silver and the miners, and if the breakout appears sustainable I will be looking to get tactically long, although I will retain my long USD position for the meantime as a hedge.

I will provide a update below should such events occur.

Update: 20 & 26 November 2020

I have added roughly 1% to the global miners (MNRS) ETF on the above dates. I will continue to update below as I progressively add to my exposure to the sector.

Update: 30 November 2020

As the sector begins to become oversold and considering we are seeing a full washout in sentiment, I have added another 1% exposure to the physical silver ETF. I will look to add more toward the aggressive junior minors and silver minors in the near term.

Update: 3 December 2020

Again, I have added another 1% of my portfolio to the GDXJ and SIL miners ETF’s. I am likely done adding to my positions for the time being.