Inflation May Become A Problem For Asset Markets Again In 2025

Summary & Key Takeaways:

Inflation remains above target on all measures.

Currently, Goods CPI is outright deflationary, while Shelter CPI and Services ex-Shelter CPI are declining slower than expected.

Most lead indicators of inflation are pointing to a slight increase over the coming three to six months. This will be primarily driven by Goods CPI. However, Services CPI should continue to trend lower, but at a slower pace.

The Fed has chosen to ignore above target inflation in favour of reducing the policy rate to help accomodate the growing federal deficit. While this is to be expected to continue for the most part over the coming decade, periods of above target and rising inflation will at some point force the Fed’s hand, if only for a short-term.

It seems this could be the case at some point in 2025. But don’t expect CPI above 3.5-4%, as that simply cannot occur with services inflation trending lower.

In isolation, this may be not a problem for asset market, but when stocks are priced to perfection and a significant easing cycle has been priced in, persistent upside surprise in inflation over the next six months may cause a temporary re-pricing of asset prices and monetary easing expectations.

Inflation remains above target

The current US inflation picture is largely the same has it has been for most of 2024. All primary inflation measures remain well above the Fed’s 2% target. And even though the sticky inflation measures have been trending down, the pace of deceleration is slowing.

Clearly, we are in a situation where an imminent decline to sub-2% inflation is highly unlikely. For that to occur the US economy requires a recession, something which appears unlikely in the near future.

If we look at the drivers of CPI in recent times, it has been a combination of outright Goods deflation, Shelter disinflation (which remains well above pre-COVID levels) and a reaccelerating in Services ex-Shelter inflation.

Services ex-Shelter inflation has been the primary drag on core inflation measures, as it reaccelerated from ~2.5% to ~5% in 2023 and 2024 and is still yet to move notably lower than 4.5%.

We can see these CPI drivers in further detail below. Quite clearly, Services inflation is moving lower at a modest pace, while the volatile Goods and Energy components have been largely deflationary for over 18 months now. Food CPI has been a non-factor since mid-2023.

Where should we expect CPI to move from here

As it stands, many investors and strategists are making calls at both ends of the inflation spectrum. Some expect the inflation decline to continue into 2025 to a comfortable level below the Fed 2% target. Others expect a material re-acceleration.

Both outcomes would have material impact on asset prices for very different reasons, but as I shall discuss, I suspect we end up somewhere in the middle come 2025, with a light bias toward the right tail. More specifically, inflation is not going to move notably lower than current levels and is likely to trend modestly higher from here, but not to an alarming degree. I suspect we will see Headline CPI moderate around the 3-3.5% level over the next six to 12 months.

When it comes to the lead indicators themselves, firstly, recent movements in the US dollar are pointing to an upward bias over the next three months or so, and neutral to down beyond that.

On the other hand, financial conditions are suggesting notable upward pressures on CPI are coming over the coming six months.

Manufacturing prices paid are relatively neutral.

Services prices paid are pointing to a sideways too slightly higher outlook. Importantly, neither are signalling a notable move lower.

Regional Fed prices paid surveys are suggesting upward inflation pressures are coming in the short-term.

As are commodity prices, though not to a significant degree.

Small business price plans favour a neutral outlook over the short-term.

While my composite lead indicator and forecasts are pointing to sideways too slightly higher inflation pressures over the next three months.

As we can see, many short-term to medium-term lead indicators of overall inflation remain neutral too slightly higher. None are pointing to any notable decline in CPI, while none are conversely suggesting a significant rise in inflation.

What this means is we should expect Headline CPI to to trend in the 2.5-3.5% range over the next three to six months, particularly as inflation base effects are now more likely to bias inflation to the upside moving forward.

What’s more, as I shall explain, upside inflation pressures appear much more likely to be on a Headline basis than on a Core basis.

Goods inflation set to move higher

The primary driver of upside inflation pressures moving forward is likely to be Goods inflation, just as it has been a primary driver of disinflation in recent times.

At this stage, we aren’t likely to see any kind of post-COVID style spike in Goods inflation, but we should see Goods CPI trend toward 1-2% over the next six months, a far cry from the -1-2% deflation we have seen in Goods of late.

This is a dynamic to which the New York Fed’s Supply Chain Index is suggesting.

So too are the various regional Fed Delivery Time surveys.

Along with the ISM Delivery Time Index.

Food inflation is also on the rise

Upside pressures in Food CPI are also likely to persist over the coming six months. Food inflation has become a non-factor over the past 18 months, so renewed upside movements in Food CPI will result in upside pressures on overall Headline CPI, even though it only makes up 13.5% of the Headline basket.

There are a number of indicators suggesting this. Food Manufacturing PPI is one.

While the FAO’s Food Price Index is another.

Mixed signals on the energy front

From an Energy CPI perspective (6.6% of the Headline basket) we are seeing mixed signals.

Energy Services CPI (3.1% of Headline) has been a notable upside inflationary force over the past six months on the back of higher natural gas prices (on a rate-of-change basis). With YoY natural gas price growth stalling of late, we should expect to see Energy Services CPI however around the current ~4% level over the coming quarter or two, so Energy Services inflation will continue to be a positive driver over this time frame.

A colder than normal US winter could result in natural gas prices spiking further over the next quarter, but such things are very difficult to predict in advance and will be largely ignored by policy makers.

On the other hand, Energy Commodity CPI (3.5% of Headline) have been deflationary for some time now on the back of weaker crude oil prices and thus gasoline prices.

From a growth perspective, oil prices would need to move significantly lower from here (think sub-$60) for the YoY change in crude oil and gasoline prices to have any further material downside impact on Energy Commodity CPI. And, while I expect oil prices to be rangebound ($65-$85) in 2025, we are likely at the bottom of that range, which means Energy CPI asymmetry is skewed to the upside, though not too any outstanding degree.

As such, Energy CPI is probably set to move sideways overall over the next couple of quarters, and its overall impact on CPI likely to be minimal.

Question marks surround the outlook for Services inflation

As we saw earlier, Services CPI has proved the stickiest part of the inflation complex. This is through a combination of Shelter CPI (Rent and Owners’ Equivalent Rent) decelerating at a slower pace than many expected, along with Services ex-Shelter CPI reaccelerating higher for most of 2024, driven largely by rising Auto Insurance CPI.

Beginning with the former, Shelter CPI has always been the largest component of the CPI basket at around 36.5% (which itself is primarily made up of Owners’ Equivalent Rent (OER) CPI and Rent CPI), so the overall trend and level of Shelter CPI will largely determine Headline and Core inflation measures.

The slow decline in Shelter CPI has surprised many, particularly as most leading indicators of Shelter CPI have largely returned to pre-COVID levels. This is true of Zillow’s Observed Rent Index, which bottomed over 12 months ago and has been flat every since.

The same can be said of the BLS’ New Rents Index.

Ditto CoreLogic’s Single-Family Rent Index.

But, some Shelter inflation leads are pointing to a modest rise in the short-term. InflationGuy’s Primary Rents Model is one such indicator.

Source: InflationGuy

Along with the growth in US house prices, which has historically been a reliable lead indicator of the OER component of Shelter CPI.

There appear to be a number of conclusions we can make from there various indicators of rental costs and thus Shelter CPI:

Given a number of these lead indicators appear to have bottomed and some have reaccelerated suggest the decline in Shelter CPI should continue into 2025, but at a slower pace; and,

There is evidence to suggest Shelter CPI is set to return to pre-COVID levels, but that is not likely until much later in 2025, and we may even see a re-acceleration first.

Overall, we should expect Shelter CPI to continue to trend lower over the next 18 months, though the pace is not likely to be swift, unless this is offset by re-accelerating wage growth.

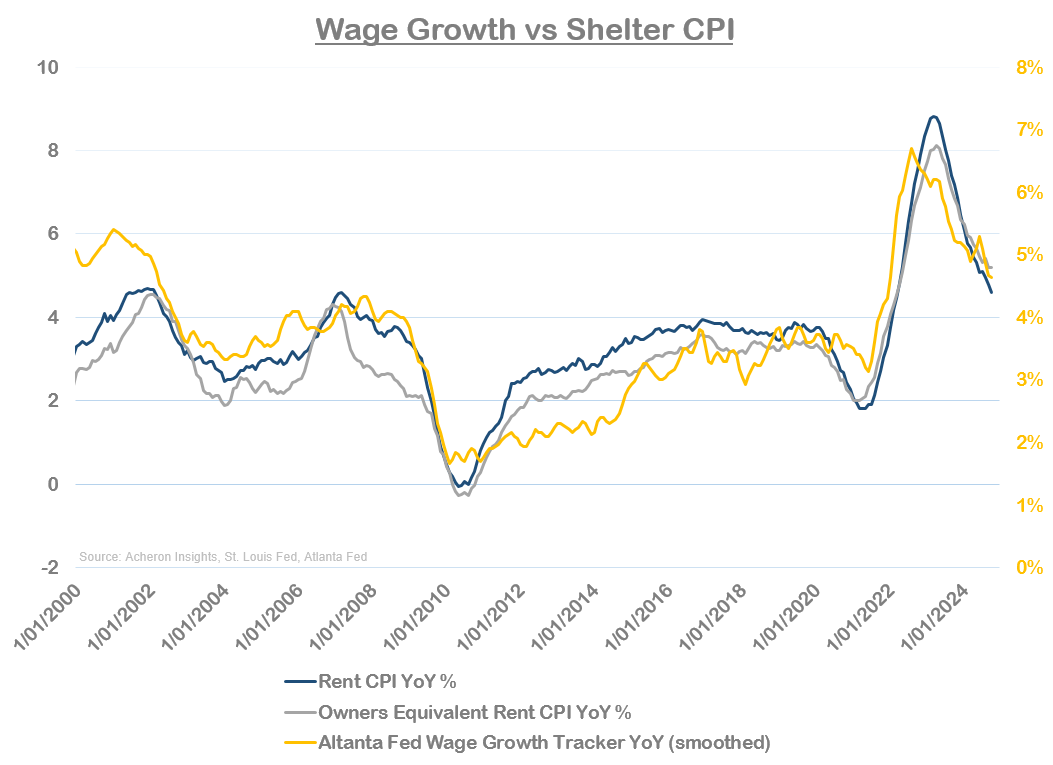

Indeed, another important factor to consider as it relates to Services CPI overall in addition to Shelter CPI is wage growth, which as we can see below, has historically been perhaps the most important driver of both.

When we look at the above charts, the slow decline in Shelter CPI and overall stickiness of Services CPI makes sense. Wage growth is declining, but remains well above pre-COVID levels.

Therefore, where wage growth is heading will ultimately have the largest directional impact on the direction of Services CPI and inflation as a whole moving forward.

And, as has been the case from much of the past 18 months, wage growth lead indicators have been trending lower. That remains the case today, but the pace of deceleration does appear to be slowing.

Therefore, we should expect to see Shelter CPI and overall Services CPI trend lower over the next six months, but at a slower pace than what we have exhibited in 2024. The normalisation of Auto Insurance CPI (currently at 14% YoY) will also provide added downside pressures, though is only 3% of the Headline basket.

For 2025, the inflation story is thus set to be how much of the upside pressures in Goods CPI can offset those of decelerating Services CPI. I expect it to be somewhere in the middle, which is why we are likely to have bottomed and should see a moderate move to the upside from here. While any upside move is unlikely to push CPI measures much above 3-3.5%, they should be enough to continue to put some pressure on the Fed and long-term interest rates.

The Fed has chosen to ignore above target inflation in favour of reducing the policy rate to help accommodate the growing federal deficit. While this is to be expected to continue for the most part over the coming decade, periods of above target and rising inflation will at some point force the Fed’s hand, if only for a short-term.

It seems this could be the case at some point in 2025. But don’t expect CPI above 3.5-4%, as that simply cannot occur with services inflation trending lower.

In isolation, this may be not a problem for asset market, but when stocks are priced to perfection and a significant easing cycle has been priced in, persistent upside surprise in inflation over the next six months may cause a temporary re-pricing of asset prices and monetary easing expectations.

. . .

Thanks for reading!

If you would like to support my work and continue to allow me to do what I love, feel free to buy me a coffee, which you can do here. It would be truly appreciated.

Regardless, feel free to share this with friends and around your network. Any and all exposure goes a long way and is very much appreciated. Thanks again.