The Calm Before The Storm

Summary & Key Takeaways:

Stock market fundamentals are solid, but slowly weakening, particularly from a liquidity perspective.

What’s more, most long-term measures of sentiment and positions are maxed out. Markets are also priced to perfection from a fundamental perspective.

As a result, should economic data and corporate earnings begin to disappoint, and global liquidity continue to trend lower, we could see a significant bought of volatility coming to the markets. Waning market breadth are seemingly confirming this outlook.

In the short-term however, given the strength of overall market internals, underweight hedge fund exposure and the fact that the weeks leading into early to mid-January are generally the most favourable for the stock market suggests we could have one final leg higher before a much more volatile 2025.

Either way, there is ample evidence to suggest 2025 will be a much more challenging year for equities than we have experienced over the past 24 months.

The Fed has played their hand, but they can only hold out for so long

One of the primary drivers of my recent bullishness toward the stock market has been the willingness of the Fed and other central banks to ease monetary policy amidst robust economic growth (at least in the US) and above target inflation.

The Fed in particular has illustrated to the world their dovish reaction function, despite underlying data not wholly supportive of rate cuts. We now live in a world of populism and monetary debasement, where central bankers of the world’s developed economies having their hands tied by the excessive government debt burdens and continued deficit spending. Monetary policy actions over the past few months have again illustrated policy makers will do whatever it takes to ease.

These two opposing forces in above target inflation and excessive government spending thus create an environment where we are likely to see more volatile monetary policy. We are currently in the easing stage of that cycle which is undoubtedly bullish for risk assets, but the question now becomes how long will it last.

This answer likely lies in the direction of inflation growth. The Fed has made it clear they are happy to tolerate above target inflation that is trending sideways (as has been the case for the past few quarters), but I am not so sure they will tolerate above target inflation that is also trending higher.

As I detailed here, I suspect we will see inflation trend modestly higher over the next few quarters, potentially as high as 3.5%. At the very least, we are likely past a cyclical low in inflation.

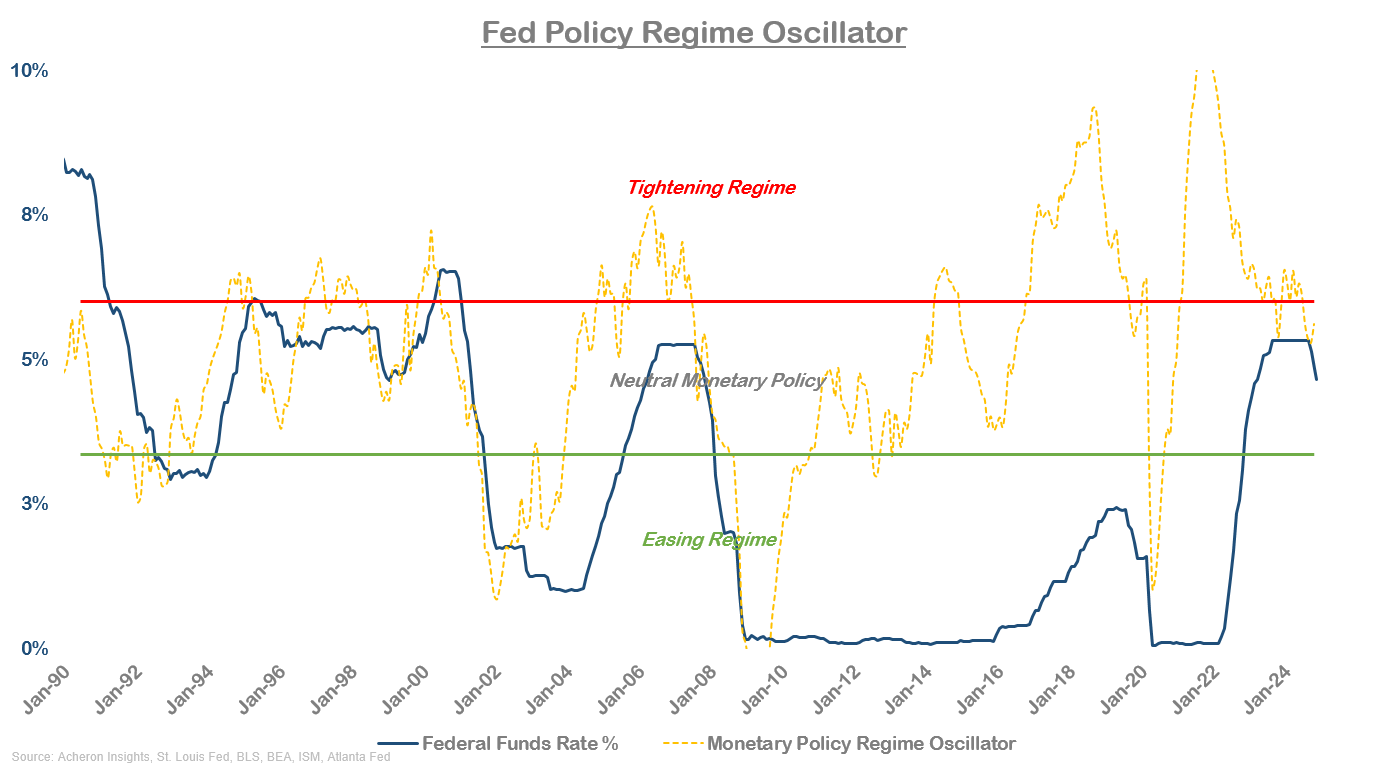

And when we look at the entire swath of data that generally determines monetary policy (employment, economic growth, financial markets, in addition to inflation) in the form of my Fed Policy Regime Oscillator below, this continues to point to neutral monetary policy at best.

Inflation surprises and economic surprises are also signalling neutral-to-hawkish monetary policy in the US. Similar data also no longer favours further easing from other central banks at present.

As a result, unless the data turns more favourable on the inflation front (unlikely from what we have seen), or deteriorates to the downside on the economic front, this easing cycle is not likely to last as long nor be as excessive as market participants are both expecting and pricing in.

Economic resilience to continue

One thing we can have greater assurance on over the medium-term however is the continued resilience of the US economy.

I have said this much in recent times, but is worth repeating: the lead indicators of the US business cycle are not signalling any kind of imminent recession.

This is obviously a supportive dynamic for markets. We are not going to see any kind of recession-driven sell-off in the stock market.

But we are in a situation where equity markets have excessively priced in a strong US economy. This makes the market vulnerable to downside surprises in economic growth, which could well be the case in 2025, particularly as housing market activity is deteriorating and longer-term lead indicators are now much less favourable.

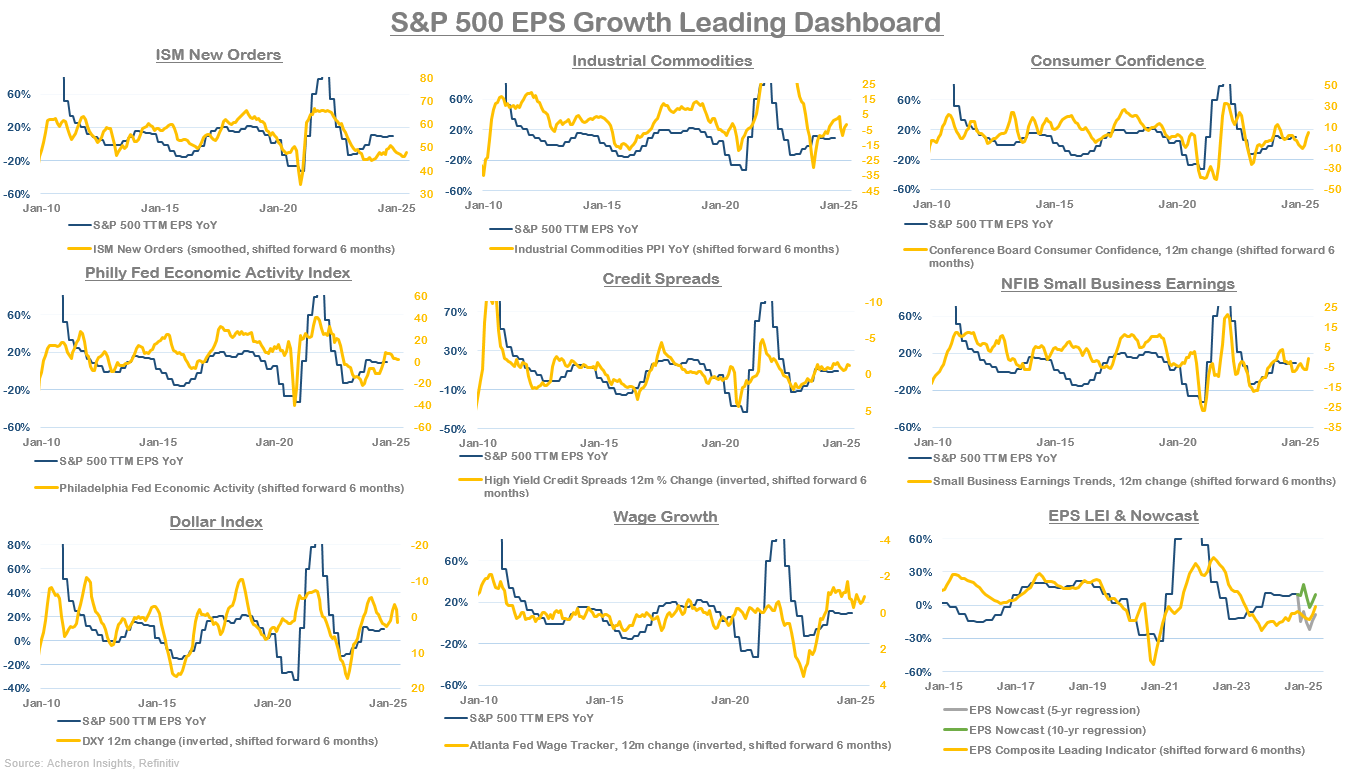

The stock market is also fully priced relative to earnings growth expectations, as we can see below.

Again, should earnings growth disappoint in 2025, such a scenario could result in greatly increased market volatility.

As it stands, most EPS lead indicators are giving mixed signals for the next six months or so.

Other composite earnings growth lead indicators such as those of Morgan Stanley are pointing to declining earnings growth in 2025.

Source: Morgan Stanley

Again, when the market is aggressively priced from an economic and earnings growth perspective, downside surprises are likely to lead to increased volatility, though we shouldn’t expect to see any material collapse in earnings any time soon.

Overall, fundamental drivers of the market are yet to roll off a cliff, but their support is waning, as we can see below.

The same can be said of liquidity and financial conditions.

The strength of the US dollar has been a particularly strong headwind of late, particularly as it relates to global liquidity growth.

Indeed, global liquidity is waning, and unless the dollar falls in the short-term, this headwind is likely to continue into 2025, particularly as there is a large swath of maturing debt that needs to be refinancing over the coming year. Declining global liquidity growth coupled with increased debt refinancing needs is the recipe for refinancing stress.

Sentiment and positioning are stretched

From a stock market sentiment and positioning perspective, the market seems to currently find itself it a situation where all long-term sentiment measures are reaching extreme levels, but there remain one notable groups of market participants that are still underweight stocks: hedge funds.

Sentiment is very frothy right now. Bank of America’s Fund Manager survey is also very much confirming this, illustrating that managers are currently as overweight stocks as they have been since just before the GFC.

While fund manager cash allocations are also at record lows.

While these stretched positioning metrics certainly suggest we are close to some kind of top in markets, the fact that net speculative positioning is now underweight stocks (driven by significant hedge fund deleveraging, as we can see below), suggests to me there is further room to run for them market in the short-term.

Markets rarely top when hedge funds are underweight stocks, and even though such measures as my S&P 500 Fair Value model is pointing to a significantly overvalued market, I would like to see hedge funds capitulate to the long side before becoming too bearish, but the warning signs are there.

A blow-off top?

This is where the short-term indicators of the market come into play.

For now, stock market internals are largely supportive of the recent move higher. But we do appear to be seeing clear signs of waning participation. For one, my pro-cyclical index has started to diverge lower, if only slightly (as this can persist for prolonged periods of time).

We are also seeing very poor market breadth, as fewer and fewer constituents are taking part in the gains of the overall index.

Longer-term breadth measures such as the percentage of stocks above their 50 and 200-week moving averages have diverged notably over the past few months.

We are also seeing similar divergences in short-term breadth measures, as we can see below.

Breadth divergences can of course self-correct, but the extent to which we are seeing these divergences, coupled with deteriorating global liquidity, moderating underlying fundamentals and a stock market that is fully priced relative to its fundamental drivers suggests these kinds of divergences could have greater meaning.

From a technical perspective, we are also starting to see some divergences from a longer-term perspective.

That does not mean we are likely to see any king of imminent correction of bear market. But it does suggest the likelihood of increased volatility over the short to medium-term appears likely.

But for now, given the strength of overall market internals, underweight hedge fund exposure and the fact that the weeks leading into early to mid-January are generally the most favourable for the stock market suggests we could have one final leg higher before a much more volatile 2025.

. . .

Thanks for reading!

If you would like to support my work and continue to allow me to do what I love, feel free to buy me a coffee, which you can do here. It would be truly appreciated.

Regardless, feel free to share this with friends and around your network. Any and all exposure goes a long way and is very much appreciated. Thanks again.