US Economic Resilience Should Continue, But Cracks Are Forming

Summary & Key Takeaways:

The US economy is far from recession. Economic growth remains robust, driven by strength in the services economy, along with robust income and consumption growth. The primary detractor of economic growth has been weakness in the manufacturing sector, and recently, declining growth in employment.

From a leading indicator perspective, there is little evidence of impending weakness, so we should expect economic resilience to continue as most short-term leading indicators remain favourable.

However, some of the long-term leading indicators are beginning to roll over, suggesting 2025 may well be the year economic growth starts to disappoint to the downside.

This is notable in the case of easing financial conditions, with have yet to notable translate into improved underlying economic activity, particularly in the housing market.

What’s more, the market is overvalued versus underlying economic growth and liquidity, while investor sentiment and positioning is reaching extreme levels. This leaves the stock market vulnerable should growth start to surprise to the downside, which is likely at some point in 2025.

As such, investors should expect 2025 to be very different to what we have experienced over the past 24 months.

The US economy remains resilient

A resilient US economy has been the theme of 2023 and 2024. As it stands today, there is little evidence to suggest otherwise.

Since late 2022, economic growth has been modestly trending higher, lead by strength in the services economy and above trend growth in consumption and incomes. On the other hand, manufacturing and industrial production has been weak.

As we can see below, my Business Cycle Index - which attempts to track the US business cycle using key economic data points from all areas of the economy - continues to largely trend sideways to modestly higher.

The US economy appears to be growing at an average pace, currently ~2% YoY. Average growth is by definition not what occurs during recession. Indeed, since 1960 every recession has coincided with growth in the Business Cycle Index turning negative. This is not the case today.

Below is a six-month annualised growth version of this index, which perhaps does a better job illustrating the recent resilience of US economy.

Importantly, other composite measures of the US business cycle are confirming this trend, such as the Conference Board’s Coincident Economic Index.

If we compare these hard data with some of the soft data measures of the business cycle in the form of the various US PMIs, we can see again how growth seemingly bottomed in late-2022 and has been modestly higher since on average. What we can also glean below is how manufacturing PMIs have clearly been weaker than non-manufacturing PMIs over the past year, confirming the struggle in the US manufacturing economy relative to the services economy. The former are in contractionary territory (sub-50), while the latter are in contractionary territory (above 50).

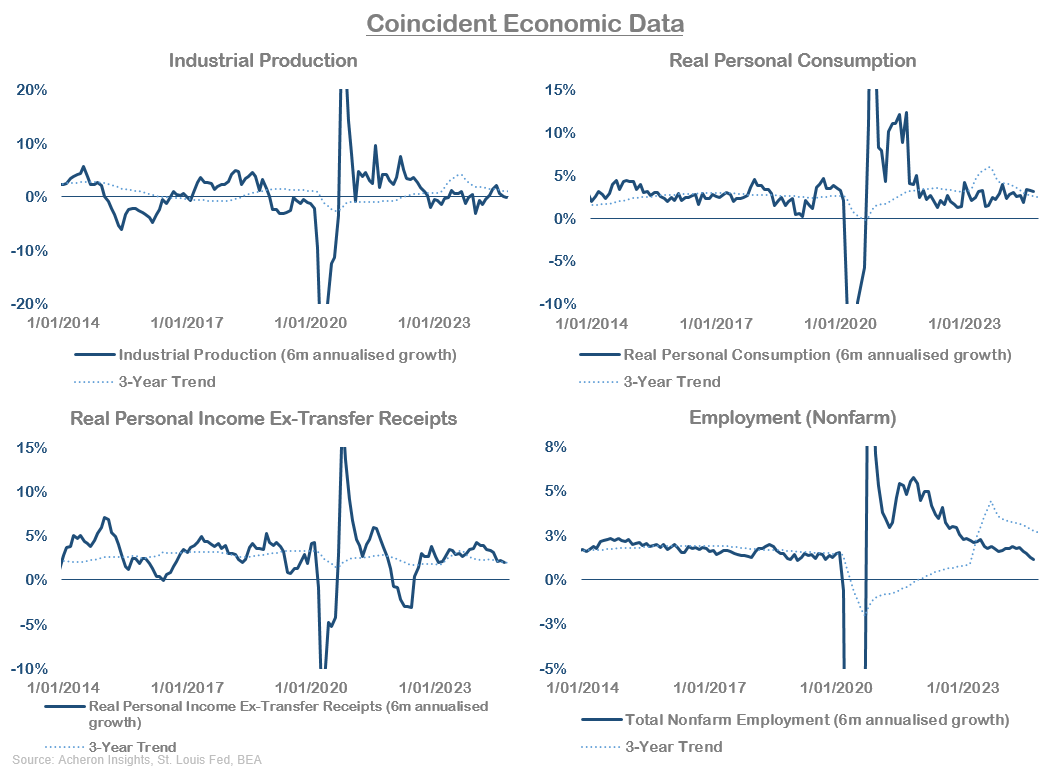

Digging a little further into the individual hard economic data themselves, the below dashboard displays each of the four components of my Business Cycle Index, allowing us to see where economic strength or weakness is being derived. As we can see, the majority of recent economic weakness has come in the form of decelerating employment growth (though still positive) along with weak industrial production growth which has been below trend and negative for much of the past 24 months.

On the other hand, consumption growth has been positive and robust during this period, as has income growth (though slight weakness in the latter can be seen in recent months).

If we compare these various data points (and others) relative to their own history’s, we are able to obtain further understanding of which areas of the economy are exhibiting strength and weakness. As we can see below, industrial production and retail sales growth are contracting from economic growth, while overall consumption, incomes and manufacturing and trade sales are all growing at average levels.

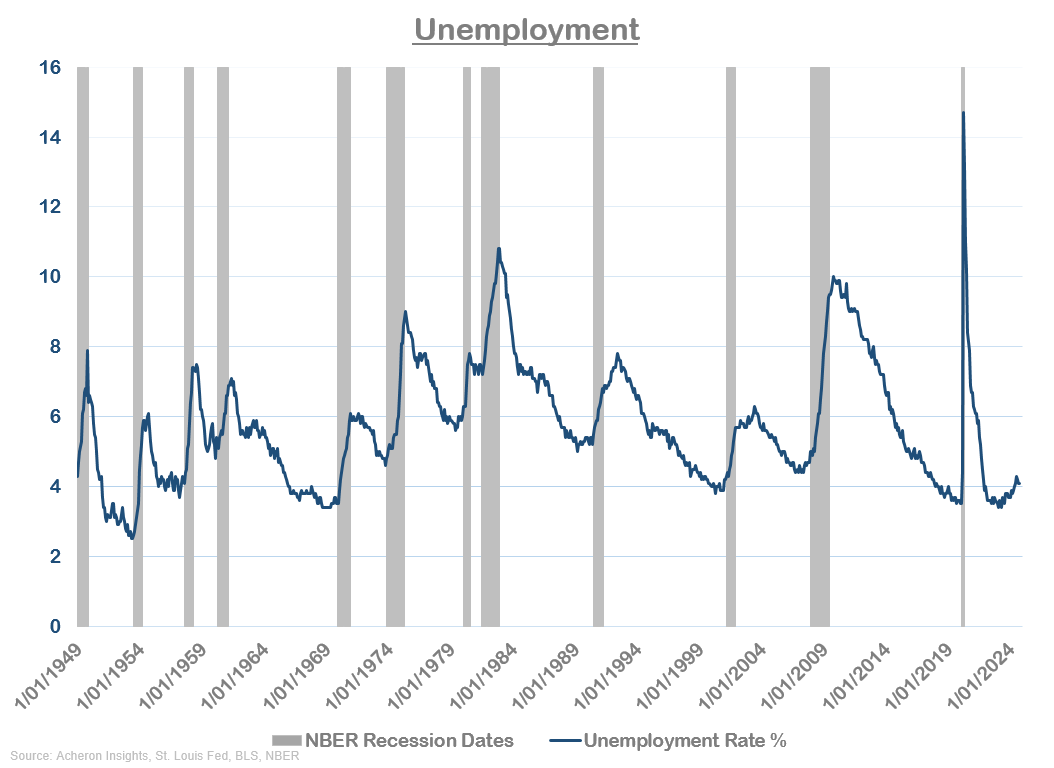

While it is true the growth in employment has been weak of late and contracting from economic growth, the labour market overall is still doing fine. An unemployment rate of 4.1% is not what we see during recession nor a weak economy.

If we turn our focus to the manufacturing sector (a key detractor from the economy of late, as we have discussed), we can see the weakness has been relatively broad based, though the sector is still growing at a higher rate than it was during 2022. While it is true the manufacturing sector is now only a small part of the US economy, it remains one of the key cyclical drivers of the business cycle.

Soft data from the manufacturing sector in the form of the sub-categories of the ISM manufacturing survey are confirming this notion. 2023 saw a modest rebound in manufacturing activity while 2024 has seen a modest decline.

But as we have seen, this decline in manufacturing activity in 2024 did not translate into notable overall economic weakness due to strength in other areas of the economy, with the services sector faring far better.

While services consumption and disposable income growth have been choppy, both have been firmly positive and at or above average levels seen over the past decade (particularly from a consumption and services PMI perspective). Non-cyclical employment has been a drag on economic growth of late as it continues to trend lower.

As we can see, the US economy overall remains robust though not outstanding. Although we have seen a contraction in manufacturing activity and some weakness in employment, overall consumption remains robust (particularly on the services side) on the back of robust income growth.

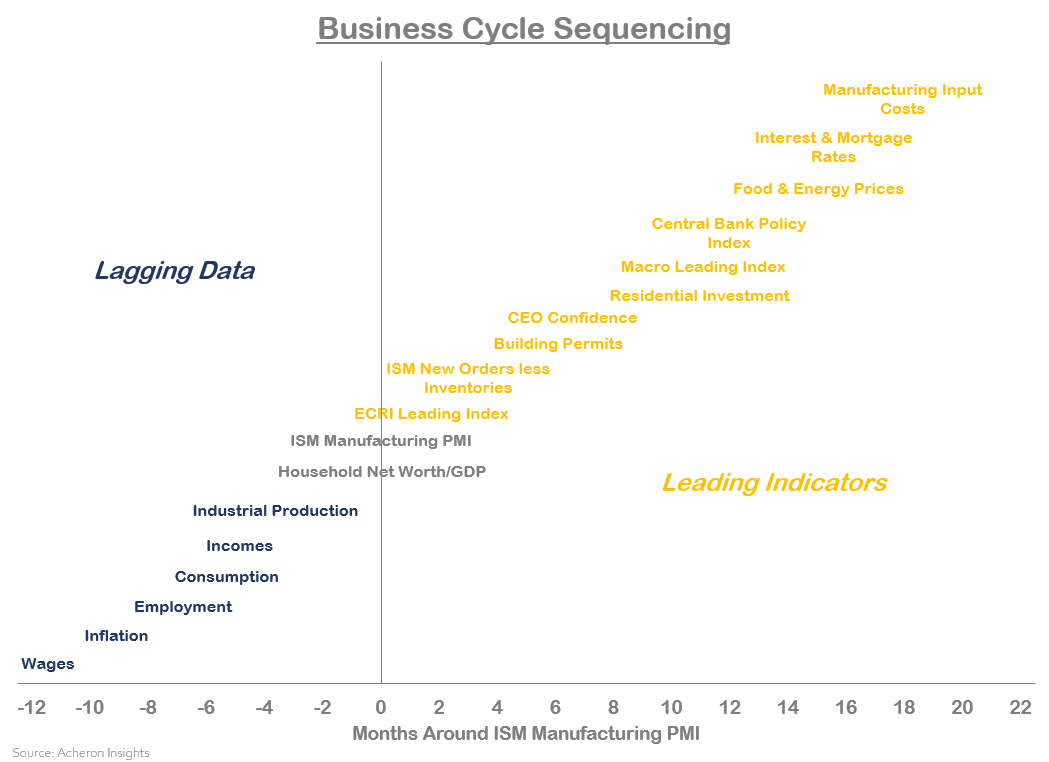

But as always, we must remember all data presented above are coincident and lagging to some degree, with the timeliest data points generally being the PMIs. The following chart illustrates the sequencing of the business cycle, from hard economic data points as well as leading indicators and the extent to which they generally lead and lag the PMI.

When we understand this sequencing process of the business cycle and its natural leads and lags, the data often makes much more sense.

When we understand this dynamic, can better grasp the power of the business cycle and how almost all economic data along with asset price fluctuations are almost always a function of said business cycle.

Herein lies the importance of assessing the outlook for where the business cycle may be headed and the importance of leading economic indicators.

The outlook for the business cycle is slowly deteriorating, but there is little yet to fear

Thus, we can now turn our attention to what really matters from an investment perspective, the lead indicators of the business cycle.

For most of 2024, business cycle lead indicators have largely been forecasting what has played out: modest growth with little evidence of impending weakness. That remains largely the case today, though many of the longer-leads are starting to turn down.

Starting with the short-term outlook, the various regional Fed real GDP nowcasts are pointing to a modest decline in real GDP growth in Q4. The Atlanta Fed’s GDPNow is the most favourable of these, forecasting Q4 real GDP growth of 2.7%, a relatively robust figure.

I tend to put the highest weight on the Atlanta Fed model of those presented above. Importantly, other high frequency data points and short-term leads are seemingly confirming this robust outlook.

For one, the Fed’s Weekly Economic Index has not turned lower nor signalling any kind of notable economic weakness through the first two months of Q4.

Likewise, ECRI’s Weekly Leading Index continues to largely trend sideways and is positive overall.

Meanwhile, the cyclical components of GDP (residential investment, durable goods consumption and transportation equipment investment) which tend to lead overall GDP growth by about a quarter are exhibiting accelerating growth on a composite basis.

The same can be said of household net worth as a percentage of GDP.

The Conference Board’s Leading Economic Index also continues to trend higher on a growth rate basis is

Another short-lead indicator which is not as unfavourable as it has been previously is the ISM Manufacturing New Orders less Inventories spread. Though it has yet to inflect higher, this indicator is no longer trending downward, suggesting any material weakness in the manufacturing sector over the short-term appears unlikely.

When we look at similar new orders/inventories spreads via the regional Fed data, the message is even more favourable for the manufacturing sector over the short-term.

This is particularly true of the Philly Fed, with the New Orders index recently reaching its highest level since early 2022.

Easing lending standards are also generally a tailwind for industrial production growth.

As well as retail sales, though the positive benefit of easing credit card lending standards is much less pronounced and may be close to running its course.

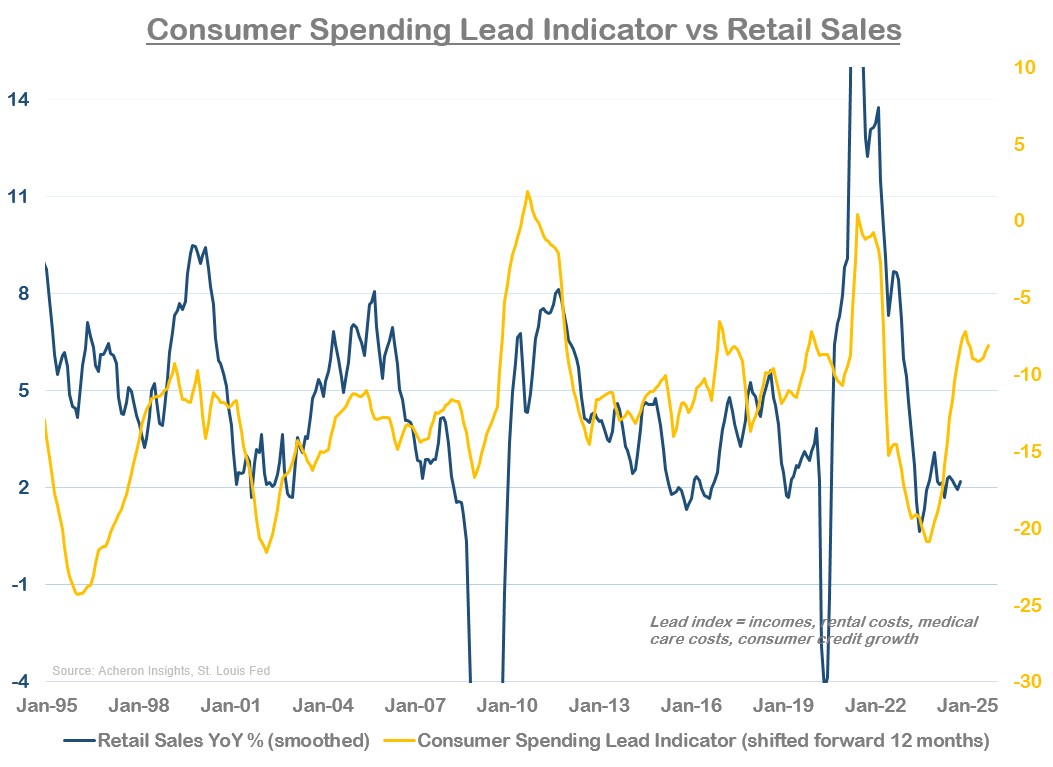

My consumer spending lead indicator also remains positive. However, this indicator has been moving sideways for circa six months now, suggesting its positive impulse may wane come 2025.

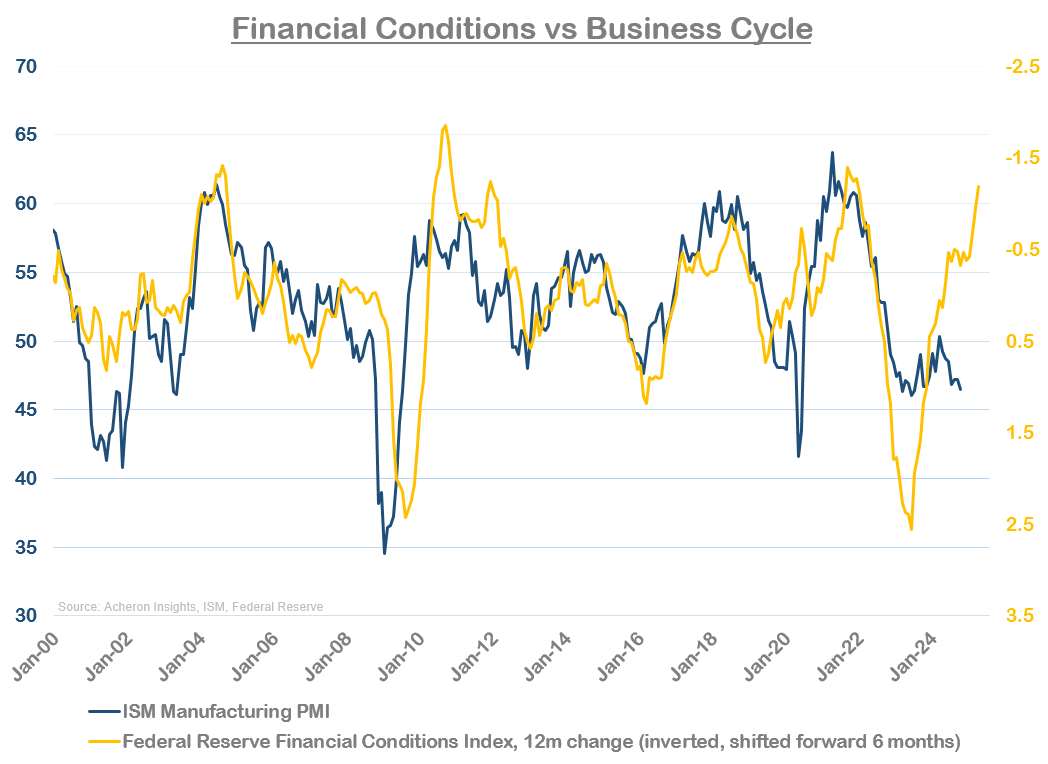

On the other hand, easing financial conditions remain a firm tailwind for the economy. Though it must be said, this tailwind looks to have translated little into actual underlying economic activity throughout 2024, which may be cause for concern.

This notion is seemingly confirmed by CEO confidence, which tends to lead the business cycle by around six months and is waning. CEO confidence is largely a function of financial conditions and stock market performance.

Nonetheless, while easing financial conditions are yet to translate into noticeably improved economic activity, they remain supportive of the business cycle on a rate-of-change basis for now.

One of the primary transmission mechanisms to which easing financial conditions stimulate the economy is via the housing sector. And, as we can see below, the 12-month change in mortgage rates has historically been an excellent short-term lead of housing market activity, for obvious reasons. While mortgage rates remain elevated on an absolute basis, they have retraced notable on a rate-of-change basis (inverted below). This has clearly resulted in improved homebuilder sentiment via an increase in the NAHB Housing Index, but has not translated (yet) into an increase in building permits, and thus actual underlying economic activity.

In fact, growth in building permits is still on the decline, a headwind for the business cycle.

And as a result, so is residential investment, one of the primary cyclical drivers of economic growth.

As such, for the economy to grow meaningfully from here, we likely need to see mortgage rates further retrace and for this to actually translate into increased housing investment and construction, so watch this space.

Another tailwind for the business cycle which appears to be turning to headwind is inflation and input prices. As we can see below, manufacturing prices (as proxied via the ISM Manufacturing Prices Paid index) tend to lead the business cycle by around 12-18 months, and have been trending lower over much of the past 12+ months now. Remember, for leading indicators such as this, the turning points and direction of travel matter more than the magnitude of movements.

The same can be said of commodity and manufacturing input prices as measured via their respective Producer Price Index’s.

And finally, my Macro Conditions Lead Index has also seemingly begun to roll over. This index was wholly supportive of the business cycle in 2023 and 2024, and it appears that may not be the case in 2025.

A global perspective

As always, it was be imprudent to assess the outlook for the US business cycle without considering the implications of the global business cycle given the interrelation between the two.

One lead indicator which remains firmly positive is my Global Central Bank Policy Index, both for the world as a whole and G10 central banks. Central banks continue to ease monetary policy on net, which historically has been supportive of the global business cycle over the following nine or so months.

Likewise, the percentage of global OECD Composite Lead Indicators continues to rise on net, a dynamic which generally has been a reliable lead indicator of the global business cycle.

Lead indicators of the European business cycle also remain neutral to supportive of the business cycle over the short to medium-term.

Of course, the big question market for global growth is China, whose economy remains mired in a balance sheet recession and housing market crisis. Stimulus efforts by policy makers have thus far been ineffective in stimulating an economy recovery. Both the China Credit Impulse and China M1 continue to decline, a headwind for the global business cycle.

However, there appears to be some signs of life. Chinese bond yields have historically been reliable lead indicators of Chinese M1 and the China credit impulse, and their recent move lower suggests we should see these two data points tick higher over the medium-term.

Whether this proves true remains to be seen. I would be much more confident were China’s Leading Economic Indicator moving notable higher, but it has been flat for nearly six months now on a growth rate basis. For now, China remains the wildcard for 2025.

Where does this leave investors?

Economic resilience has undoubtedly been supportive of risk assets over the past 24 months, particularly when calls for recession were so consensus during 2022 and 2023. But now, we are at a point where the stock market and risk assets have priced in a lot from an economic growth and fundamental perspective, as we can see below.

This leaves the market thoroughly overvalued relative to not just underlying business cycle fundamentals, but also to the liquidity cycle, as we can see below.

What’s more, my composite S&P 500 fair value model is also firmly in overvalued territory. This model incorporates not just growth and liquidity, but other valuation indicators such as the CAPE ratio, and interest-rate adjusted PE ratios among others.

In addition, economic surprises have firmly been to the upside of late, and, given this is a mean-reverting measure by nature, at some point growth will start to surprise to the downside.

Of course, the market can remain overvalued versus both growth and liquidity for prolonged periods of time (refer the dotcom bubble for example). But, when such overvaluation is present at a time where fundamentals drivers begin to deteriorate, that is when trouble can arise.

While we are likely not there yet (given short-term business cycle lead indicators remain robust), the fundamental picture is clearly deteriorating for the market.

As is the liquidity picture.

What also leads me to be increasingly concerned for the market in 2025 is the positioning cycle. As we can see below, many sentiment and positioning measures are maxed out. Again, this means little for the short-term (particularly as hedge funds, CTAs and vol targeting funds have plenty of room to run), but at some point these dynamics will matter for the market.

In all, the outlook for the business cycle should remain supportive of risk assets in the short-term at the very least. But, as we have seen, longer-term leading indicators are turning lower at a time where the market is overbought versus underlying fundamentals. I don’t expect growth to deteriorate such that we see a recession in 2025 or be the impetus for a major risk of event, but it certainly could lead to increased market volatility given where we are in the positioning cycle.

Investors should expect 2025 to be very different to what we have experienced over the past 24 months.

. . .

Thanks for reading!

If you would like to support my work and continue to allow me to do what I love, feel free to buy me a coffee, which you can do here. It would be truly appreciated.

Regardless, feel free to share this with friends and around your network. Any and all exposure goes a long way and is very much appreciated. Thanks again.