The Fed Doesn’t Need To Cut Rates, But Probably Will Anyway

Summary & Key Takeaways:

Relative to inflation, employment and economic growth, monetary policy is neutral to slightly tight. But this is not an economy that needs rate cuts.

And yet, given the political will the Fed has to cut rates prior to the election, one and maybe even two cuts in 2024 seems the likely scenario, along with reduction in balance sheet run-off.

Positive progression on the wage growth front may be the Fed’s only data supported avenue for easing monetary policy.

On the margins, this is supportive of risk assets and could go a long way to igniting animal spirits for a blow-off top to close out the year.

For 2025, the Fed and the market are expecting three to four further rate cuts. This is not going to happen.

Just how brave are you Jerome Powell?

The data driven approach to the Federal Reserve’s monetary policy decision making process has simply not afforded Powell & Co. any scope to ease monetary policy since they ceased hiking rates in July 2023.

As it stands today, maybe, just maybe, we are seeing a confluence of economic data that may allow the Fed to undertake its one or two rate cuts it so badly wants. Are they justified by economic data? No. Not really. But it depends how you spin it.

With the political pressure for pre-election rate cuts evident, it appears the Fed may have a window to squeeze through a cut or two along with the continued tapering of QT, even if they are not data supported. Just don’t expect a fully-fledged easing cycle any time soon.

The economy is doing fine

From an economic growth perspective, the Fed doesn’t really need to ease monetary policy. After all, we are probably approaching (or more likely, well past) the cyclical low in coincident economic data. While the outlook for the US economy appears robust.

And, outside of a notable downturn in manufacturing and industry (which is now entering a cyclical upturn), other key drivers of economic growth in the form of consumption and employment continue to hold together. Where we are now seeing deterioration in hard economic data is in relation to incomes, which as we shall see later could offer the outlook to easier monetary policy, if only temporarily.

If we assess where monetary policy stands relative to current economic growth, one could make the case monetary policy is closer to tight than it is loose. While the historical relationship between the fed funds rate and GDP growth is not overly tight, the current state of economic growth is generally associated with a marginally lower fed funds rate. Note the emphasis on marginally.

The problem is, if the leading indicators are correct, coincident economic data should strengthen from here, not weaken. But we all know the Fed wants to cut, and as such, we should expect them to take advantage of any weakness in the business cycle should this eventuate.

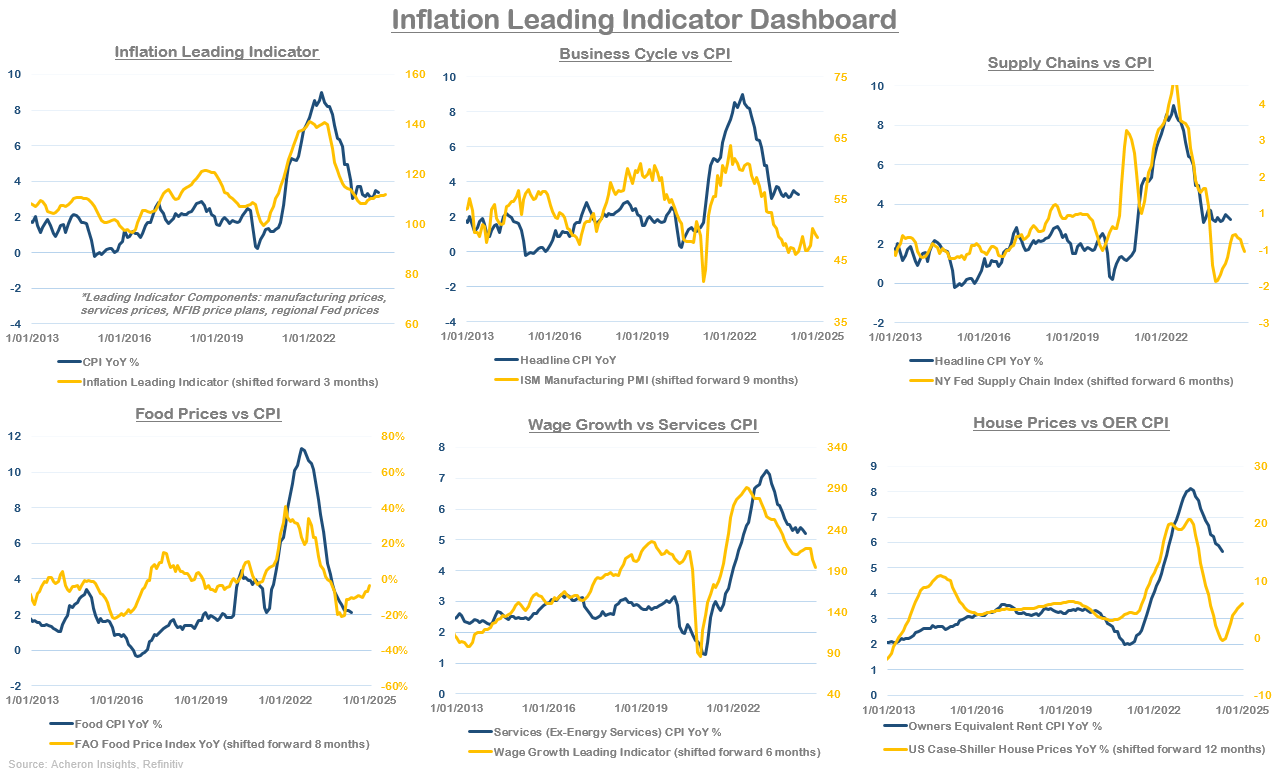

The inflation war isn’t won, but the battle is probably over

From an inflation point of view, it is a similar story. Current inflation data doesn’t really justify rate cuts. But, if the Fed really wants to cut, then they may be able to get away with one or two cuts based on where inflation data presently resides.

May’s downside surprise in CPI is certainly testament to this. And, as we can see below, upside inflation momentum is beginning to wane. This is important as upside surprises in inflation have dominated 2024, led by sticky services inflation and rent inflation that refuses to decelerate at the pace consensus though it would. The Fed will take all the downside inflation surprises they can get.

We must remember inflation has made very constructive progress to the downside over the past 18 months, such that monetary policy is now starting to look somewhat tight relative to Core CPI.

Is inflation tight enough to warrant rate cuts? Again, probably not. In only four of the 11 major easing cycles since the 1950’s did the fed funds rate peak at a smaller spread over Headline CPI than the 1.9% difference we have currently. And, only twice was it smaller than the current 2.5% spread over Core PCE. It is unusual for the Fed to ease monetary policy given similar conditions historically, but not unheard of.

In terms of the outlook for inflation, I continue to believe we will not see a return to sub-2% CPI at any point this business cycle. This take shouldn’t come as a surprise to anyone by now. However, I also do not see inflation rising back above 5% any time soon. As it stands, I suspect we will see inflation largely trend sideways as we progress through 2024. And, as we approach 2025, goods inflation will likely begin to bias inflation higher.

Again, this probably affords the Fed a window over the next quarter or two to cut rates. Beyond 2024, I don’t believe inflation will offer any scope for rate cuts. In fact, I suspect rate hikes will be back on the agenda at some point in 2025.

The Fed will like what is sees from the jobs market

When we turn our attention to the jobs market, this is one area of the Fed’s mandate where rate cuts are far easier to justify, particularly as it relates to wages.

Overall, the jobs market has cooled markedly form its historic tightness seen in recent years. Though unemployment has only budged off its cycle lows, employment growth, job openings and weekly hours worked among many other labour market data points have cooled to levels much more in-line with what we have associated with dovish monetary policy.

Having said that, I must point out that I do not believe we are going to see a material spike in unemployment, nor a continued deceleration in employment growth that is sufficient to trigger a recession or significant level of rate cuts. As we can see below, my lead indicators have been suggesting for months now employment growth is in the process of bottoming and should start accelerating once again very shortly.

But, as it stands today, the Fed can easily make the case rate cuts are justified given current employment growth and the recent changes in the federal funds rate. This window is likely to be fleeting however.

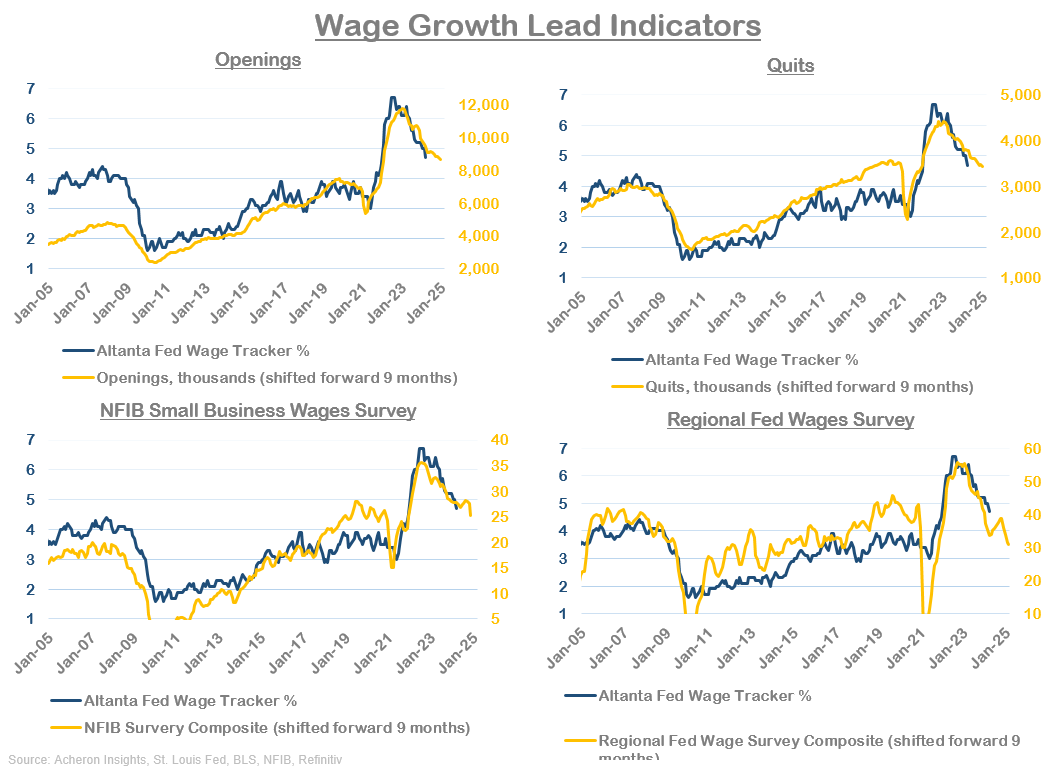

Where the Fed will be most happy is the downside progress in wage growth. Put simply, there is little evidence we are amidst a wage-price spiral. Yes, the Atlanta Fed Wage Tracker is still well above levels seen throughout the 2010s, but other measure of wage growth has returned to average levels and are currently below trend.

While my wage growth composite leading indicator and forecasts are suggesting the Atlanta Fed’s Wage Tracker will continue to decline for much of 2024.

The pace of decline is likely to lessen from here, but this is an outlook several wage growth lead indicators are also confirming.

Central bankers put a heavy emphasis on wage growth given how it is a key driver of services inflation and the stickiness of inflation overall. But, as we can see above, wage pressures are one area of the Fed’s mandate that actually isn’t requiring overly restrictive monetary policy.

Putting it all together

In all, it is evident to me aside from what we are seeing on the wage front, the US economy is not really in need of rate cuts. I think the below chart summarises this well. Further progress is needed on the inflation front to truly justify a proper easing cycle. That seems unlikely to happen anytime soon.

If we look at current financial conditions, then the argument for rate cuts is nearly impossible. For one, credit spreads are at cycle lows and are suggesting monetary policy may even be too easy at present.

Meanwhile, if we compare the Chicago Fed’s Financial Conditions Index to the historical averages associated with the commencement of easing cycles (a negative reading meaning easier financial conditions), all components within this index are well below average levels associated with the beginning of easing cycles. And, anytime the Fed has cut rates when financial conditions have been similar to where they are currently, it was with inflation at much lower levels.

Having said that, there is absolutely no doubt the Fed wants to ease monetary policy. And as a result, it seems inevitable they will. This will likely take the form of at least one rate cut (which the Fed themselves signaled is their plan during this week’s FOMC meeting), in addition to slowing the pace of their balance sheet run-off program which is scheduled to begin this month.

The market itself remains a little more dovish than those at the FOMC. SOFR futures are pricing in one rate cut in September, followed by another in December. There are five rate cuts in total priced in from now until 2025, while the Fed also anticipate they will cut a further four times in 2025.

Overall, given the political will the Fed has to cut rates, one and maybe two cuts in 2024 seems the likely scenario. On the margins this is supportive of risk assets (if only minimal), but could go a long way to igniting animal spirits for a blow-off top to close out the year.

As for 2025, I think both the Fed and the market are well off the mark. To me, it’s more likely we see a rate hike in 2025 than four rate cuts. But that’s a story for 2025, not 2024.

. . .

Thanks for reading!

If you would like to support my work and continue to allow me to do what I love, feel free to buy me a coffee, which you can do here. It would be truly appreciated.

Regardless, feel free to share this with friends and around your network. Any and all exposure goes a long way and is very much appreciated. Thanks again.