Don’t Expect A Stock Market Correction, But The Easy Money Has Been Made

The easy money has been made, for now

While it is not the time to be making any kind of significant bear case for risk assets, I think we are reaching the stage in the cycle where most of the easy money has been made. At least for the time being.

I have been - and still am - relatively constructive toward both stocks and commodities for the rest of 2024. But I suspect the next few months will not resemble those that have been so favourable since October.

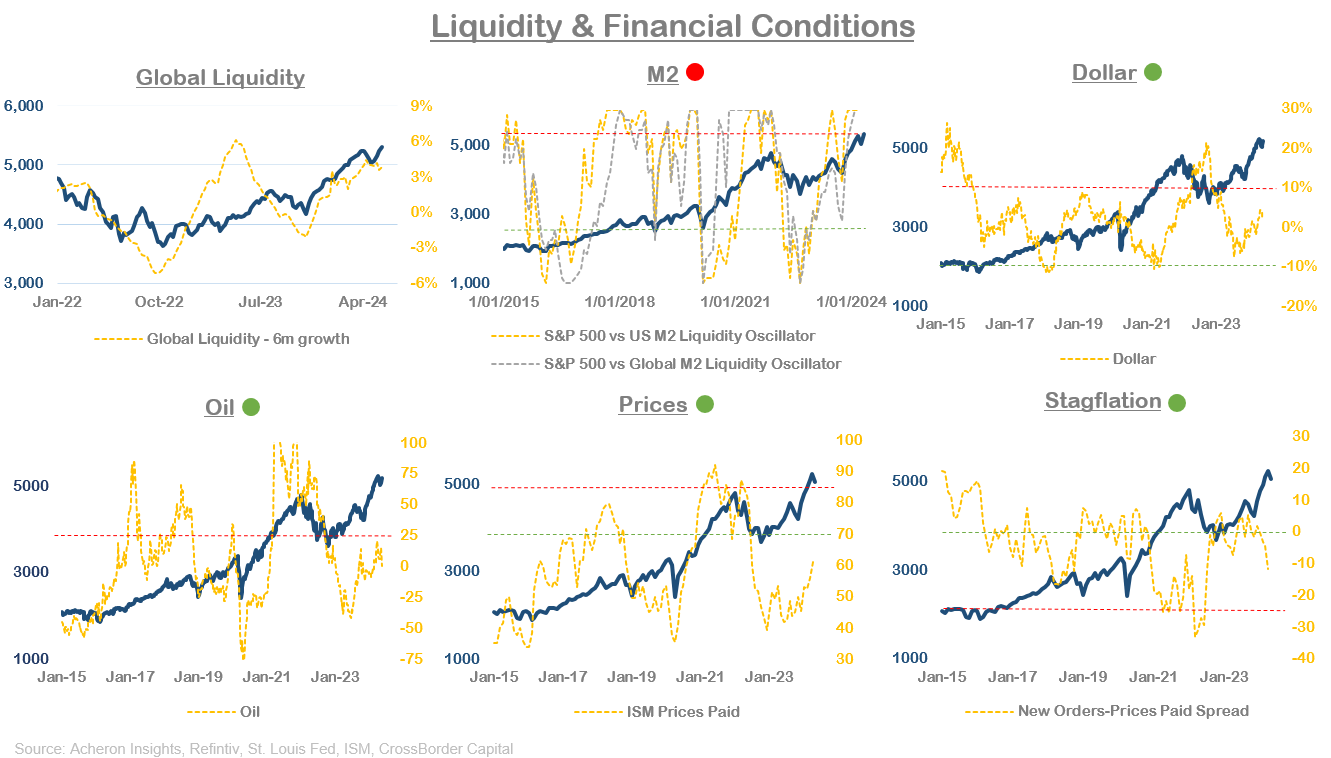

As it stands, financial and liquidity conditions remain largely supportive of asset prices. The dollar, oil, and input prices all remain fairly stable and are far from the worrying levels we saw to start 2022. It is only the liquidity conditions that have turned less favourable over the past couple of months. Still, stocks can remain overbought relative to liquidity for long periods of time.

We must also remember liquidity itself is largely a function of the business cycle. And, as I have been suggesting for some time now, the cycle looks to be in the process of bottoming and turning higher.

With a business cycle expansion comes earnings growth. And it is through corporate earnings which the business cycle drives financial markets.

Through this lens it makes complete sense we saw earnings growth bottom in 2023 and move higher since. And, given the positive outlook economic lead indicators are suggesting for the business cycle in addition to the various earnings growth lead indicators below, we are not yet at a point where earnings growth should surprise meaningfully to the downside.

It is more likely we see moderating earnings growth from here on out. That is, earnings growth will continue to expand and be supportive of equities, just less so than we have seen over the past year.

What is perhaps of more importance is equity markets have priced much of this in. This is true of both earnings growth (per the above) and economic growth (per the below).

Stock markets are naturally forward looking (particularly the long-duration areas of the market such as the Nasdaq), so this pricing in of the robust earnings and growth outlook makes sense.

What we have also seen in recent weeks is the much more economically sensitive areas of the market begin to price in an economic recovery. Copper and industrial commodities as a whole have been the standout asset class of late.

While I expect industrial commodities to continue to benefit from what appears to be a cyclical upturn in the manufacturing and industrial production cycles, speculative positioning is starting to get rather stretched. As such, industrial commodities (copper in particular) are vulnerable for a healthy pull-back from here, particularly if we do see some economic data that disappoints in the coming month or two.

In terms of stock market sentiment and positioning, some measures are looking stretched and some much less so. In relation to overall S&P 500 speculative positioning (inverse of the commercial hedgers positioning chart presented below), we can see commercial hedgers (i.e. the smart money) are currently positioned as bearishly as they have been since early 2022.

Underweight positioning has been one of the primary drivers of equities since the market bottomed in late 2022. Though positioning can obviously become far more stretched from here, this tailwind is now turning to a headwind.

Asset managers are also as bullish as they have ever been, while vol targeting funds are also relatively long this market. On the other hand, hedge funds and CTAs have plenty of scope to add to equity market positions.

I suspect it is unlikely this bull market will reach its ultimate top until hedge funds finally capitulate. We saw this occur briefly in early April. But in the weeks since, hedge fund exposure has returned to near record short levels. This is one area of the positioning complex that remains supportive of the stock market.

Overall however, we are slowly but surely seeing a bullish consensus start to emerge among market participants. Wall Street stock market forecasts are finally turning bullish. And, as we can see below, their doing so generally occurs close to notable market tops. This is not the least bit surprising.

I don’t think we are there yet. But when Wall Street consensus is bullish, you know the easy money has been made.

On a shorter-term basis, we have also seen a notable deterioration in market internals amidst the May rally. Market breadth has been poor, as per my various short-term breadth measures below.

While my market internals models have also failed to rally in conjunction with the market since early May. This has been a hollow rally.

When it comes to divergences between the index and market internals, the broad indices generally play catch-up to the downside. So, unless we see this rally broaden out imminently, we are likely to see sideways price action at the very least over the short-term. The market failing to rally despite the good news that was the Nvidea earnings beat is never a good sign.

And, that we are heading into what is generally a fairly static period of the year to the stock market is further evidence we may be set for a boring few months.

Overall, risk assets are seemingly in a situation whereby they are supported by strong underlying fundamentals, but have priced in a lot in recent times. This likely leaves equity markets and various commodity markets in need of a period of consolidation. I suspect that is probably what we will see over the coming quarter.

Sell in May and go away might prove true once again.

. . .

Thanks for reading!

If you would like to support my work and continue to allow me to do what I love, feel free to buy me a coffee, which you can do here. It would be truly appreciated.

Regardless, feel free to share this with friends and around your network. Any and all exposure goes a long way and is very much appreciated. Thanks again.