The Bull Case For Tanker Stocks

Summary & Key Takeaways:

Following what has been a decade of destruction for the industry, tanker stocks have been in the midst of a renewed bull market over the past 12 months.

There is plenty of reason to believe this can continue, especially for shipowners of Very Large Crude Carriers (VLCCs).

A combination of a low orderbook, increased scrapping of existing vessels and limited capacity for new vessels to be built should see tanker supply strained considerably over the coming years.

Shipyard capacity available for newbuilds is limited until at least 2026, and from there, it will still take a further 18-24 months for new ships to be built and delivered. As such, a significant supply response for VLCCs prior to 2028/2029 seems unlikely.

Moreover, conservative assumptions suggest scrapping of older vessels should at the very least offset any newbuilds over the coming few years.

This creates a potential three to five year period where charter rates can remain at elevated levels, which will see tanker companies flush with cash.

For me, DHT Tankers appears an excellent way to play the tanker thesis at present, as VLCCs appear to have the most favourable supply dynamics and most upside moving forward.

Making the case for tankers

When it comes to investing, shipping is as cyclical a sector as there is. Get the cycle wrong and you’re down 90%. Get it right and you’ll make multiples. It’s global, opaque and filled with nefarious players. This is true of crude oil tankers, product tankers, container ships as well as dry bulkers. Everything bad that can happen to one’s investment has happened in the shipping sector and will undoubtedly happen again.

As is commonplace with the capital cycle, overcapacity and overspending eventually leads to a dearth of supply and collapse in capital expenditures. Through time, bankruptcy and layoffs, the bust eventually plays out. This is exactly what we have seen play out in the tanker industry over the past decade and a half. The early 2000s saw a similar supply setup to today, where scrapping was occurring at the same time orderbooks for new vessels were at or near all-time lows. Couple this with growing oil demand from China, charter rates rocketed higher and stayed relatively high until the late 2000s. In turn, tanker firms were printing cash and with hitting the order button for new vessels en masse.

Unsurprisingly, the supply response was fierce. Order books went from record lows to record highs and hundreds of new tanker vessels were delivered through the 2008-2021 period. Oversupply ensued and crushed the industry. Tankers suffered through a near 15-year bear market, reinforced by the rise of ESG and the shunning of fossil fuel financing.

That is how we ended up with charts like this…

Fortunately, through this decade of destruction as the capital cycle worked its magic, the supply and demand dynamics appear to be shifting in a much more positive direction for the industry. We now appear to be approaching the next boom phase of the tanker shipping cycle that should result in significant revenue and free cash flow generation for those involved.

The supply side

The current investment case for tanker stocks comes down to a simple supply and demand imbalance that should push charter rates higher and remain at a high level for several years. And although demand will play its role in this dynamic, it is primary the supply side of the equation driving fundamentals in a positive direction. A combination of a low orderbook, increased scrapping of existing vessels and limited capacity for new vessels to be built should see tanker supply strained over the coming years.

Orderbook & Newbuilds

What is so captivating of the supply side of the equation is the near-historic low orderbook that exists for clean and dirty tankers, particularly that of the VLCC variety.

While the below chart is somewhat dated, it illustrates well the sectors of floating steel that have been starved of capital (tankers and offshore services/drillers in particular) versus those who have conversely been flooded with capital (LNG carriers for example).

For VLCC’s (Very Large Crude Carriers), the orderbook as a percentage of the existing fleet are at record lows. Compare the current orderbook (circa 5%) to that of the late 2010s (>60%). The shipping boom that occurred during this period has taken well over a decade to sort through.

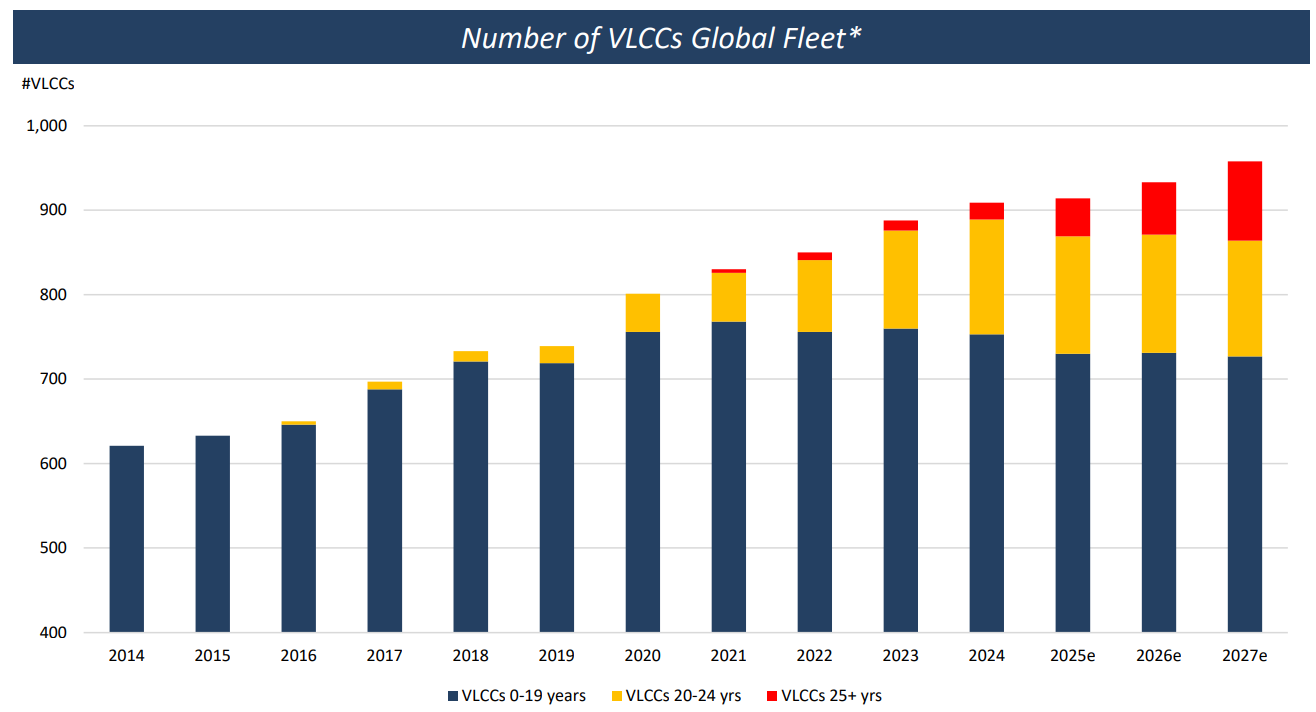

Not only is the outlook for additional supply to be added to the fleet now near historic lows, but the age of the fleet is also reaching levels not seen since the beginning of the 2000s bull market.

This leaves VLCCs in a position where the outlook for supply is limited (roughly 45 VLCCs are set to be delivered between now and 2027) and likely to be offset at least partially (if not entirely) by scrapping of older vessels as the fleet ages.

Scrapping

Over the past five years, the average scrapping age for a VLCC is about 22-24 years. Around 14 VLCCs were scrapped during this period.

Source: MB Shipbrokers

For reference, the below chart provides a quick illustration between the different types of dirty tankers.

Tankers generally have an economic life of around 20-25 years, with the first 15 years of use the most economical. During this initial period, drydocking (the process of inspection, cleaning and repairs) is required every five years. Given the drydocking process can take several weeks to complete and is an expense to the shipowners, it means less revenue generation capacity per vessel. Once a vessel reaches 15 years of age, drydocking is required every 2.5 years, whilst also becoming increasingly expensive as the vessels get older. Though it is from 2017, the below chart from Euronav illustrates the increased costs drydock and survey costs for vessels as they age.

Excluding those within the dark fleet, there are estimated to be approximately 895 VLCCs currently in use, with 40-45 on order and set to be delivered through 2027, as mentioned. Of the current fleet, approximately 15% is already over 20 years of age, while around 8-10% is over 22 years of age.

Source: Frontline PLC

If we were to be conservative and assume an average lifespan on 25 years prior to scrapping, the fleet profile for VLCCs is still quite bullish. A 25-year life suggests we should expect to see approximately 11, 24, 13 and 30 ships scrapped in 2024, 2025, 2026 and 2027 respectively, totalling around 78 ships.

Even if only half those vessels were scrapped, this would likely be sufficient to offset the entire orderbook of new vessels set to be delivered during this period. If we look even further out, between 2028 and 2030, roughly 110 additional vessels will cross the 25 years of age mark, providing a buffer should new build orders pick up over the coming years.

Thus, there is a clear window of three to five years where no supply growth (or an outright contraction in supply) could see charter rates rise substantially for VLCCs. The below chart from DHT highlights this dynamic well.

Source: DHT, Clarksons

It should be noted however, when it comes to scrapping it always pays to be conservative. The 20-25-year economic life for tankers is most likely to be skewed to the upside moving forward for a number of reasons. This is particularly the case as it relates to increased demand for tankers due to Russian sanctions, which saw scrapping in 2023 at record lows and an increased number of vessels transition into the “dark fleet” that is primarily used to carry sanctioned oil from Russia and Iran to the East.

Should we see scrapping surprise to the upside or even the average scrapping age of 22 years remain true during this period, the supply dynamics become even more favourable. Either way, we are likely to see a significant rise in scrapping from 2025 as the number of ships reaching 25 years of age rises dramatically.

Newbuilding capacity

While we will inevitably see a supply response via increased newbuilds over the coming years, the path to newbuilds may not necessarily be as easy as it was during the previous bull cycle. As it stands, shipbuilding capacity is significantly more constrained than is was a decade ago, particularly as it relates to tankers and other offshore oil vessels.

Building a new tanker takes around two years from the initial order to the delivery of the vessel. For VLCCs, newbuild costs are currently ~$130m, while Suezmax’s and Aframax’s cost around $80m and $75m respectively. Product tankers are generally smaller in size and thus are less expensive, with LR2’s, LR1’s and MR’s ranging from $78m to $50m for newbuilds, as we can see below.

Thus, ordering new vessels is expensive and a fantastic way for shipowners to destroy capital and investors dreams along with it.

One dynamic that is likely (if only temporarily) to get in the way of any meaningful supply response is the reduction in shipyard capacity that we have seen over the past decade. The 2010s saw a significant level of overbuilding from various areas of the floating steel market, particularly offshore oil and gas. Not only did the oversupply of vessels lead to a bust in the tankers and offshore sectors themselves, but as these companies went bankrupt, many shipbuilders who had received orders from then bankrupt shipowners become collateral damage and followed suit.

As a result, the number of active shipyards globally is down ~60% from the late 2000s peak.

Source: Himalaya Shipping

In 2011, there were approximately 519 active shipyards in operation. According to Frontline, this now stands at around 247, with South Korea and China having seen the largest reduction in capacity.

What’s more, even if you wanted to build a new oil tanker, not only is the availability of shipyards significantly reduced, but most of the available capacity is being used to build container ships and LNG carriers. In 2021 and 2022, container rates soared as a result of multitude of supply chain issues, and as a result, container shipping companies went on a newbuilding spree. In addition, Europe weening off Russian gas and the build out of US LNG export capacity has also seen a surge in demand for LNG carriers to cater for these new global natural gas supply chains. As a result, newbuild orders for LNG carriers and container ships has surged such that 50% of the global orderbook is being consumer by just these two shipping sectors. This leaves very little capacity for tankers, dry bulk and offshore oil drillers/OSVs.

This means that for at least the next year or two, there is almost now newbuilding capacity for tankers. And, even if we did start to see newbuilds rise during this period, it would take another 18-24 months beyond that to actually build the new vessels. What’s more, shipbuilders themselves are much more interested in building the higher margin and more expensive LNG vessels than simple tankers (or dry bulk, OSV and offshore drillers for that matter). Again, there appears to be a four-to-five year window where tanker rates could go move notably higher before the supply response finally kills the thesis.

Why VLCCs?

So far, I have primarily focused on VLCCs. And although these supply dynamics are largely true for tankers as a whole (both of a dirty and clean variety), VLCCs appear to have the most favourable fundamental outlook moving forward.

There are a number of reasons for this. First and foremost, of the various vessel types, VLCCs have the more favourable orderbook and fleet composition. Compare the ~5% orderbook for VLCCs versus ~11% and ~27% for Suezmax’s and LR2’s. While the supply outlook for Suezmax’s is still very favourable (particularly when looking at the age of the fleet and expected scrapping moving forward), the supply outlook for VLCCs is even better.

Source: Frontline

If we were to rewind 18 months, it was non-VLCC tankers who had the stronger fundamentals. But these tankers (particularly product tankers) have seen a greater supply response over the past 18 months on the back of a rising orderbook and newbuild program (compare the LR2 orderbook above to that of VLCCs and Suezmax’s).

Within the dirty tanker market itself, the smaller vessels in the form of Panamax’s, Aframax’s and Suezmax’s are also much closer to newbuilding parity than are VLCCs, given we have seen a greater move higher in their charter rates relative to VLCCs.

Why have product and smaller crude tanker rates moved faster than VLCC rates thus far and encouraged increased newbuilds of these vessel types as opposed to VLCCs? Well, Suezmax and Aframax vessels have been afforded the additional benefit of geopolitical conflict, which has helped hasten the product and non-VLCC bull market. Sanctions on Russian oil has seen Russia turn to Eastern countries as their primary oil customers (particularly India), which in turn has resulted in more Russian oil transiting the Suez Canal, a route which cannot be undertaken by VLCCs, given their size.

As a result, Suezmax and LR2 rates have appreciated circa 60% and 100% respectively from the 2021 lows, versus a rise in VLCC rates of around 45%.

This leaves the asymmetry within the tanker sector likely tilted in favour of VLCCs, though dirty tankers overall are likely to continue to do well over the coming years, along with clean tankers.

Demand

Although the bull case for tankers is almost entirely a supply story, there are a couple of points worth making from a demand perspective.

Over the long-term, tanker demand is effectively a function of oil demand, and oil demand grows at around 1.5% pa, give or take. I put myself firmly in the camp that oil demand will continue to grow at a similar trajectory for the foreseeable future, and that “peak oil” is a way off. So long as the developing and non-OECD nations wish to grow their economies and quality of life to any kind of close resemblance to OECD economies, energy demand and subsequently oil demand will follow suit. There is a strong relationship between long-term economic growth and energy demand. As emerging economies such as India ascend up their S-Curve, this should well and truly be sufficient to offset the lack of growth amongst OECD economies, and some.

In addition, I do not believe renewables have the capacity to provide sufficient base load energy to supplant fossil fuels in any meaningful way (this is likely a role eventually to be fulfilled by nuclear energy), nor do I believe electric vehicles will be adopted to the degree consensus forecasts have suggested in recent times.

It is important to remember the demand story is not the catalyst for the tanker thesis, while we should expect oil demand growth to continue moving forward, we should only be expecting modest growth (i.e. the continuation of 1.5% pa).

One important area of tanker demand growth we have seen in recent times is resulting from the changing of trade routes over the past few years. We have seen an increase in average sailing distances during this period, through a combination of increased refinery capacity in the East versus the West along with geopolitical conflict within the Suez Canal, which is leading to the need for tankers to transit from Europe to Asia via the Cape of Good Hope, a trip more suited to VLCCs rather than Suezmax or Aframax tankers (VLCCs are too large to transit the Suez Canal). This dynamic has also resulted in an increased use of VLCCs to carry refined products, rather than just crude oil.

These dynamics have helped strengthen tanker thesis, but were never the primary fundamental driver.

What kills this thesis from a demand perspective is a recession, as that will (at least temporarily) destroy oil demand. Now, I think this risk is probably overblown at present, as my macro view has been the trough of the business cycle is likely behind us. That doesn’t mean growth is going to boom from here, but I don’t see the risk of imminent demand destruction as overly high. I suspect the ~1.5% pa oil demand growth we have seen in recent times to continue moving forward.

How to play this thesis

There are a number of avenues investors can participate in this thesis. The listed tanker stocks which I favour are DHT Tankers, Frontline, International Seaways, Scorpio Tankers and Tsakos Energy Navigation.

The below table provides a quick snapshot of each from a balance sheet and valuation perspective, along with the composition of their respective fleets.

Source: Company Reports, Refinitiv, Authors Estimates

The fleets of DHT and Frontline both wholly consist of dirty tankers, with DHT being 100% VLCC’s and Frontline a mix of VLCC’s, Suexmax’s and Aframax’s. On the other hand, International Seaways and Scorpio have a mix of dirty and product tankers (along with other various vessels for Tsakos), while Scorpio’s fleet is made up of various types of product tankers.

Given VLCCs rates not yet appreciated to the same extent as the other vessel types, the performance of DHT has lagged.

DHT Tankers

My preferred company to take advantage of the tanker thesis henceforth is DHT. The reasoning here is simple. DHT’s fleet is made up of 24 VLCCs (with four newbuilds set to be delivered throughout 2026), meaning earnings are fully leveraged the VLCC charter rates. And, as I have detailed, I believe the fundamental outlook for VLCCs has the most convexity moving forward.

DHT appears to be relatively well managed (for a shipping company at least), as management have been buying sporadically buying back shares and pays 100% of net income as dividends. It’s balance sheet is relatively clean with net debt of $324m and debt debt/EBITDA of around 3.9x (which will fall as EBITDA rises). Net debt to equity is a reasonable 31%.

The newbuilds are being funded via a combination of existing cash, future cashflows as well as new debt of approximately $60m per vessels, and are costing an average of $128.5m.

Only four of the existing 24 vessels are above 15 years, with the average age of the entire fleet being only 10.5 years. In addition, the entire fleet is fitted with scrubbers, thus the fleet should largely be able to benefit from premium rates and incur fewer drydocking expenses. Currently, 19 of the 24 vessels are exposed to spot charter rates, with the other five being tied to time charters that will end sporadically over the next few years.

DHT Fleet Summary. Source: DHT

From a valuation perspective, it is true DHT is not necessarily cheaper than its peers on a per ship basis, but it is still relatively cheap outright. Rough estimates suggest DHT currently has an enterprise value of around 0.6x its replacement cost (based on a VLCC newbuild cost of $127m) and 0.9x current market value (based on $110m per ship, which is roughly how much a 10 year old VLCC currently selling for).

In terms of profitability, even at current spot charts (approx.. $50,000/d) DHT is highly profitable. In Q1, DHT printed $84m of adjusted EBITDA at average fleet charter rates of $50,900/d. Given the cyclical nature of the shipping industry, DHT has high operational leverage and thus is highly leveraged to charter rates. Even if charter rates remain at current levels, DHT will remain profitable and continue to print cashflow and provide an excellent yield.

Summary

Over the past decade, tankers and anything related to the oil and fossil fuels industry have been left for dead. These sectors have gone through deep bear markets, been starved of capital, seen shareholders wiped out while bankruptcies have been aplenty. Nowhere has this been more evident than in the tanker industry. But now, we are seeing these companies finally reward shareholders after a decade of capital destruction. The supply side of the tanker and offshore businesses have created a situation where demand is not waning and vessel supply has been so badly constricted rates have nowhere to go but up.

But then again, this is shipping. Anything bad that can happen, will happen.

. . .

Thanks for reading!

If you would like to support my work and continue to allow me to do what I love, feel free to buy me a coffee, which you can do here. It would be truly appreciated.

Regardless, feel free to share this with friends and around your network. Any and all exposure goes a long way and is very much appreciated. Thanks again.