Gold & Silver

Taking a position in gold and silver

As I have discussed previously, ideally I would have liked to see a bit of a correction in the gold price prior to adding to my gold and silver exposure (and entering my initial positions for the purposes of this blog), however, whilst the precious metals have been consolidating their gains throughout April and May, it appears as though they may be about to breakout to new all time highs, and resume the upward trend of this bull market.

Source: StockCharts.com

Whilst I expect to see both gold and silver to test this new found support from above in coming days, both outcomes above appear to be bullish for the precious metals.

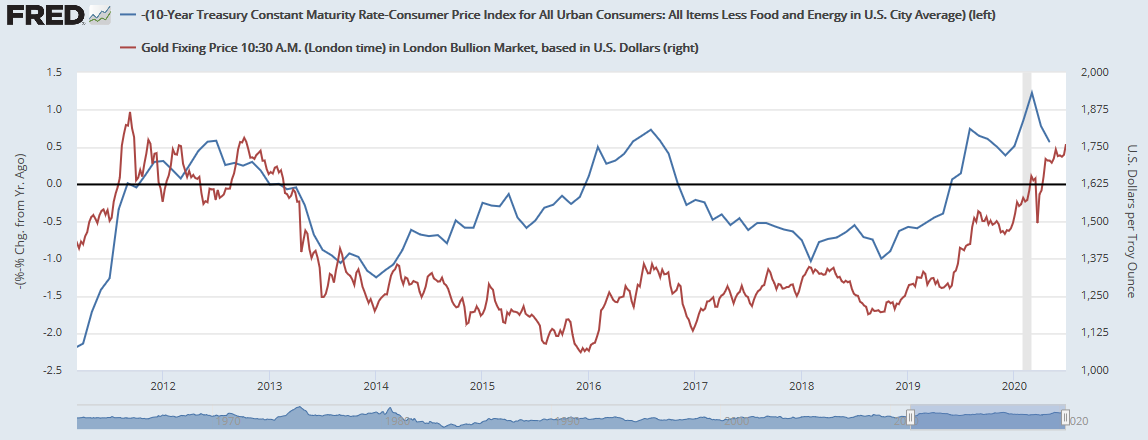

The bullish thesis behind an investment in precious metals is not overly difficult recognise in the todays economic environment. The gold price and the US fiscal deficit as a percentage of GDP hold an inverse relationship. As the deficit expands, the yellow metal has benefited as investors look for a store of value outside of their centrally controlled fiat currencies.

Source: St. Louis Fed

With the move to fiscal dominance we have seen brought on by the COVID-19 crisis, the US government will likely have no choice but to continue their massive fiscal spending in order to avoid further civil unrest, of which is largely been an outcome of the huge wealth inequality in the US.

Taking a look at the ratio of the gold price to the S&P 500 index, we can see that gold broke out of its downtrend relative to equities in mid-2019. Since then gold has outperformed the S&P 500, notably rebounding off its three year support earlier this year.

Source: StockCharts.com

Looking at this relationship over the very long term, there has clearly been periods of time to which gold and equities alternated as the better investment. There has been good times to own gold and good times to own equities. It appears the outperformance of equities over the past decade may have come to an end and the time to own gold has begun.

Source: StockCharts.com, annotated by TheFelderReport.com

Perhaps the biggest tailwind for gold in the coming years is the level of negative yielding debt. Given the fall in interest rates we have witnessed over the past 40 or so years in developed economies, the bull market in bonds appears to be finally running out of steam. Whilst benchmark yields in the US are yet to go negative compared to Japan and parts of Europe, the amount of negative yielding debt has seen a significant rise over the past five years.

Source: Incrementum AG, In Gold We Trust Report 2020

With long-term government bonds historically being the core defensive holding of most portfolios, the risk-reward for bonds is at all time lows given the limited potential price appreciation and historically low coupons. Due to the relatively small market capitalisation of gold compared to the treasury market, any move by institutional investors and pension funds to replace even a fraction of their negative yielding treasury exposure with gold will hugely impact the gold price.

Taking a look at a more technical long-term indicator for gold, the Coppock Curve gave a buy signal in 2017 as this momentum indicator commenced its upward trend.

Source: StockCharts.com

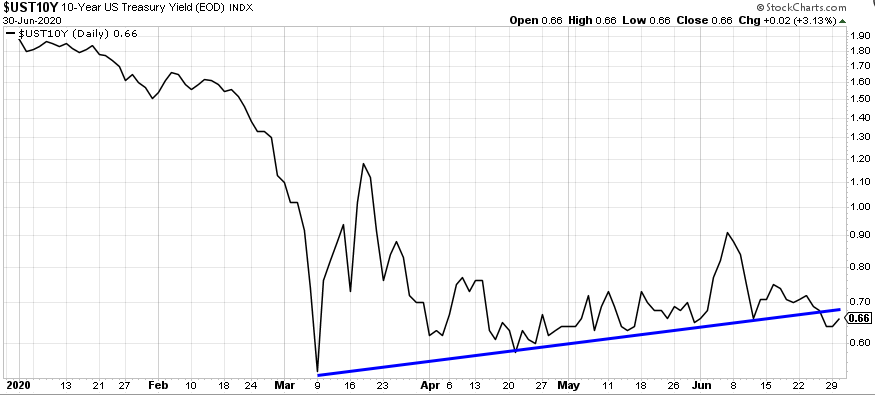

As I discussed here, the price of gold is highly correlated with real interest rates. Given we have seen core CPI fall much faster than rates so far in 2020, real rates have been pushed back into positive territory, something that has historically been a headwind for gold. As such, a correction in the gold price is certainly possible in the coming months, however waiting for such an outcome to take a position during a bull market could be costly.

Source: St. Louis Fed

As you can see above, real yields have diverged from the direction of the gold price of late, primarily due to the fall in CPI we have seen as a result of the deflationary crunch that is typical of a recession. However, a development we have seen over the past couple of weeks is yields breaking down below short-term trendline, a trend that could see falling rates catch up to the fall in CPI and alleviate the pressure being caused by rising real rates.

Source: StockCharts.com

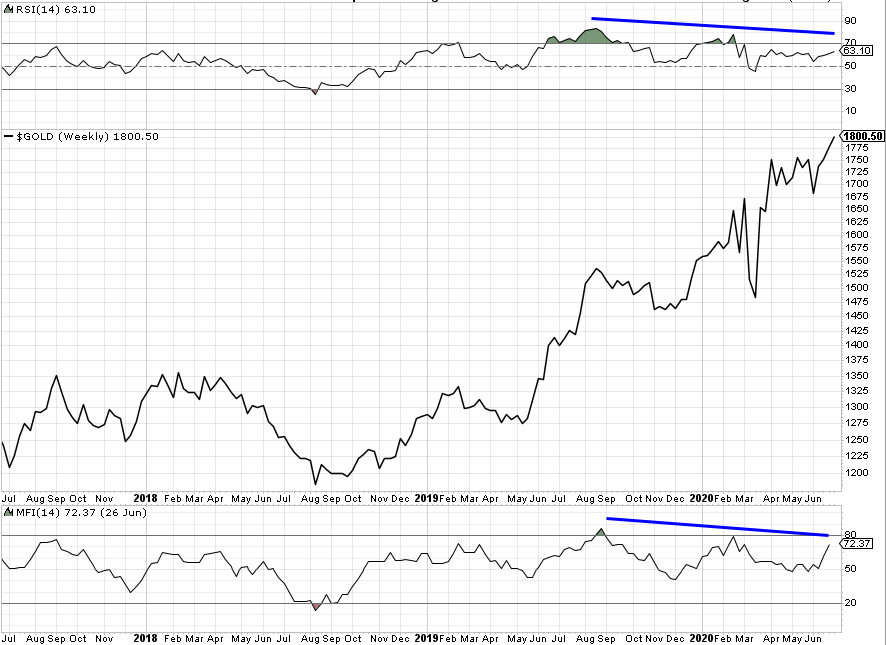

Adding to the potential headwinds facing gold are various short term technical and sentiment indicators. The new highs in the gold price have not been confirmed by momentum (RSI) and money flow. Both have diverged bearishly over the past 12 months whilst gold has continued its rise.

Source: StockCharts.com

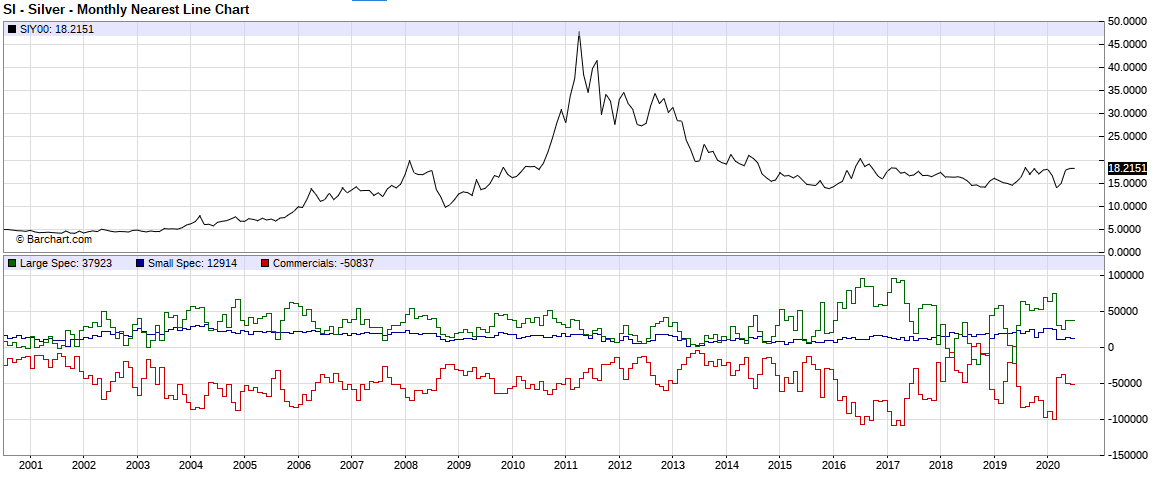

Speculators still hold one of their largest net-long positions in gold we have seen over the past 10 years, indicating that sentiment in the gold is still somewhat too high, whilst this trend is less prevalent for silver.

Source: BarChart.com

However, given we are in a precious metals bull market I would rather use any future pullback in price as an opportunity to add to my positions, rating than trying too hard to time the market.

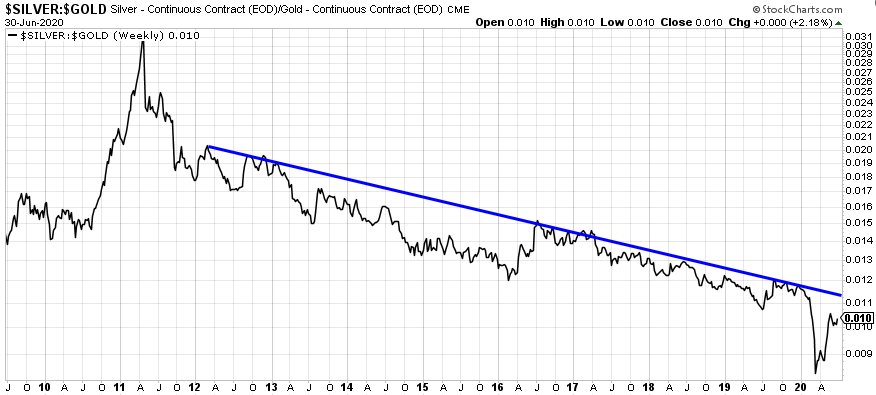

My core positions in precious metals will be in the form of gold and silver, along with a few satellite holdings in the miners. As we have seen in precious metals bull markets in the past, silver and the miners tend to outperform gold. At present, the silver to gold ratio still remains below its long term support that dates back 20 years, nor is the ratio yet to breakout above its downtrend that dates back to 2012.

Source: StockCharts.com

A breakout above this support level has historically preceded a significant outperformance of silver relative to gold. I expect a similar outcome this time around.

Turning to the miners, who are effectively a leveraged play on the price of the precious metal. Relative to the gold price, the gold miners index is not too far above its all time lows, with recent breakouts from its long-term support and medium-term downtrends.

Source: StockCharts.com

Source: Goldchartsrus.com

Similar to silver, the gold miners tend to outperform gold on both the upside, whilst the junior minors tend to outperform the seniors. What makes me more bullish about the miners today relative to previous bull markets in precious metals is the stronger fundamental position the major miners find themselves in today. They have reduce their debts, have cleaner balance sheets and improved profitability, allowing for an increased capacity to benefit from higher gold prices, all the whilst still being at relatively attractive valuations. Another added benefit is many of the miners have recently began to pay dividends to shareholders.

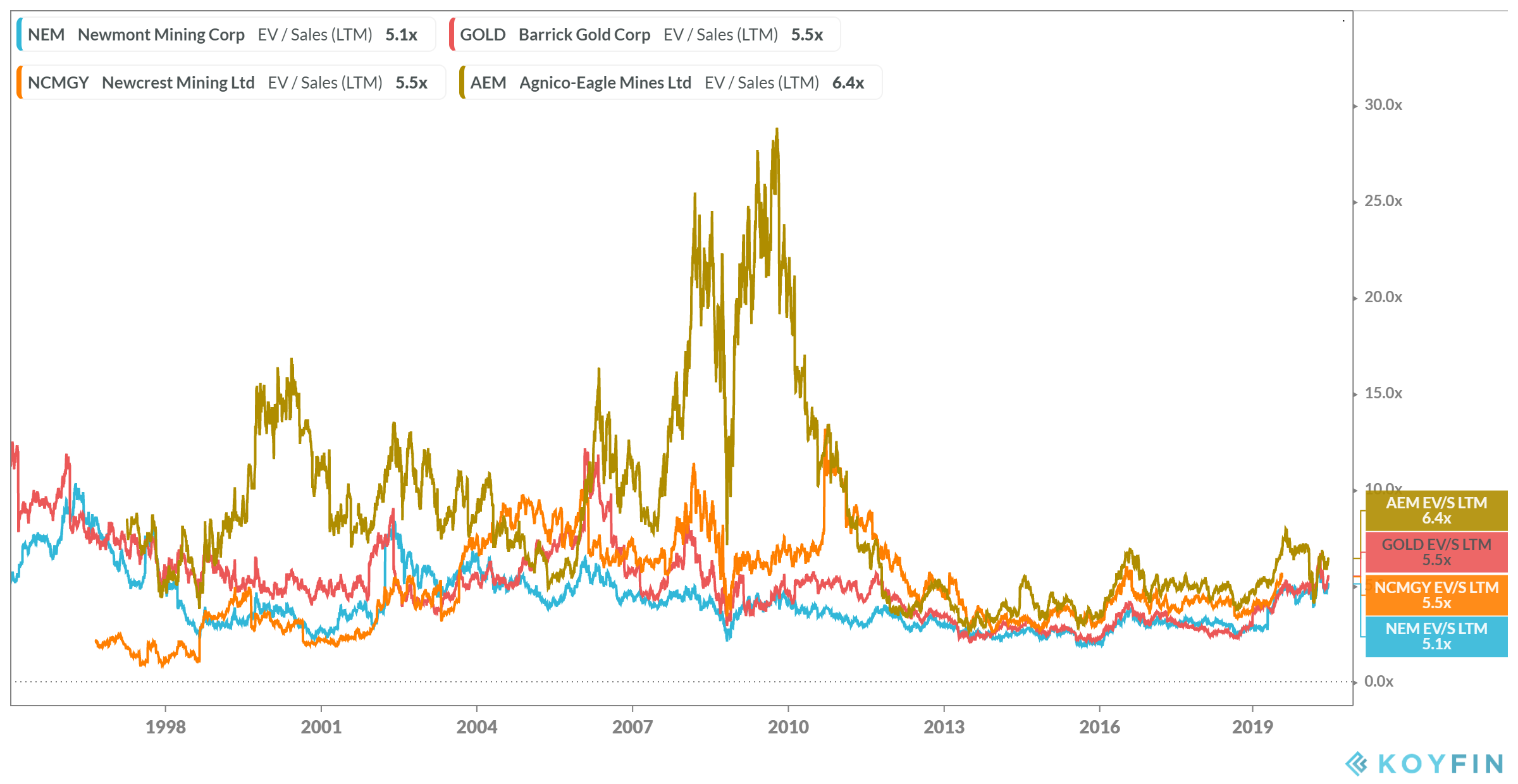

Looking at the EV/sales ratio of the largest of the group, we can see that Newmont, Barrick, Newcrest and Agnico-Eagle are still all relative close to their historical lows in valuation.

Source: Koyfin.com

A couple of final relationships worth considering for the miners are silver miners to gold miners and junior miners to gold miners ratios. Bull markets in precious metals are always confirmed by the mining stocks. The outperformance of the silver and junior minors provides a good trend confirmation indicator, and suggests risk appetites in the precious metals space are increasing.

Source: StockCharts.com

Source: StockCharts.com

A breakout of the above trendlines would suggest an outperformance of the silver miners and juniors miners, similar to that seen in 2016. I would be hesitant to take a position in either at this stage until such a breakout occurs. This is something I am keeping an eye on,

For the moment, given the potential headwinds the precious metals may face in the coming months, my initial positions will be a small holding in gold and silver directly, somewhere between the 5-10% mark respectively. To keep things simple, I will be using the ETFS Physical Gold ETF (GOLD.ASX) and ETFS Physical Silver ETF (ETPMAG.ASX). For the miners, again to keep things simple, I will utilise the BetaShares Global Gold Miners ETF - Hedged (MNRS.ASX), and will be allocating a 5-10% exposure at this time. In this case I am happy for the hedging overlay provided by this ETF, given the unhedged exposure of the gold and silver ETFs mentioned.

In regards to entering these positions, I will begin doing so over the next couple of weeks, at which point in time I will update this post below. All trades will be reflected in the portfolio.

Update: 7 July 2020

On Friday 3 July 2020 I added a 5% exposure to the MNRS ETF, a 5% exposure to the ETPMAG ETF and a 7.5% exposure to the GOLD ETF. These trades are now reflected in the portfolio. I intend to write an update in the future to discuss why I have used these specific ETFs over the others that are available in the precious metals sector.

Update: 16 July 2020

Its appears as though the junior minors may have broken out of their downtrend relative to GDX.

Source: StockCharts.com

Given this development, I have added a 5% exposure to the GDXJ ETF to take advantage of the potential outperformance the junior minors may afford as part of this gold bull market.

Update: 22 July 2020

The silver miners ETF has now too broken out of its downtrend relative to the gold miners. This follows on from an explosive move from silver seen over the course of this week.

Source: StockCharts.com

I’m adding a small exposure to the SIL ETF, around 2.5% or so. This leaves me with about 20% of my entire investment portfolio invested in precious metals, in the form of the miners and the metals themselves. I am invested fairly defensively elsewhere so am happy to have such a large position given how bullish I am on the sector. I will look to add to my positions amid any pullbacks we may have in the near future.