Energy Is Breaking Out: Is It For Real?

Since the Fed’s September FOMC meeting and official taper announcement, we are witnessing what appears to potentially be a shift back into the reflation trade. With the bond market reacting to the announcement by selling off sharply, yields look to be trying to now price in inflation. A clear repricing of those assets who benefit from higher yields has been evident. Despite much of the leading data suggesting economic growth looks set to decelerate over the coming months, it’s important to remember that, when the bond market makes a move, it is generally the right move and investors ought to pay attention.

Indeed, on the back of rising yields and a steeping yield curve, one of the biggest beneficiaries of this shift has been the energy sector, namely oil and oil related equities. With crude oil leading the charge, the energy sector looks to be breaking out of an important technical resistance point, a potentially bullish outcome for the immediate future.

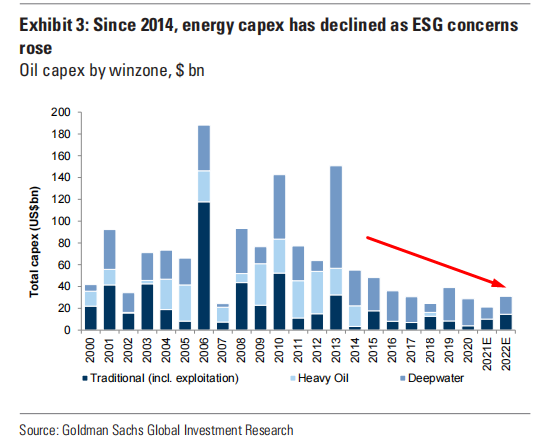

The fundamental case for crude oil and energy related equities, particularly in the exploration and production space, remains as bullish as ever. The sector has been starved of capital since 2014 and is a trend set to continue for the remainder of 2021 and 2022 at the very least. Ever increasing ESG pressures will only exacerbate this dynamic over the coming years. The energy sector remains one of my favourite trades for the next few years.

Source: Goldman Sachs

Combined with attractive valuations on both a relative and absolute basis, the stage is set for a continuation of this bull market. Indeed, with the energy sector still only representing around 3% of the S&P 500 index, despite having appreciated roughly 150% since March 2020, plenty of upside potential remains.

Thus, as long-term investors bullish the sector this begs the question; is this breakout the catalyst for the next move higher?

While breakouts above well-defined horizontal levels of resistance are inherently bullish and represent excellent opportunities to trade tactically, of the many indicators I monitor not just technical but from a sentiment, fundamental and macro perspective, the signals are mixed.

What is encouraging when looking at the market from a longer-term perspective is how commercial crude oil hedgers (i.e. the smart money), have reduced their short positions in the futures market to the lowest point since early 2020, as illustrated below. Producers themselves are now fully net long (not pictured), an encouraging development as the producer hedging position is most often short rather than long. Producers use the futures markets primarily as a means to hedge downside risk against falling oil prices. In addition, the managed money futures positioning (not pictured), consisting primarily of hedge funds and CTA’s, also have their smallest net-long positions since March 2020. It pays to fade managed money as these market participants are effectively just trend-followers, and are thus routinely long at market tops and short at market bottoms.

Source: SentimenTrader

However, as you will note above small speculators remain heavily net long, clearly illustrative of investors betting on a continuation of the reflation trade.

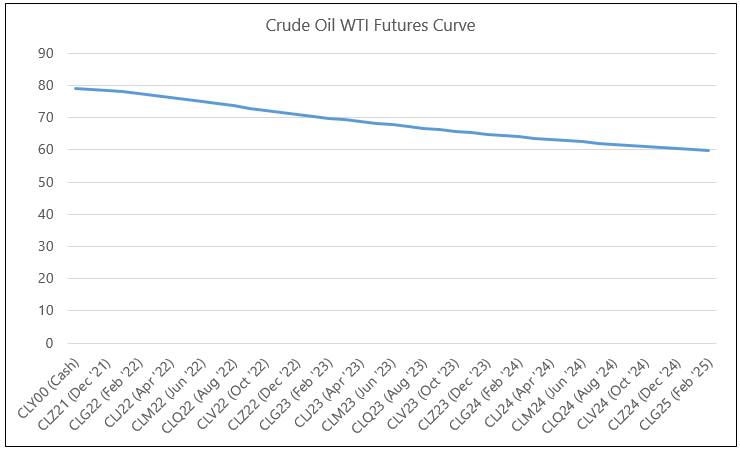

The futures curve itself remains in state of backwardation, a situation whereby the prices of the shorter-dated contracts exceed the longer-dated contracts. The futures term structure is by no means a predictor of future prices, but rather is reflective of supply and demand within the oil market. A state of backwardation as we are in currently is representative of a deficit, meaning demand for immediate delivery exceeds immediate supply. This has been the case for most of 2021.

Source: BarChart, Acheron Insights

The shape of the term structure is a very useful tool to assess the underlying fundamentals within the market. Backwardation implies a deficit, resulting in inventories needing to be drawn down to meet demand. This is the opposite of what occurred in March 2020, where the short-dated contracts went negative in a state of steep contango, reflecting the worldwide evaporation of demand induced by the initial COVID-19 lockdowns. The majority of gains within the energy markets come when the curve is in either backwardation or falling contango.

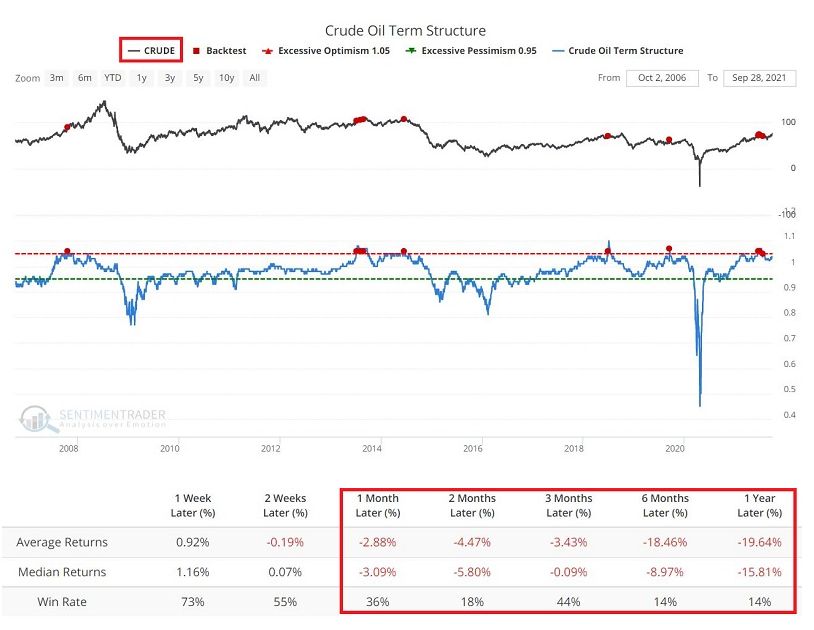

However, it is during times of falling contango whereby the most impressive returns in energy markets take place. In fact, as noted recently by SentimenTrader, backwardation is more closely associated with periods near market tops, with six to 12 month subsequent returns historically negative.

Source: SentimenTrader

Although it must be said this analysis has very little bearing for the immediate future, as the curve will likely shift from backwardation to contango prior to such market pull-backs, hopefully providing a decent warning signal in advance. For now, the backwardation of the term structure in the futures market is supportive of this recent breakout.

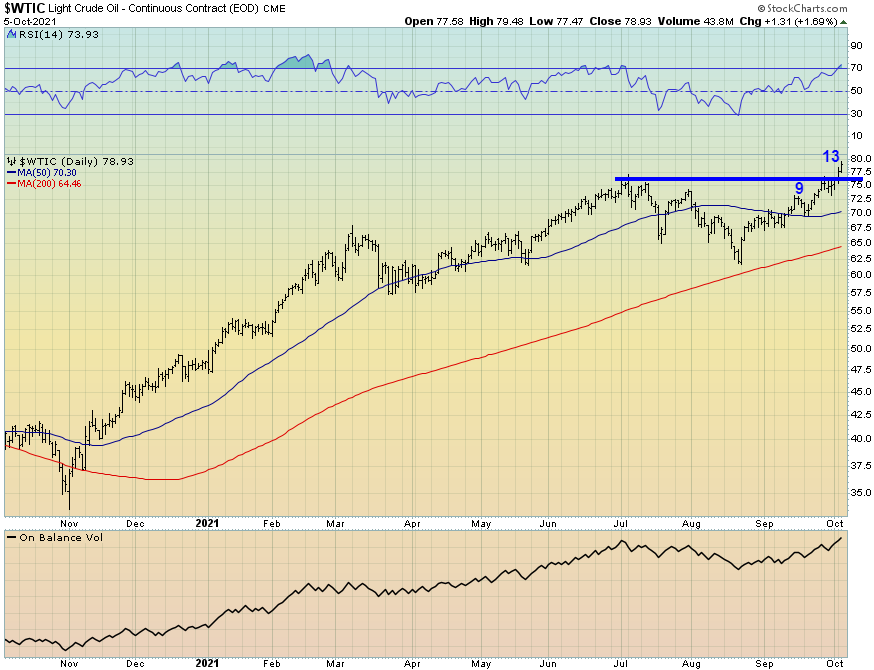

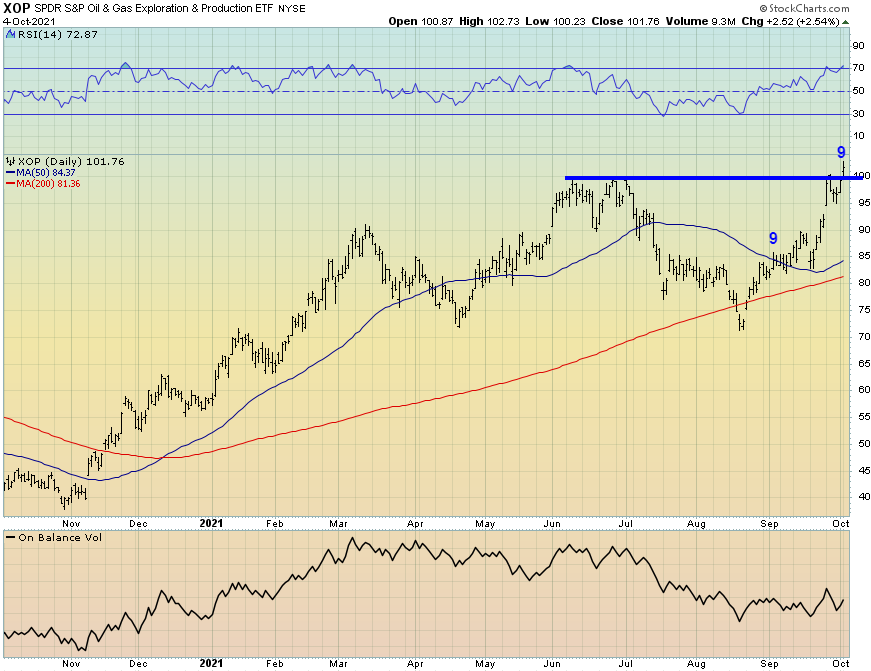

Turning now to the technicals, as we can see below the breakout in crude has been accompanied by daily DeMark 9 and 13 sell signals, a sign of potential trend exhaustion.

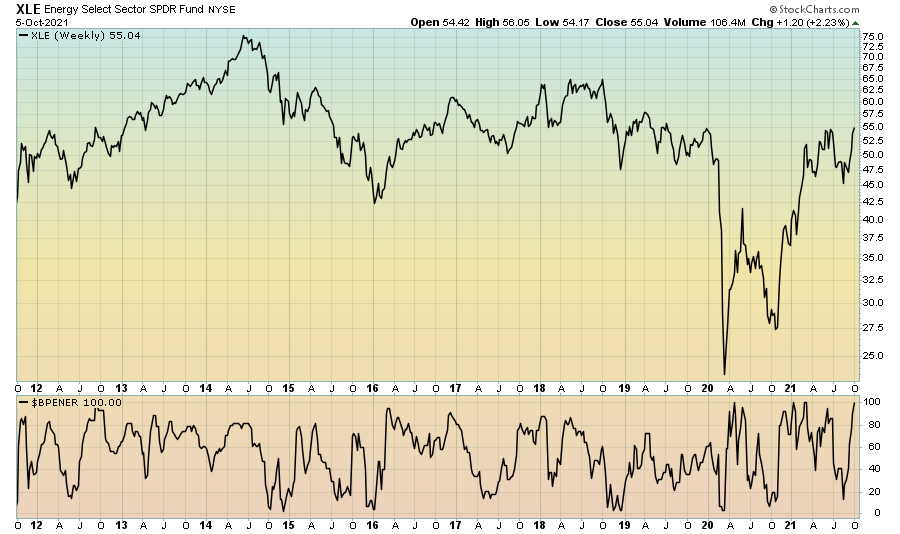

It’s hard to argue this clear breakout is not bullish from a pure technical perspective, though we are yet to see the broad energy stocks follow the path of crude. The XLE energy sector ETF is sitting right at a level of strong overhead resistance. A close above 56 would be a bullish outcome and a confirmation of the breakout in crude.

The XOP ETF however, appears to be confirming the bullish breakout in oil. This in unsurprising, as XOP contains the oil and gas exploration and production companies whose price action resembles somewhat of a levered play on oil itself.

Whilst the fundamentals are strong and the technicals potentially looking bullish, not every indicator is confirming this breakout. Firstly, we are on the precipice of the worst performing months for crude oil historically. Whilst I would never base my investment decisions off seasonality alone, as my preference is to utilise a holistic approach combining fundamentals, technicals, sentiment and macro, one thing is for certain, going long crude oil in Q4 is one fraught with danger historically.

From a sentiment perspective, investors have gone from pessimistic to outright euphoric in a matter of weeks. We can see this by looking at the energy sector Bullish Percent Index ($BPENER), which is maxed out at 100.

And by looking at the XLE Optimism Index (Optix).

From a growth cycle and macro perspective, energy stocks and oil are best suited to environments of accelerating growth, ideally accompanied by accelerating inflation. Stagflation on the other hand is not an environment in which crude oil or energy equities have performed well historically, nor in one of disinflation. Whilst inflation may well continue to accelerate on a rate of change basis throughout the remainder of this year, what is evident is the leading indicators of the economic growth cycle are still pointing towards a deceleration in growth over the near term. I discussed this in detail within a recent post. Confirming this message is the Atlanta Fed’s GDPNow forecast for real GDP growth for Q3. This estimate has again just been revised down to a 1.3% annualized quarter-over-quarter growth rate of real GDP from 3% only last week.

Source: Atlanta Fed

As a result, we are beginning to see divergences emerge between the performance of energy and several growth related market indicators that are not supportive of the recent positive price action. Firstly, the dollar has continued to rally despite bonds selling off over recent weeks. As the dollar and energy are very much negatively correlated, one will catch up with the other at some point.

Could it be the dollar is confirming the message of slowing growth? Seasonality is suggesting this may be the case.

Source: SentimenTrader

As is the copper-to-gold ratio, another historically good indicator for assessing the current macro environment. This ratio is yet to confirm the breakout in energy and has continued to make lower highs since May.

While the bond market and various equity sectors are looking like they are trying to price in a resumption of the reflation trade, the leading growth cycle indicators are yet to follow suit. Given the bond market in particular generally gets things right, it may well be the case that we see energy prices continue to March upwards throughout the final months of 2021.

However, until we see a pickup in growth reflected in the leading data and with the potential macro headwinds and euphoric sentiment towards the energy sector at present, it’s hard to see this breakout as more than a potential trading opportunity from a tactical perspective for the time being.