Economic Growth Outlook: The Slowdown Continues

As I have discussed in a number of recent posts, leading economic data continues to suggest a cyclical slowdown in the business cycle is upon us and is likely to continue to persist for the coming months. Furthermore, a continued slowdown in growth may precipitate a deceleration in the rate of change in inflation, indicating a transition from a stagflation macro regime to that of outright disinflation, whereby both inflation and growth decelerate together. As such, investors would do well to position their portfolios in a defensive nature and reduce risk, particularly with the notion of the likely tightening of monetary stimulus by the Federal Reserve on the horizon.

Leading Indicators: Credit Creation

Beginning with what is perhaps the best indicator of growth potential in the real economy, as opposed to just the financial economy, the G3 credit impulse is now firmly in negative territory after peaking in the latter stages of 2020.

Source: Nordea

Credit impulse is a measure of the rate of change of new credit creation as a percentage of GDP, with the G3 measure above incorporating this data from the US, China and Europe. Unlike pure monetary measures such as the M2 money supply, credit creation measures the rate of change of credit creation in the real economy, via commercial bank lending and fiscal deficit spending, and thus acts as a far better tool for predicting real economy growth. Credit impulse is effectively a leading indicator for just about everything, usually by about 10-12 months.

Confirming the message of the credit impulse is Chinese bond yields, which themselves are an excellent leading indicator of the worlds business cycle. China remains the worlds largest manufacturer and drives much of the worlds business cycle. Similar to their credit creation, Chinese yields have been trending lower since their short-term cyclical peak in December 2020.

Source: Trading Economics

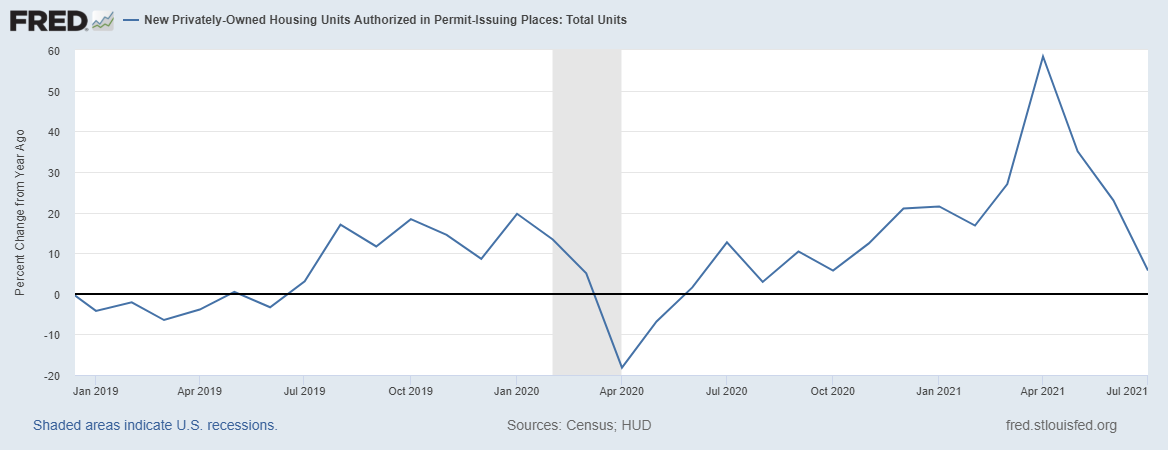

Leading Indicators: Construction

Turning to manufacturing, building permits for new housing have been decelerating in a year-over-year rate of change basis at an alarming rate since April.

A reduction in building permits is indicative of slowing growth in the housing and construction sector as building permits precede the construction of new housing and indicate lessening demand.

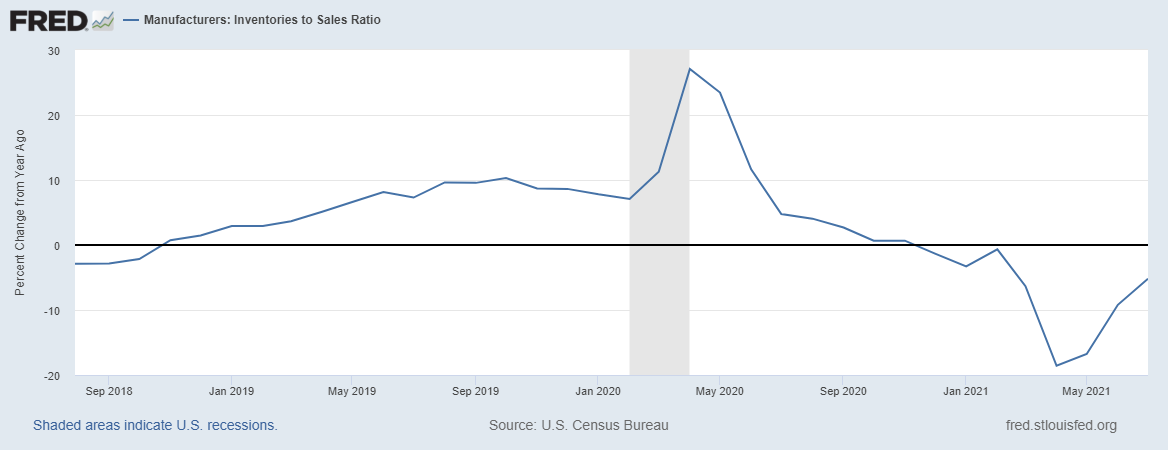

Leading Indicators: Manufacturing

So too confirming the deceleration in growth is the manufacturing sector. The US Census Bureau’s manufacturing inventories to sales ratio continues to trend upwards to nearly positive on year-over-year rate of change basis.

When sales are rising at a greater pace than inventories and the ratio falls, then more inventory needs to be produced, thus putting upward pressure on prices, as well as an increased need for workers and hours worked. When inventories rise at a greater pace then sales, the inverse occurs.

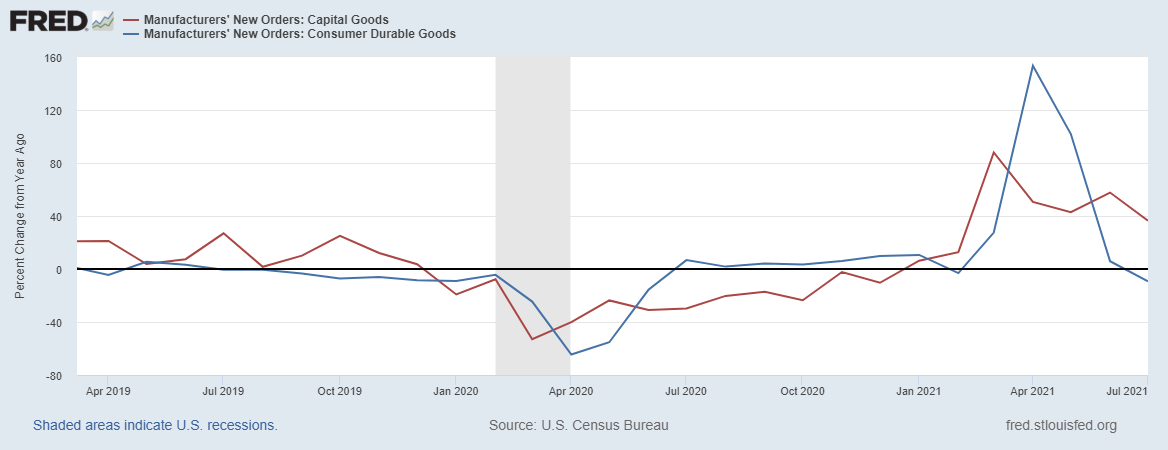

We can extrapolate this further by focusing on the Census Bureau’s data of new manufacturing orders, which continues to decelerate after peaking in April this year. As new orders are very demand sensitive, a deceleration in the data clearly indicates a slowing of growth in the manufacturing sector.

Again, we can extend this further to see both the growth rate of new orders of durable goods and capital good peaked in the March to April 2021 period and are decelerating. Both metrics provide a good lead on the short-term direction of the economy.

Of the US ISM Manufacturing Index, supplier delivery times is another leading indicator with important consequences, as this measure gives us a good read on supply chain disruptions in the manufacturing sector. Like with the manufacturing data presented above, supplier delivery times according to the ISM Manufacturing Index participants have been trending lower since May.

US ISM Manufacturing Supplier Deliveries Index

Source: YCharts

Unsurprisingly, as manufacturing demand and delivery times begin to trend downward, we are seeing the ISM Manufacturing Prices Paid index too begin to trend downward. As supply constraints lessen and demand decelerates, it is unsurprising to see prices paid follow suit. As these ISM readings trend lower, it tells us that fewer executives in the manufacturing sector are facing supply constraints and price increases relative to the previous month.

US ISM Manufacturing Prices Paid Index

Source: YCharts

Industrial commodities are too confirming this message. Although they remain elevated on a nominal basis, the growth in prices for industrials commodities is clearly decelerating.

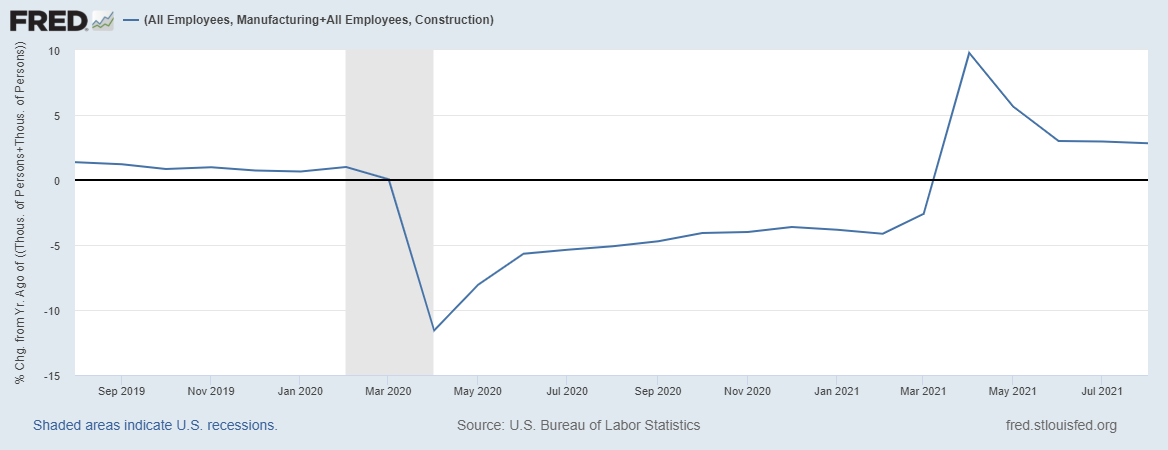

The same can be said for employment in the manufacturing and construction sectors. The aggregate data of both peaked in April on a year-over-year rate of change basis and have been decelerating since.

Leading Indicators: Consumer Demand

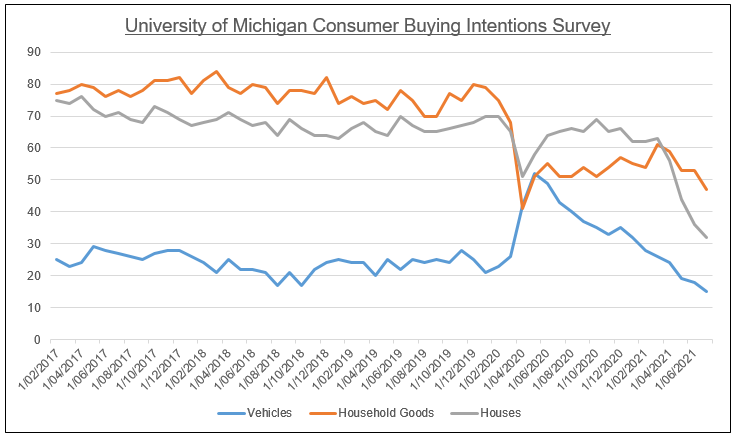

From a consumer demand perspective, the University of Michigan Consumer Buying Intentions Survey for vehicles, houses and household goods all remain near their lowest levels in some time. The spike in inflation over the past number of months is clearly impacting consumer demand for goods. Evidently, demand is not only waning in the manufacturing and construction sectors but in households too.

Source: Acheron Insights, University of Michigan

Other Leading Indicators

Turning now to several broader leading indicators of economic growth, the growth rate of Economic Cycle Research Institute’s (ECRI) weekly leading index continues to decline following its April peak. As noted by ERCI, this composite index generally leads cyclical turning points in the economy by 2-3 quarters.

Source: Economic Cycle Research Institute (ECRI)

The Citibank Economic Surprise Index remains firmly in negative territory. This index measures the level of economic data coming out better or worse than expected, and thus, when in negative territory is indicative of more economic data releases disappointing to the downside rather than surprising to the upside.

And finally, SentimenTrader’s Macro Index Model recently triggered a sell signal. This index combines 11 economic indicators to determine the current state of the US economy (with a focus on the housing market and labor market), of which the indicators are; new home sales, housing starts, building permits, initial claims, continued claims, heavy truck sales, the yield curve, the S&P 500 relative to its 10 month moving average, the ISM manufacturing PMI index, margin debt and year-over-year headline inflation.

Coincident Indicators

Confirming the trends of the leading economic indicators I have detailed above are the coincident economic indicators. Whilst not necessarily useful in predicting changes in the business cycle, they are important data points that define and confirm the trends in economic growth.

We can see the growth in total non-farm employment confirming the cyclical growth peak in April.

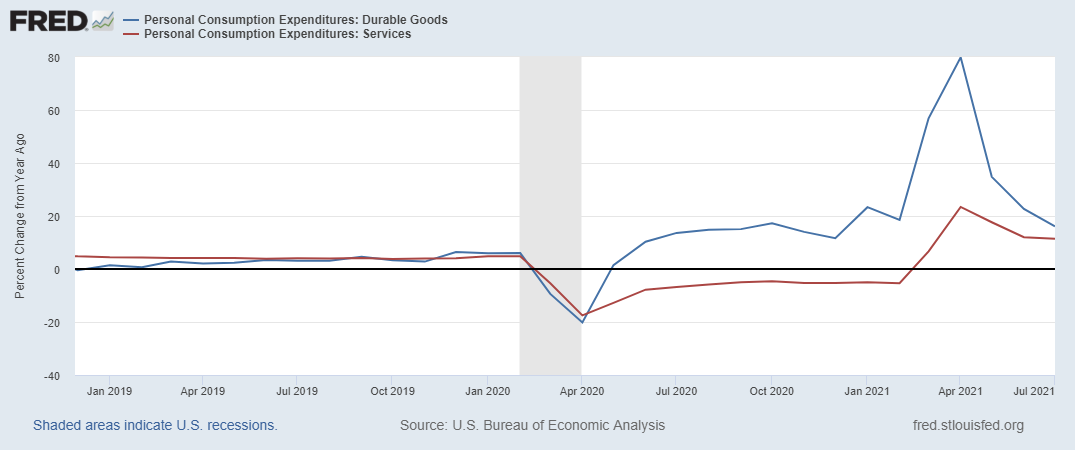

The same can be said for personal consumption of both goods and services.

Whilst we would expect to see the growth rate of goods consumption slow as the lockdown induced spike in the consumption of goods was always going to be unsustainable once the economy began to reopen, a deceleration in goods consumption coupled with the decelerating growth in services consumption seemingly confirms the message of a slowdown in the business cycle.

Financial Market Performance

Turning now to financial markets, as I have noted previously, some of the most cyclically sensitive sectors of the stock market have very much confirmed the growth cycle story outlined above. The relative performance of the retail, transports, metals & mining, materials and industrials sectors compared to the S&P 500 all peaked during the first half of 2021 and have underperformed since.

As growth accelerates, you would expect to see these cyclical sectors outperform, and conversely, when growth decelerates you would expect to see them underperform, as has been the case over the preceding few months.

In addition to the stock market sectors confirming the downward trend in growth, we can see other market performance data sending a similar message. Stocks relative to bonds, commodities relative to stocks, copper relative to gold and lumber relative to gold have all largely underperformed since the first half of the year. Should growth continue in its current downward trend over the coming months as the leading data suggest it might, we ought to expect these relative market performance trends continue.

Taking a closer look at the performance of stocks relative to bonds, we can see that aside from the Nasdaq and the mega-cap growth names, stocks have largely underperformed relative to bonds in recent months. Again, this is indicative of a slowing growth environment.

And finally, the various iterations of the yield curve continue to remain well below their peaks in March earlier this year. The bond market continues to price in a slowdown of the economy as well as a deceleration in inflation.

Portfolio Positioning & Asset Allocation

It is important to remember from an asset allocation and portfolio positioning point of view that it is the direction of the rate of change in growth that matters. As growth and credit creation accelerates, it is important to position your portfolio towards the business-cycle sensitive equity sectors and asset classes expected to benefit in such conditions. Similarly, as growth and credit creation decelerate, it is those business cycle sensitive equity sectors and asset classes who are likely to underperform.

As of right now, the leading economic data suggests we are now firmly in a period of decelerating growth, coupled with the likely cyclical peak in inflation. Although inflation pay persist at higher levels on a nominal basis for some time yet, from a rate of change perspective, we are likely to see a deceleration in CPI going forward.

Source: Acheron Insights, BIS, OECD

As such, investors will do well to position their portfolios towards assets most likely to benefit from a deceleration in credit and growth, and underweight assets that are unlikely to benefit in such a scenario. Risk management is ever so important during such times.

Source: Acheron Insights

With the probabilities indicating the slowdown in economic growth is likely to persist for the coming months, investors should do well to adjust their portfolio allocations accordingly in order to ensure their portfolio’s downside risk is limited, whilst also being prepared for what opportunities a potential continued slowdown in growth may provide.