Crypto Market Outlook: A Potential Bounce May Be Imminent

What has been a tumultuous last few months for crypto markets has only accelerated through the turn of the New Year. Several of the key support levels for both Bitcoin and Ethereum I highlighted in my initial crypto market outlook have since been breached and unsurprisingly ushered in further negative price action to the downside. Bitcoin now resides on what can only be described an incredibly important level of support at $40k-$42k. For dip-buyers and long-term holders alike this is almost a must buy level as its importance as both resistance and support throughout 2021 has been paramount and thus could well be a level Bitcoin consolidates and bounces from. However, as I will cover off within this article, not all of the signs are there for a meaningful market bottom.

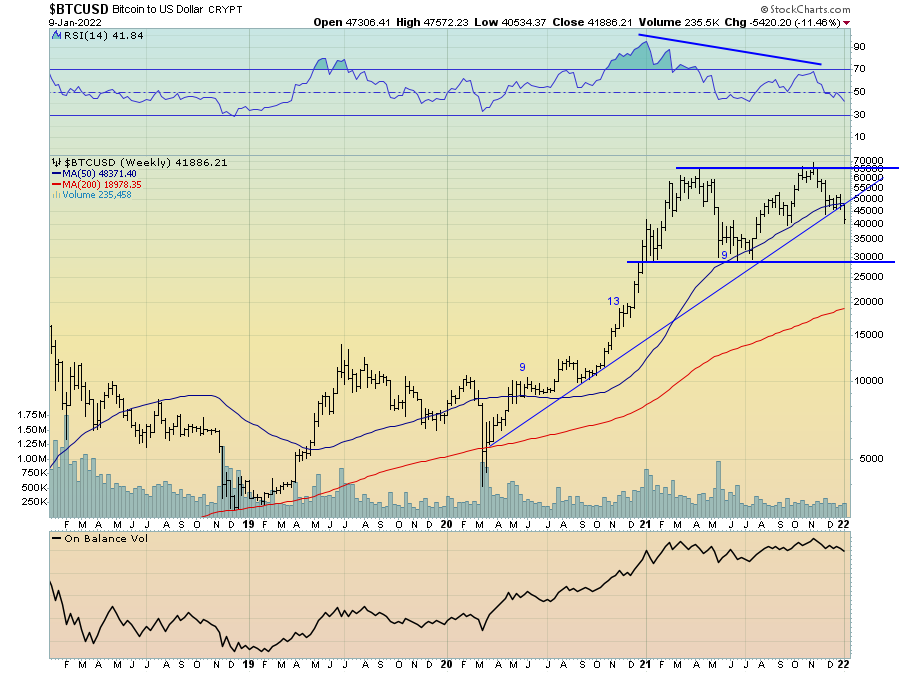

Beginning with the long-term technicals for BTC per the weekly chart, what is of concern is the recent price action has taken us meaningfully below the 50-week moving average. This moving average has provided key support since the mid-2021 lows and any meaningful close below would be the first since March of the 2020. By simply examining the weekly chart it looks as if we could easily see the price fall back to the $30k area. If we do enter a sustained bear market for crypto in the latter parts of 2022 I would not be surprised if this level is reached. Such an outcome would not doubt provide an excellent long-term buying opportunity for those bullish digital assets.

What also concerns me regarding the recent price action is we are yet to see a spike in downside volume that would usually accompany downside capitulation representative of a sustainable bottom. Although we have seen such volume spikes to the downside in all meaningful market bottoms over recent years, it must be said of course that bottoms can form without such movements in volume. This is certainly is something investors should keep an eye on nonetheless.

Shorter-term, BTC finally lost its 200-day moving average after back-and-forth price action in recent weeks, ushering in a swift move down to $41k. As I mentioned earlier, we can see below how important this level has been for over 12 months, flipping between support and resistance on a number of occasion. I have highlighted such points on the chart below for reference.

Given its obvious importance from a technical perspective, this level provides a simple and attractive opportunity to structure a long trade with a clear stop below $40k. Should we indeed break meaningfully below $40k, $30k looks all but inevitable.

Turning now to Ethereum, the story is largely the same as Bitcoin, with $3k marking an excellent buy-the-dip opportunity but a break below opening the possibility of a fall down to as low as the $1,700 area.

To become more bullish on Ethereum in the short-term, I would love to see the 200-day moving average retaken in short order similar to what occurred in late-June and early-July of last year.

That being said, the recent price action of the ETH/BTC spread does not look favourable to me for Ethereum in the short-term. Unless the 0.08 resistance level can be retaken, what we may have witnessed was a false break above this level in December and a reversal to the downside, pointing to further Bitcoin outperformance going forward. This would either playout with Bitcoin outperforming to the upside which would be constructive for the overall market, or Bitcoin outperformance to the downside, not an ideal outcome for altcoins and riskier digital assets.

Though we currently reside at important levels that can easily be bought, not all the technical signs are there for a meaningful market bottom to be in place. Ideally, I would like to see a spike in downside volume along with bullish divergences in such indicators as the RSI and OBV (On Balance Volume) confirming the bottom is in, particularly so for the latter.

Turning now to investor sentiment, we are evidently nearing levels of extreme market fear. We can see this via the Crypto Fear & Green Index.

And Bitcoin Optix.

Whilst we are nearing levels indicative of buying opportunities in the past, the issue with sentiment measures for crypto markets is they have historically displayed a momentum effect, in that positive investor sentiment is indicative of positive price performance over the short-term and vice-versa. As such, though the Fear & Greed Index is low, it could well go lower or remain low for some time as price continues to fall. This is why I have used the 10-period moving average for the Optix index as it appears to provide a more accurate contrarian buy or sell signal.

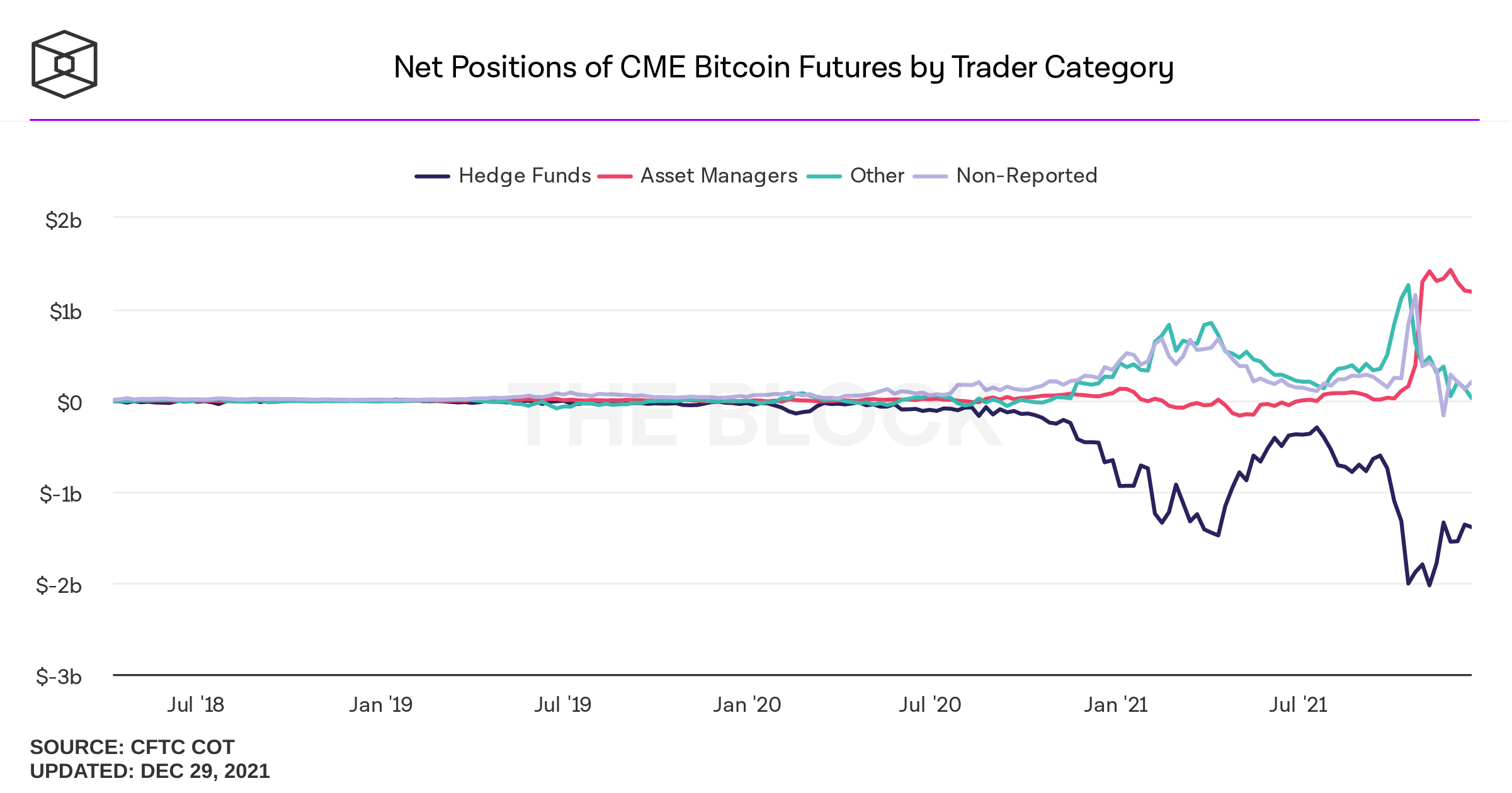

We can also assess sentiment through the lens of the futures market positioning in both Bitcoin and Ethereum. In the crypto futures markets, hedge fund activity differs to that seen in traditional asset futures markets as have thus far acted as the smart money and thus tend to be short at the market tops and less-short at the market bottoms. The other and non-reported categories (representing the dumb money, i.e. small speculators) seem to be long at the tops and less-long at the bottoms.

Hedge-funds are still heavily net-short, although the Other and Non-Reported categories appear to be reaching more favourable levels.

Source: TheBlockCrypto.com

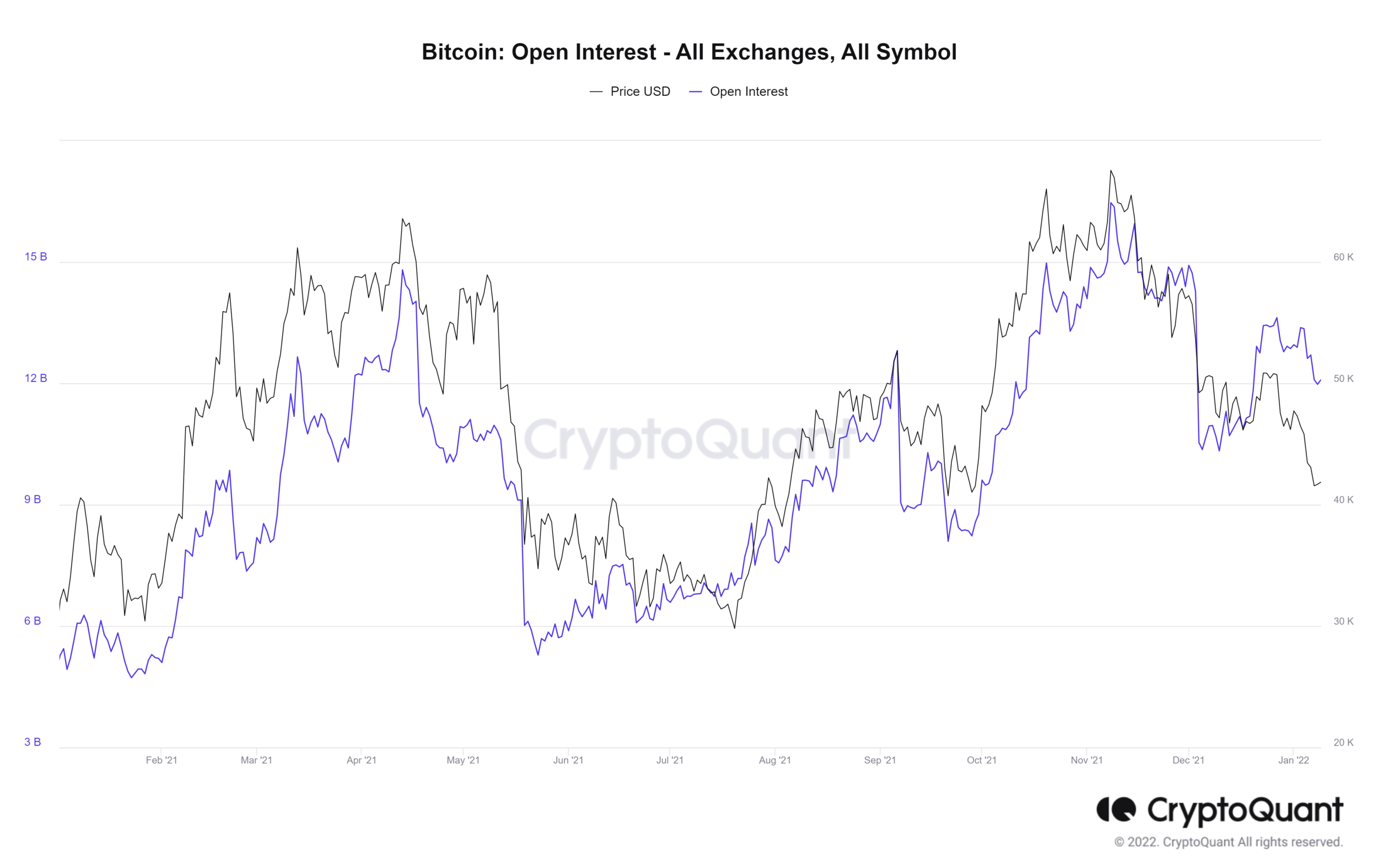

In terms of open interest for all derivatives for Bitcoin and Ethereum, BTC open interest still remains elevated relative to the recent price action. We saw an excessive drop in leverage as open interest fell significantly in early December along with price. Since then, whilst the Bitcoin price has continued to make a new low, open interest has instead made a new high, positively diverging from price.

As I have noted in the past, it is important to remember however this open interest data for Bitcoin is being influenced by the introduction of the Bitcoin futures ETFs in recent months. As the futures market is generally used for traders of a short-term time frame due to the excessive roll costs associated with holdings futures contracts for long time periods, buyers of the Bitcoin futures ETF who intend to hold for the long-term would cause the open interest data to be skewed to the upside. As a result, looking at Bitcoin open interest in isolation as means to asses speculative leverage within the system may be misleading.

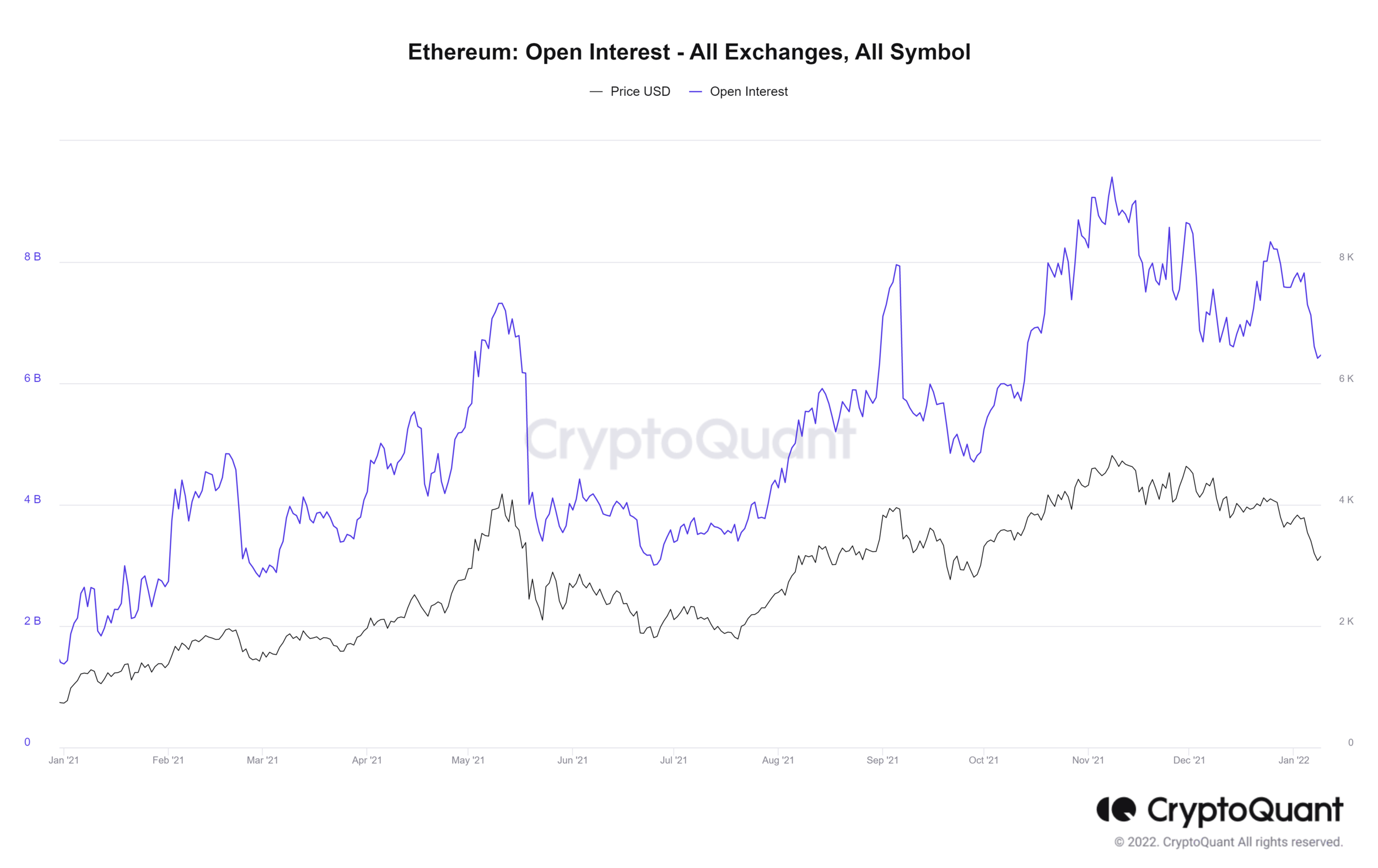

However, the fact that Ethereum open interest remains elevated to its own history (though has fallen along with price unlike Bitcoin) indicates there is still a large amount of leverage within the market for crypto as a whole.

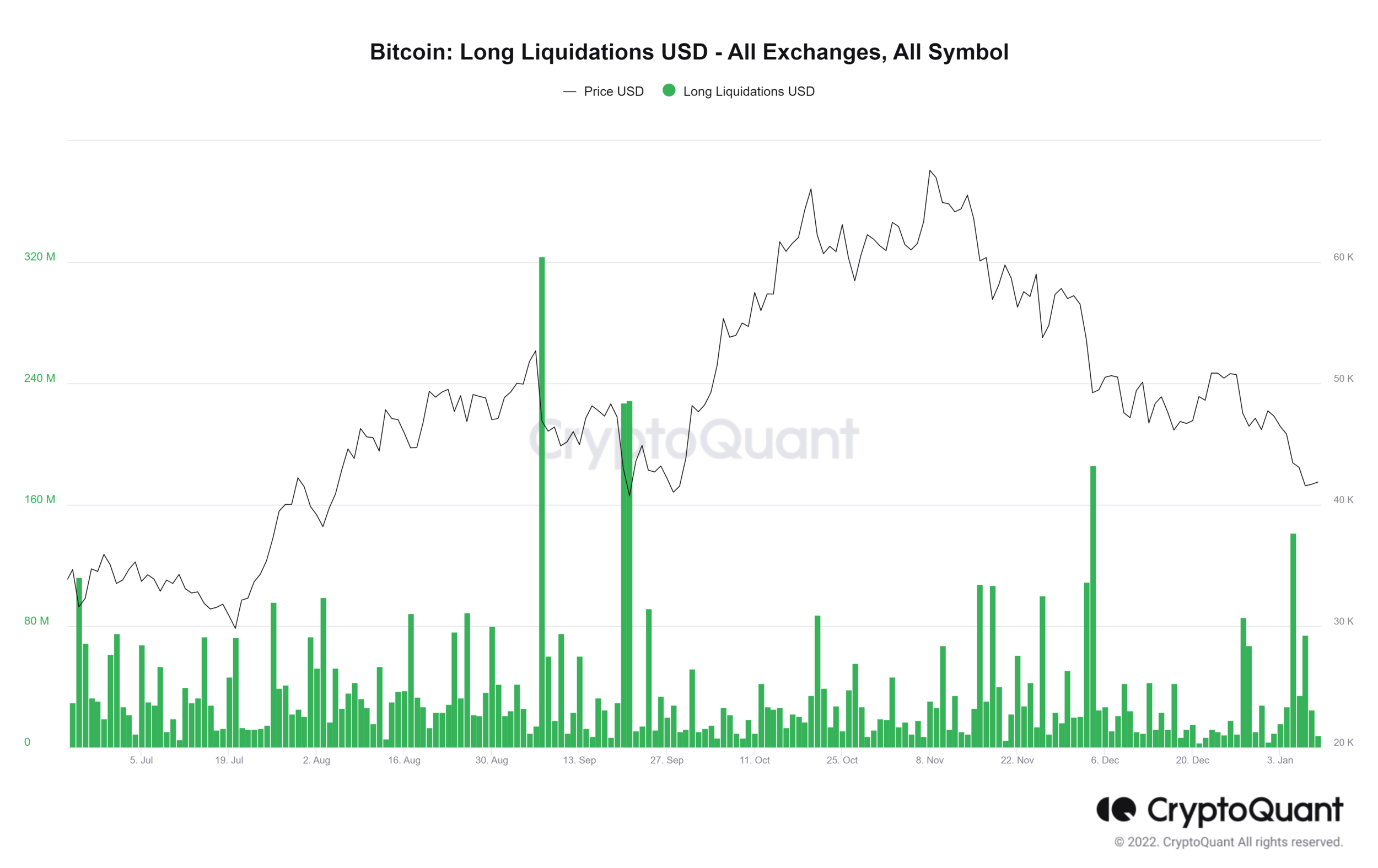

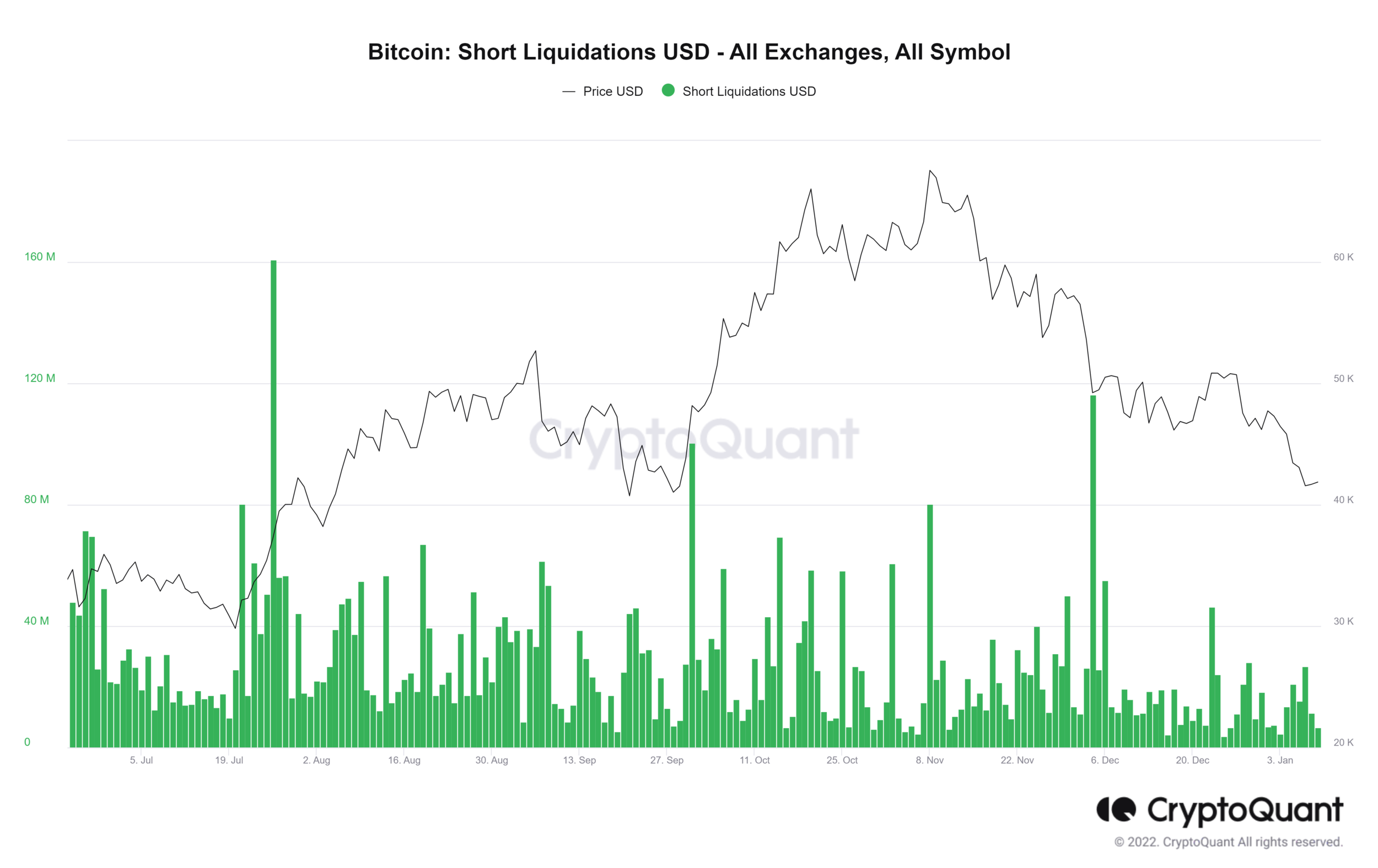

This divergence in open interest for BTC could be indicative of a couple of things. Firstly, it may mean there is still further leverage to be washed out before we find a sustainable bottom, or, it could be suggestive of traders betting heavily against BTC on the short-side, thus selling futures. To get a better idea of whether this is indeed the case, we can examine long-liquidations relative to short-liquidations for BTC. Long-liquidations in the past couple of weeks have been significantly greater than short-liquidations in terms of notional value.

This dynamic creates the possibility that we could be setting up for some form of short-squeeze to the upside in the near term. We saw a similar dynamic play out during the July/August bottom.

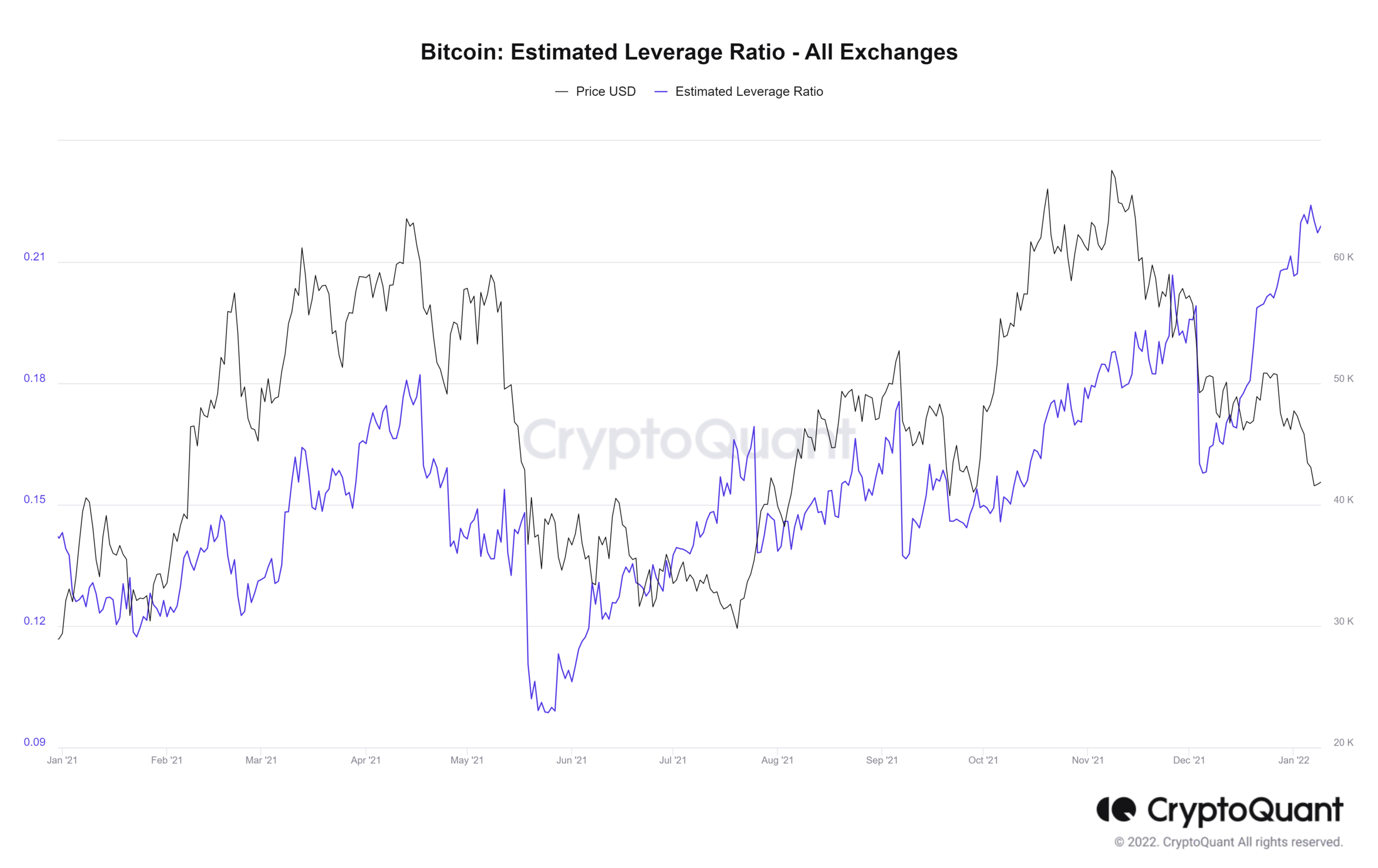

The leverage ratio for both Bitcoin could well be confirming the notion that investors are indeed betting heavily on the short-side, again indicating the potential for a short-squeeze in the near term.

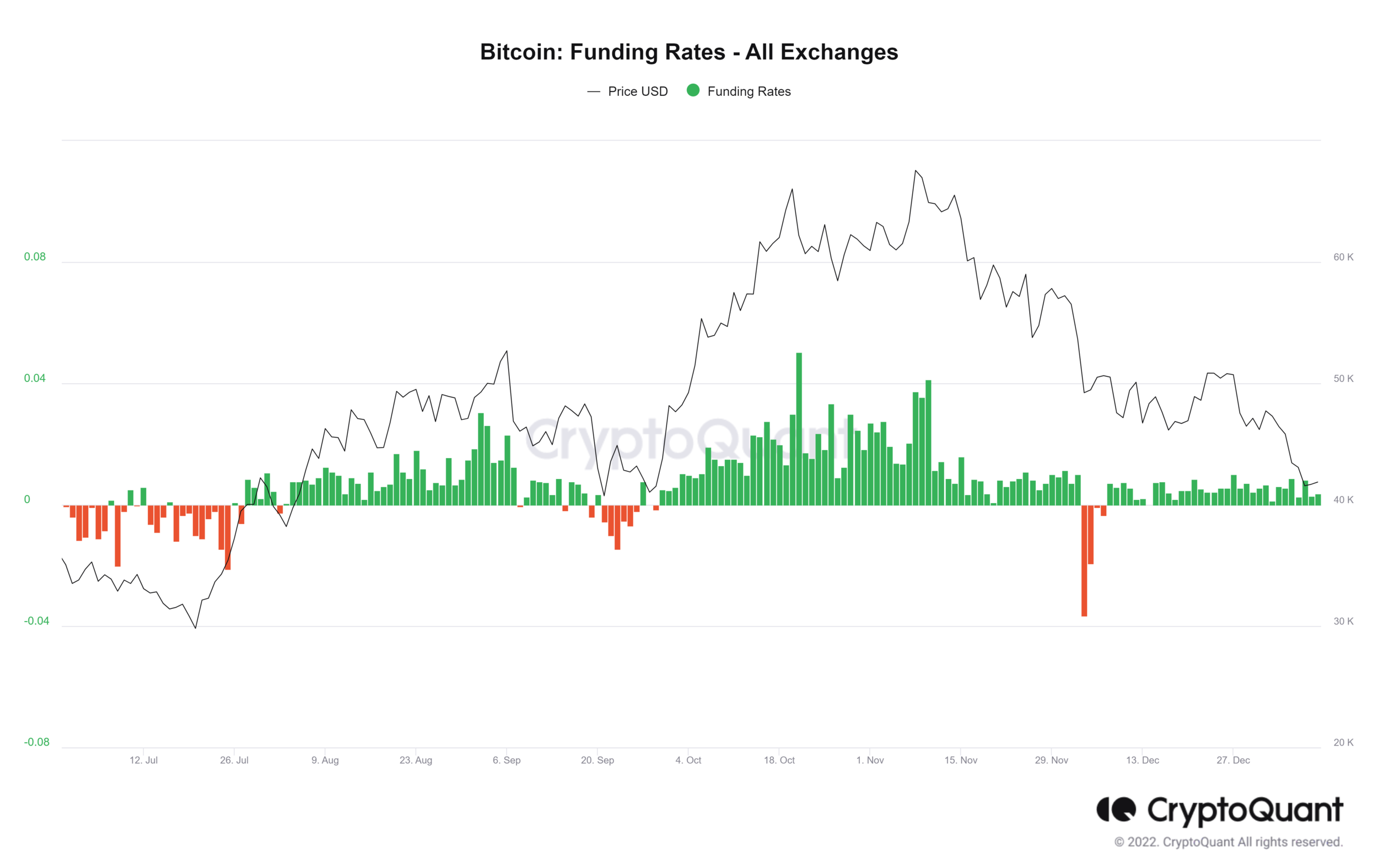

However, it is important to note that funding rates for both BTC and ETH are not necessarily confirming this theory as they remain positive (though marginally) for the time being. Negative funding rates indicate traders are paying extra to be short the market.

Before I move on to the on-chain metrics I monitor, one final thing I would like to point out in regards to the derivatives space is how we have just entered negative Gamma territory (…what’s Gamma?), and how dealers are short a decent amount of Gamma below the $42k area.

Source: Laevitas

Source: Laevitas

The options market for crypto does not have the same impacts on price movements as it does in equity markets via Gamma, Vanna and Charm flows but it likely does have some influence and is worth paying attention to. Undoubtedly, its impact is one that is only going to grow and become increasingly important going forward as more and more institutions enter the space, particularly so when we see things like the rise of short-volatility and yield enhancing mechanisms in De-FI Options Vaults (DOVs). Indeed, we did see the impact of dealer hedging influencing prices throughout the latter part of December as we approached the massive open interest options expiry at the end of the month. Given the significant level of out of the money (OTM) call option open interest that expired in December, this left dealers largely short calls. As we didn’t see any catalyst cause the market to move higher, the effects of Charm caused dealers to slowly reduce their long BTC hedges, keeping a cap on the market into expiry.

For now, what can be gleaned from the negative Gamma situation we find ourselves in at present is that volatility is likely to remain high in the short-term, whether to the upside or the downside.

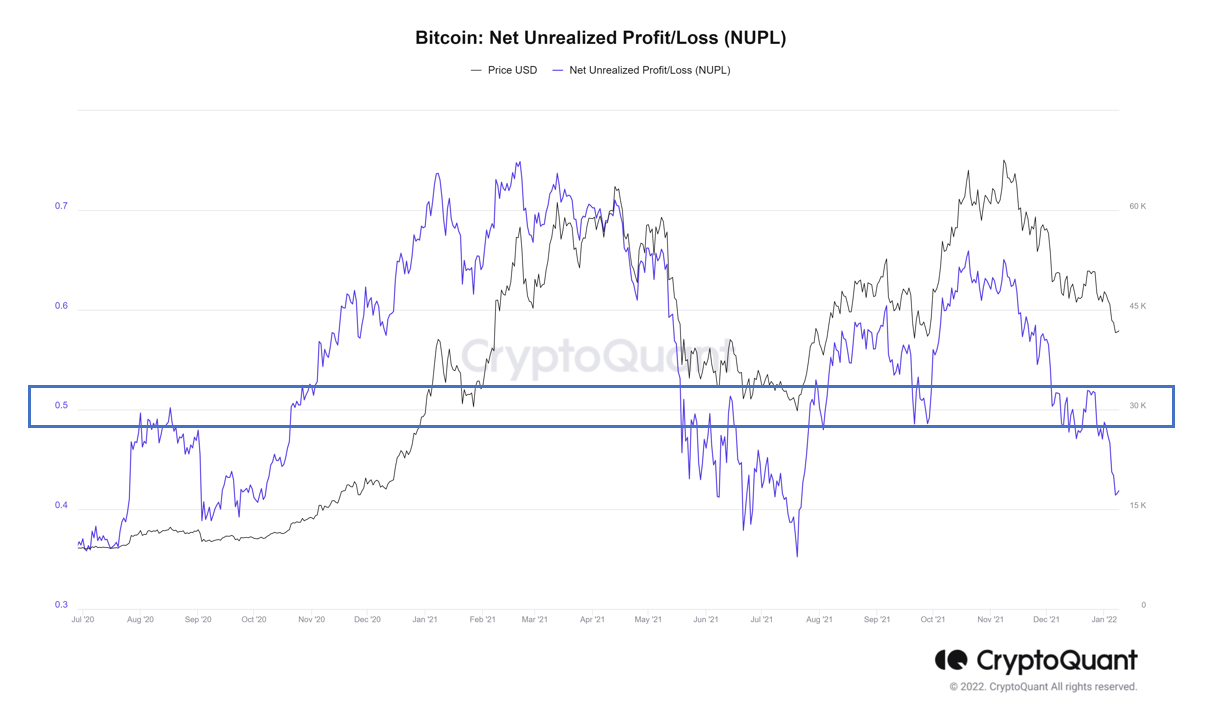

From an on-chain perspective there is a couple of things worth pointing out. Firstly, the 0.5 net unrealised profit/loss area has been breached. As noted by Glassnode in recent weeks, this 50% unrealised profits area has acted as key support and resistance over the past 18 months, and seems to be an area that defines whether we are in a bull or bear market. We have now clearly broken below this key level which indicates we may need further consolidation or negative price action to materialise before the bottom is in.

Likewise, the Short-Term Holder Market Value to Realised Value (MVRV) is sending a very similar message. This ratio measures Bitcoin’s market capitalisation relative to its realised capitalisation for short-term holders and can be thought of as a measure of their profitability. This metric has recently crossed below one, and when this has occurred in the past we have seen a period of sideways price action at the very least for some months. Again, this metric appears to be telling us a sustainable bottom may not yet be in place.

Source: Glassnode

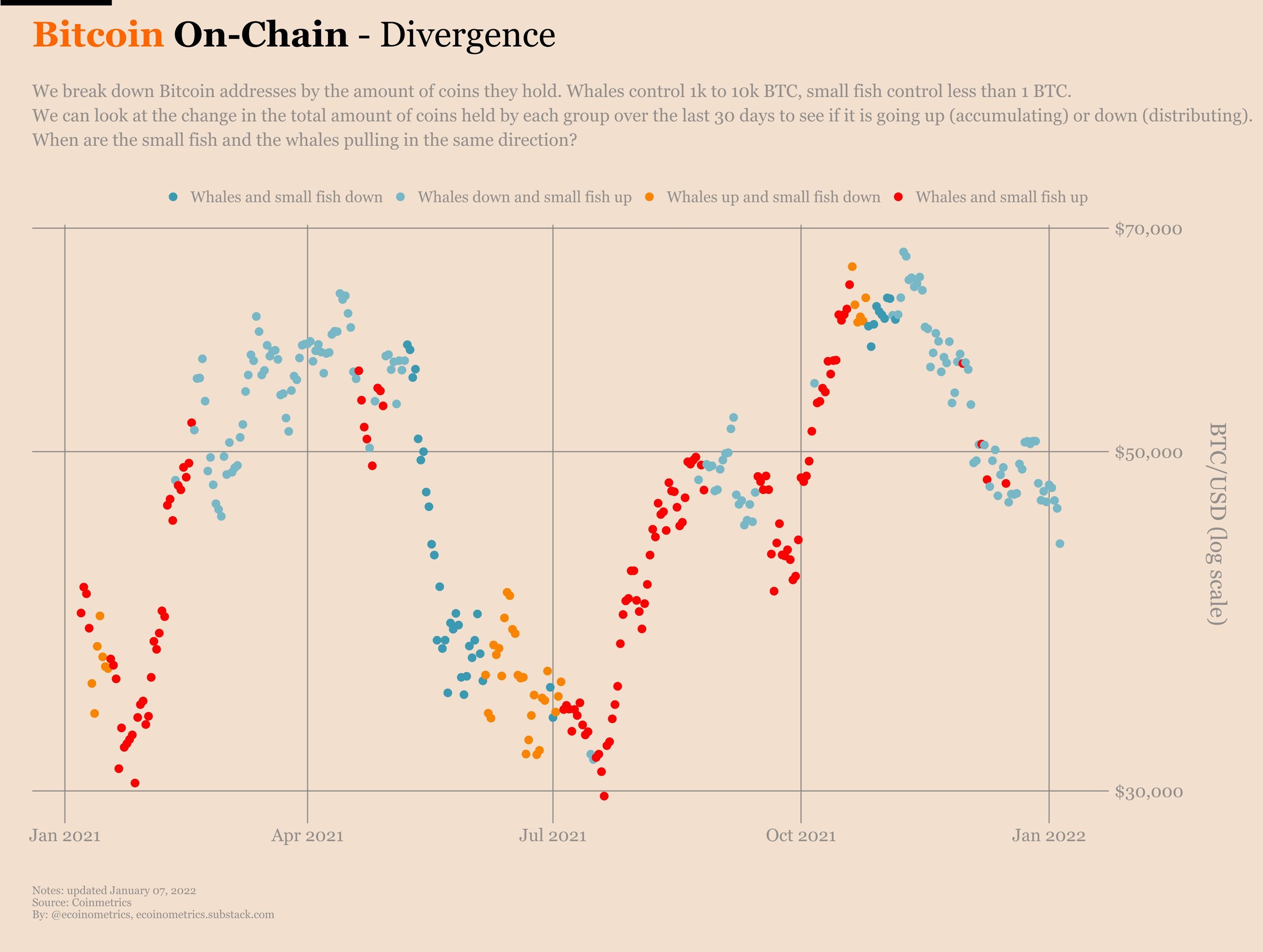

If we look at the buying activity of Whales (those who control more than 1 BTC and who can be thought of as the smart-money given their historical buying trends) relative to the Small Fish (those who control less than 1 BTC), we are again yet to see significant buying activity from the formed which would be indicative of a bottoming or up-trending market. Per Ecoinometrics, the blue dots on the below chart indicate Whales selling and the red/orange dots buying.

Source: Ecoinometrics

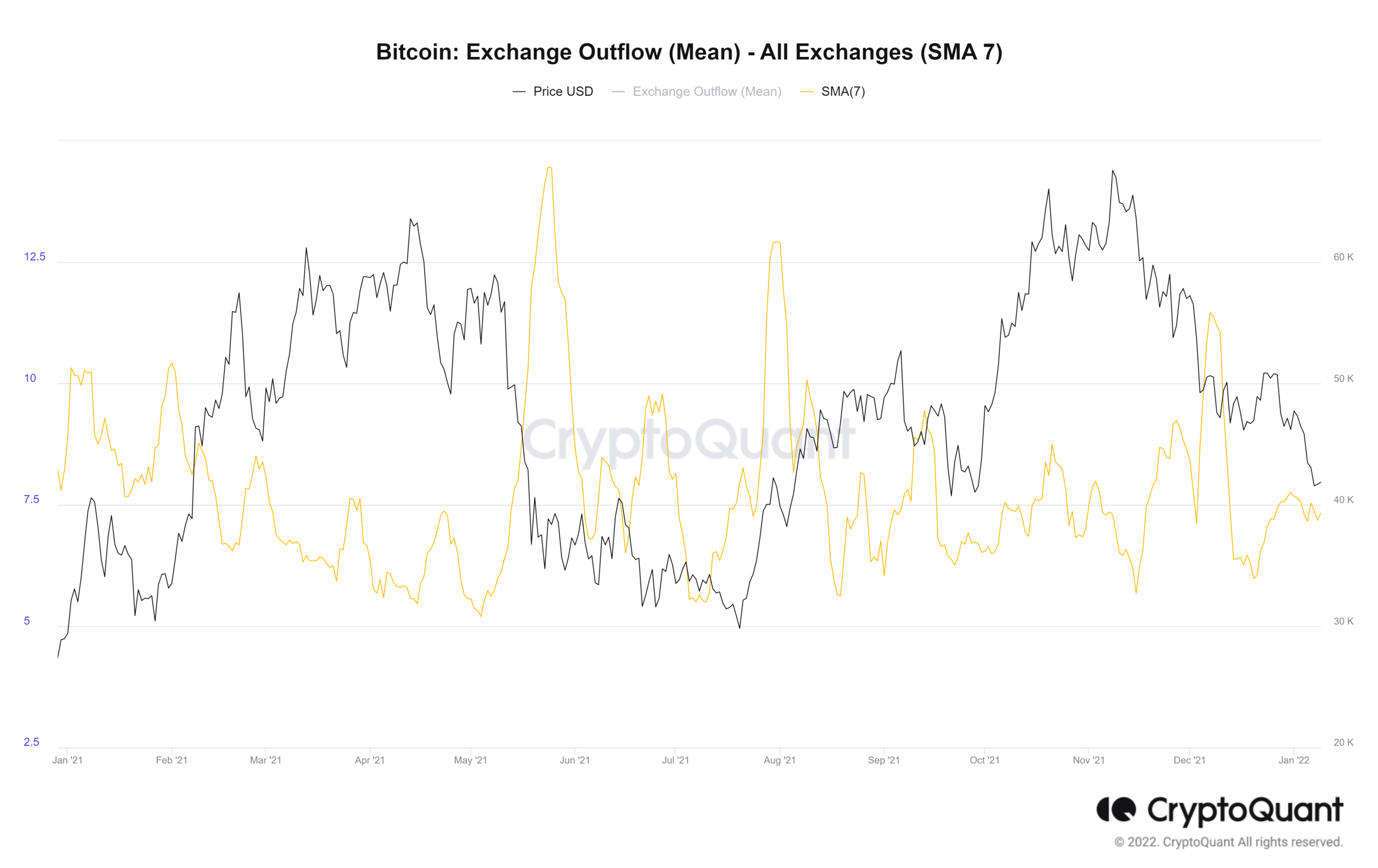

Likewise, if we look at exchange outflows, which measure the amount of Bitcoin removed from exchanges per transaction, we are not seeing a spike that would represent Whales accumulating and moving their coins off-exchange to be held for the long-term. High readings would be indicative of Whale buying (i.e. smart-money buying) as they would be moving a significant amount of their holdings off-exchange per transaction, a trend that would also signify decreased selling pressure.

Turning now to the macro outlook and in particular the growth cycle outlook, from a medium-term perspective I do believe crypto markets will find it very difficult come mid-to-late Q1 and beyond this year as we see a material pick-up in the deceleration of economic growth. I detailed this dynamic in depth within my recent Growth Cycle Outlook. Again, as I have pointed out previously, crypto markets do not perform well in macro regimes whereby growth and inflation decelerate in tandem. Unfortunately, slowing growth and inflation remains the highest probability outcome for much of 2022 at this point in time.

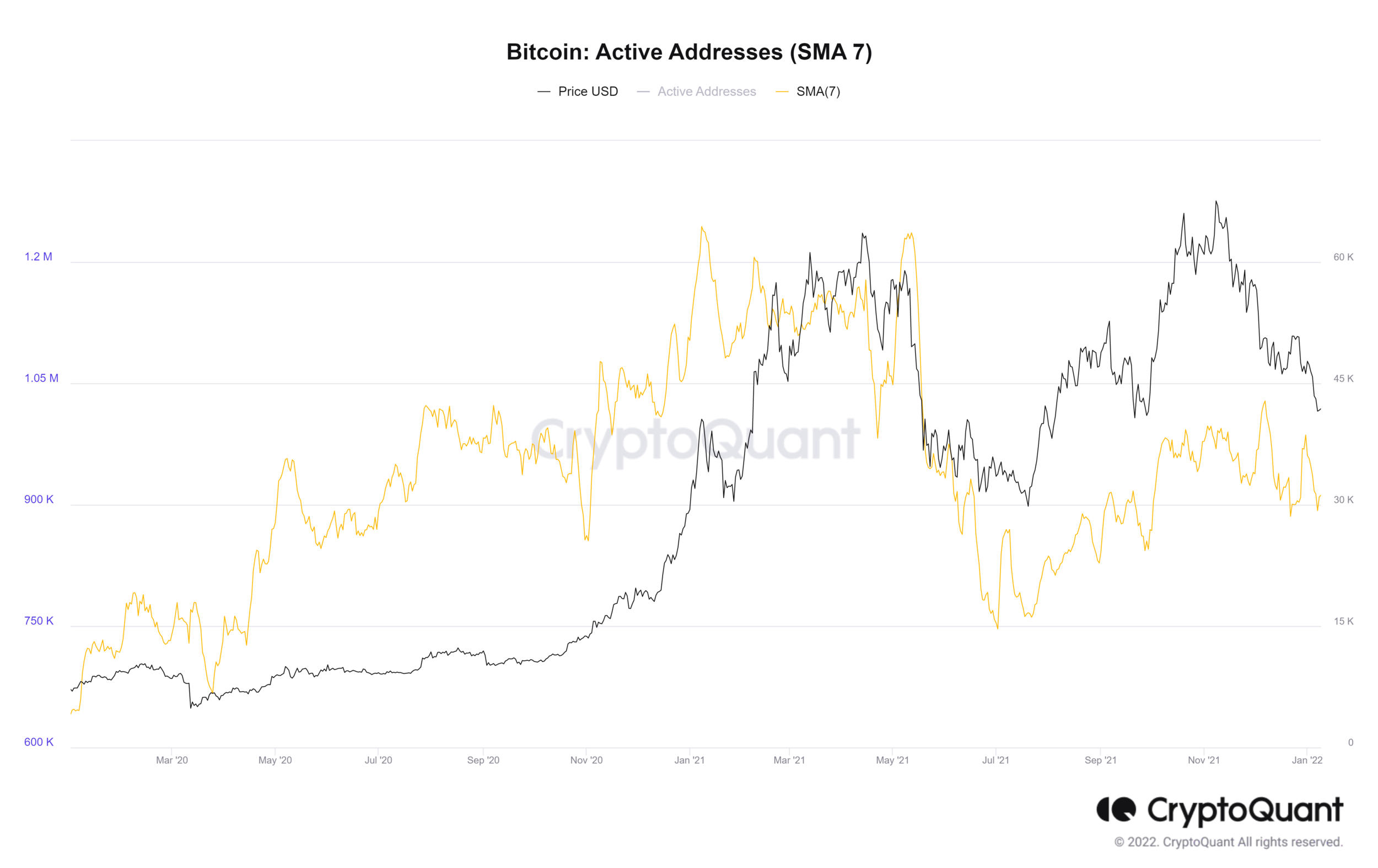

Indeed, we can see how much retail speculation has subsided in recent months as the business cycle began its slowing in Q2 2021 and how this has impacted crypto markets by looking at the number of active addresses. This metric peaked in early 2021 and has not recovered since.

Given so much of crypto’s price action has been governed by discretionary spending and consumption trends over the past couple of years, it is unsurprising to see that as real income growth has fallen and demand subsided, we have seen a lull in crypto markets via a significant drop in retail participation.

For the next month or two moving forward, we are seeing equity markets again attempt to price in one last bounce in growth before liquidity conditions truly deteriorate. As such, a mini-reflation trade over this time frame would likely bode well for crypto assets, particularly if we see rates continue to rise and a blow-off top in equity markets eventuate.

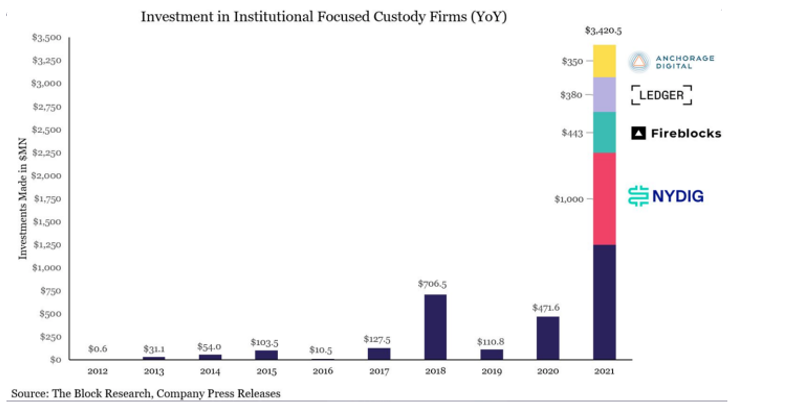

Couple this with the institutional money ready to flow into crypto markets, we may well see constructive price action for crypto in the months. Indeed, if we look at how much cash has been raised by institutional focused custody firms in 2021, approximately $3.5b, we get an idea of how much cash on the sidelines from an institutional perspective there actually is.

Source: The Block Research

In summary, we currently reside at important technical support levels for both Bitcoin and Ethereum that should be bought so long as investors employ proper risk management. Likewise, sentiment has by and large been washed out to a level indicative of buying opportunities in the past (though this could well go lower). Couple these factors with a potential short-squeeze and risk-on rally in equity markets, there are signs we could see constructive price action for crypto in the immediate term.

Once again, what remains a certainty is that risk management has never been as important in crypto markets as it is today.