A Dark Cloud Is Looming Over Markets

Summary & Key Takeaways

As banks increasingly tighten lending standards, credit conditions among households and corporations are slowly deteriorating as the credit cycle downturn progresses.

While households are on solid footing from a structural perspective, their increasing reliance on consumer and credit card debt in recent years should ultimately see a standard credit cycle downturn play out, though this is unlikely to be a full-blown credit crunch.

As corporations refinance their low-interest rate loans into higher yielding debt through 2024 and 2025, the higher interest rate environment and deteriorating credit environment will begin to be felt by corporations to a far greater extent than we have seen thus far.

Thus, as the credit cycle plays out, we should see credit spreads rise at some point, which will have negative implications for equities, volatility, employment and corporate earnings.

A storm is brewing

The slow but steady deterioration of the credit cycle remains one of the largest headwinds both investors and the economy face over the next 12 to 18 months. To be sure, as a result of a resilient economy, well capitalised consumer and corporate balance sheets along with little duration risk (yet), both households and the corporate world have been able to hold up relatively well in the face of multi-decade high interest rates. But, as the credit cycle continues to play out (albeit slower than expected), cracks are slowly beginning to form.

Central to credit creation and thus the credit cycle itself are lending standards, and as we can see below, the percentage of banks tightening lending standards across the board look to have reached cyclical highs.

Unsurprisingly, tighter credit conditions are slowly seeping through the economy. Per the NFIB Small Business Survey credit conditions for small businesses are at or near their worst in a decade, while interest costs are nearing decade highs. Credit requirements are also on the rise (though from secularly low levels).

Meanwhile, household credit conditions too appear to be tightening. Per the New York Fed’s household survey, the percentage of respondents who are finding it more difficult to obtain financing relative to a year ago is at its highest point in over a decade. The probability of households not being able to service interest payments over the next three months also continues to rise steadily, though still at moderate levels.

The slow but steady deterioration of household credit conditions should hardly be surprising given the backdrop of the rise in credit card interest rates we have seen over the past 18 months.

Such dynamics are following a period where we have seen significant growth in consumer credit, primarily in the form of credit card debt as nominal wage growth lagged inflation for much of 2021 and 2022.

Thus, delinquency rates for credit card debt is on the rise, particularly of those offered by smaller regional banks.

Meanwhile, consumers are also feeling the pinch in relation to car repayments. A noted recently by Bloomberg, “Americans are falling behind on their auto loans at the highest rate in nearly three decades. The percent of subprime auto borrowers at least 60 days past due on their loans rose to 6.11% in September, the highest in data going back to 1994.”

Source: Bloomberg

Of course, the sector of the economy most susceptible to higher interest rates and deteriorating credit condition is commercial real estate. Delinquency rates for nearly all types of commercial property are on the rise, with offices being hit particularly hard via the combination of both higher rates and the shift to work-from-home. The fact the majority of commercial real estate loans are issued by regional banks only makes matters worse. The balance sheets and lending capacity of such banks have been hit much harder versus their larger peers during this hiking cycle, a dynamic which culminated in the Silicon Valley Bank crisis earlier this year, forcing the Fed to backstop bank balance sheets via its Term Funding Facility (whose usage just made a new high this month).

So then, we are we in the credit cycle?

As we have seen, credit conditions are clearly worsening across the board, but at this stage remain far from recessionary levels.

Perhaps the best leading indicator of where the credit cycle is heading is the yield curve. An inverted yield curve tends to squeeze bank interest margins, reducing incentives to lend and thus resulting in lending standards tightening.

Tighter lending standards in turn leads to falling loan growth. This is true of both commercial and industrial loans…

As well and consumer loans.

So, as credit becomes increasingly scarce, delinquency rates rise, particularly as this generally occurs when economic conditions worsen and the need for credit rises. The exception to this was the COVID-19 induced recession, though this was likely attributable to the unprecedented monetary and fiscal response that muted almost all negative impacts associated with a deteriorating credit cycle (much of which is still being felt today).

Alas, we should expect to see some kind of spike in delinquency rates, as well as default rates in the coming quarters.

And of course, perhaps most importantly for investors, the negative implications of such dynamics should ultimately show up in the form of rising credit spreads. After all, credit spreads are the direct link between the credit cycle and financial markets, namely equities and volatility. Per Bloomberg’s Simon White, “Corporate balance sheets explain the link between credit and volatility. As credit expands, loan growth rises, funding business investment and consumer spending. But when the loans come due, they often need to be refinanced. This stresses both sides of corporate balance sheets. As equity is just a thin wafer of capital on the balance sheet, it must bear the adjustment, meaning that equity volatility rises. The lead time in the relationship is explained by the average maturity of loans.”

One of the primary reasons why worsening credit conditions and higher yields have yet to fully filter through to the real and financial economies is due to the significant level of low-duration financing that took place by corporations during COVID years of record low interest rates (i.e. 2020-2022). As such, corporate debt burdens for the most part continue to be easily serviced by cash flow.

However, as these low interest rate debts mature and businesses slowly begin to refinance these loans with the much higher interest rates of today, we should expect to see the negative implications of the credit cycle come for the fore. As we can see below, roughly one fifth on US corporate debt is set to mature over the coming 36 months, at a time where yields are at decade highs.

As such, we should expect to see a spike in credit spreads at some point over the next six to 12 months. My credit spreads model (which uses such inputs as the ISM Manufacturing PMI, bank tightening standards, as well as various consumer and small business surveys) suggests spreads should be significantly higher than current levels. Whilst this is probably true to a certain extent, this model is undoubtably being skewed to the upside as a result of survey data being heavily influenced by inflation rather than underlying fundamentals.

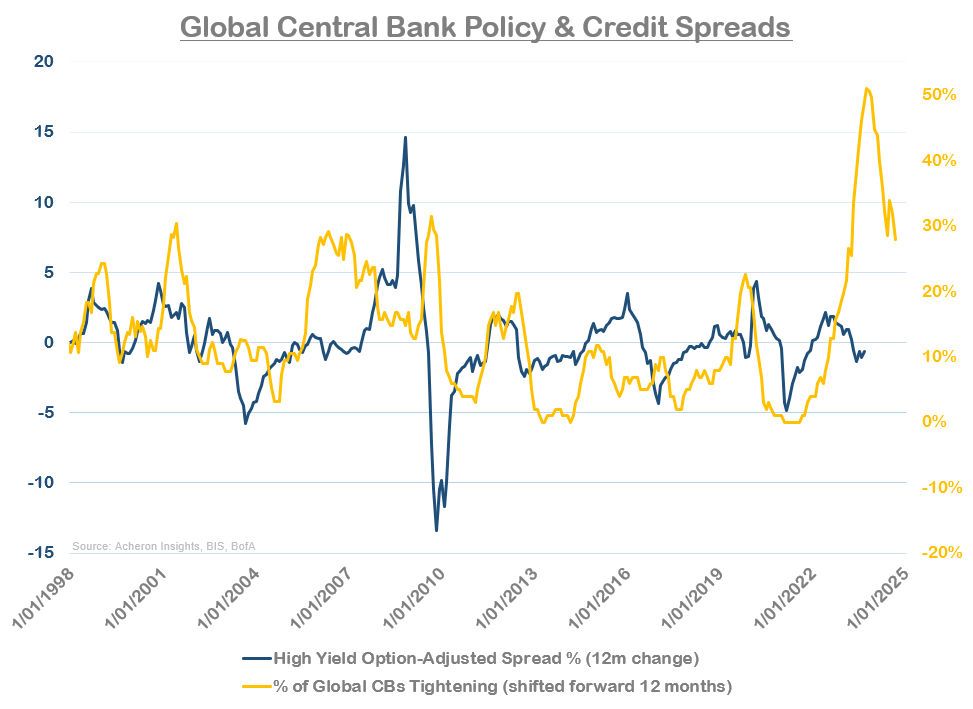

Regardless, it is clear spreads will spike at some point, with interest rates also suggesting this to be the case.

As well as global monetary policy conditions.

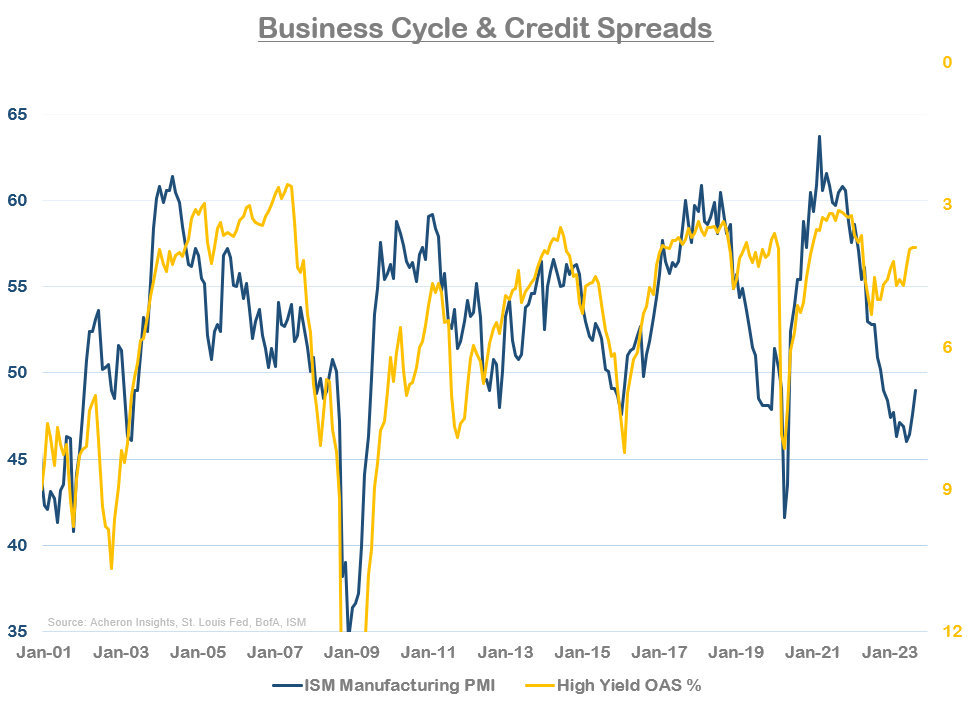

While it is also fair to say markets are pricing high yield spreads to perfection relative to the business cycle.

Consequences of a credit cycle downturn

Deteriorating credit conditions and rising credit spreads have significant implications for investors. The link between credit spreads with equities and equity volatility is perhaps most important. As we can see below, rising credit spreads generally correlate to lower equity market returns over time.

And unsurprisingly, higher credit spreads thus equate to higher volatility.

One way this manifests is through corporate earnings. The continued compression of credit spreads we have seen over the past year has been very supportive of corporate profits, and is likely to continue to be the case until spreads do eventually widen.

Of course, the worst hit sector during such times is generally banks. Tighter lending standards usually results in the underperformance of the banking sector relative to the broad market, with about a 12-month lag.

Other sectors that are particularly vulnerable to the credit cycle are industrials and real estate, which are both cyclical and capital intensive.

And finally, tightening credit conditions almost always lead to rising unemployment. Unemployment is generally the last shoe to drop in both the business cycle and credit cycle, as laying off workers is usually the last resort for employers during bad times.

Fear not, this won’t be a GFC-style credit crunch

While the downturn of the credit cycle is obviously an unfavourable period for the economy, we shouldn’t expect this slowdown to be anything out of the ordinary. Don’t expect any kind of GFC-type credit crunch.

As it stands, both households and corporations continue to be in as good a position to deal with higher interest costs and tighter credit conditions as they have been at any other point in recent decades.

Indeed, as we can see below, debt serviceability for mortgages remains at secular lows, ditto household debt overall. And while we have seen a significant spike in consumer debt service payments/total consumer debt as a percentage of disposable income (as I have detailed above, and whose rise will put the most stress on households during this credit cycle downturn), we are still only near average levels.

Meanwhile, household net worth and checkable deposits remain well above their respective long-term trends, particularly the latter. Thanks to an epic bull market over the past few years, households remain on solid footing to such an extent that they should be able to ensure any credit cycle downturn does not evolve into a full-blown credit crisis.

. . .

Thanks for reading!

If you would like to support my work and continue to allow me to do what I love, feel free to buy me a coffee, which you can do here. It would be truly appreciated.

Regardless, feel free to share this with friends and around your network. Any and all exposure goes a long way and is very much appreciated. Thanks again.