The Outlook For The Stock Market Is Bullish

Summary & Key Takeaways:

Though above target, inflation has cooled sufficiently to support front-loading of rate cuts by the Fed.

Business cycle lead indicators remain neutral to favourable, so given recent growth weakness, we should expect growth to begin to surprise to the upside.

Any upside surprises in growth coupled with rate cuts and increasing liquidity are a very bullish backdrop for risk assets and support a continued rally into 2025.

However, a number of short-term headwinds remains, suggesting we could see further volatility over the next month or two before a post-election rally takes the market to new all-time highs.

Inflation remains supportive of rate cuts, for now

From the Fed’s perspective, the current battle against inflation is over. The Fed has decided it favours supporting financial and monetary conditions over its inflation target mandate. Unless you expect economic growth to significantly deteriorate from here, this is unequivocally bullish for risk assets.

While it is true inflation has not returned to the Fed’s 2% target, it is also true inflation pressures have eased materially over the past 18 months to a level that would allow the Fed to cut rates and ease monetary policy should they wish to do so. This “window” of moderating but above target inflation is open and is likely to remain open for at least another couple of quarters.

This is what inflation lead indicators are signalling. We are likely close to a trough in headline inflation but shouldn’t expect a material pick-up until 2025.

But there is evidence of a less favourable inflation outlook on the horizon. We are seeing signs of life from a goods and food inflation point of view. In addition, we may be nearing a trough in Owners’ Equivalent Rent CPI (the biggest component of the CPI basket).

Another lead indicator that has turned higher is my regional Fed prices survey.

Financial conditions also continue to suggest the year-over-year inflation rate should be at least equal to what it was 12 months ago. For reference, headline CPI was 3.7% at this stage last year and is currently 2.6%.

Thus, there are clearly upside inflation pressures at play that are likely to see CPI move upwards at some point in the near future, so this easing “window” for the Fed may be fleeting.

But, as it currently stands, inflation is at reasonable enough levels for the Fed to ease in the short-term and provide scope to front-load as many of the rate cuts priced into markets as possible. The bearish implications stemming from any potential pick-up in inflation remains a story for 2025, not September of 2024.

The jobs market also supports easy monetary policy

From a monetary policy perspective, labour market data has been trending in the right direction even more than inflation of late.

The Atlanta Fed Wage Growth Tracker currently sits at 4.6%, down from its peak of 6.7% two years ago. Wage growth remains above its pre-COVID trend, but the Fed will be very happy with these developments, particularly as it relates to services inflation. My wage growth lead indicators also continue to suggest this downtrend is likely to continue into year end.

Expect policy makers to ease while they can

Inflation and growth surprises are both firmly supportive of easy monetary policy at present. This is not just true for the US, but for most of the developed world.

Historically, when the Fed cuts rates at a time where the S&P 500 is within 2% of an all-time-high, the stock market have been positive 75% of the time over the next six months.

Source: Ryan Detrick

Another risk markets are laser-focused on at present which also looks to be taking a back seat for now is the Bank of Japan’s hiking cycle and the unwinding of the yen carry trade that have been negatively impacted by this dynamic. While I expect this to be a theme that continues over the long-term, risks of the BOJ tightening monetary policy and tapering liquidity measures appears unlikely over the medium-term. Again, this is supportive of risk assets on the margin.

Expect economic growth to surprise to the upside

On the growth front, regular readers will know my analysis has led me to believe we should continue to expect economic resilience from the US economy. Even with the recent spout of economic weakness (primarily from the labour market), this view has not changed.

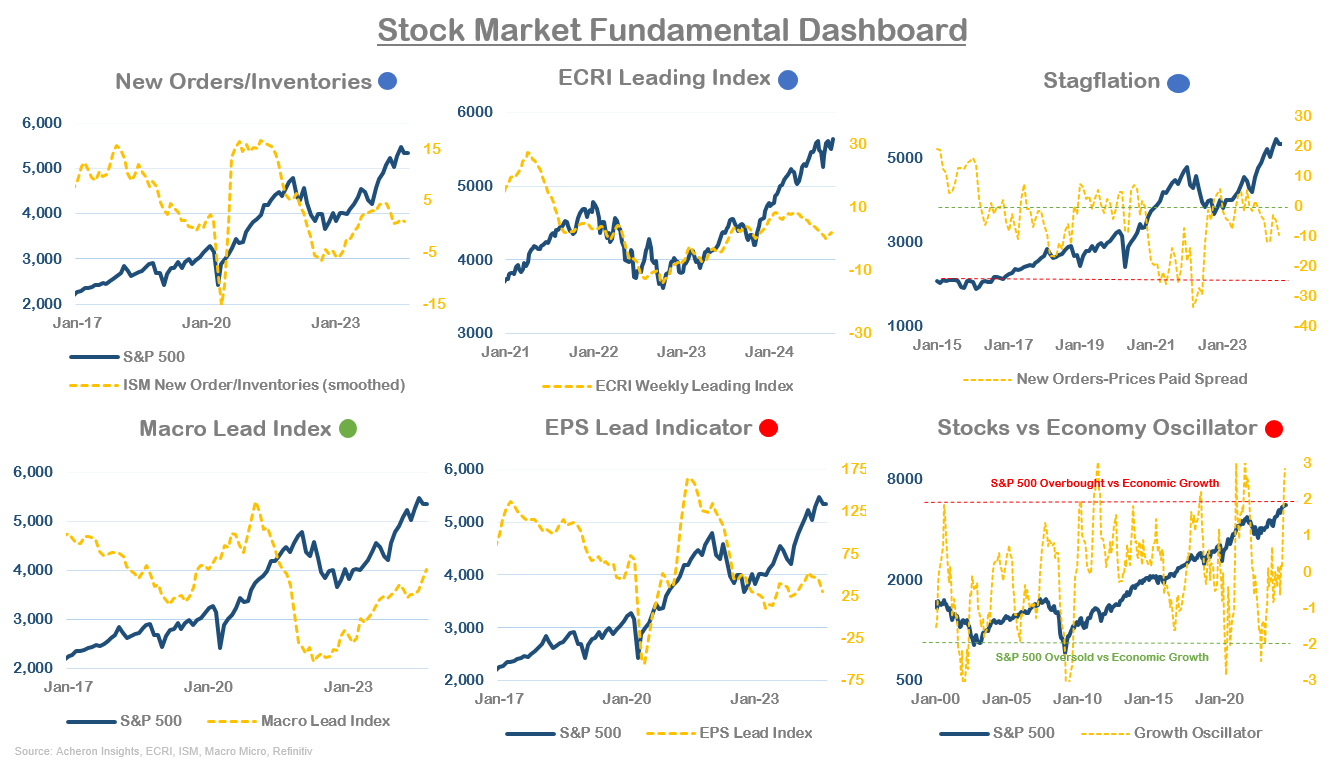

Now, even though stocks remain overbought versus underlying economic fundamentals, we should expect growth to begin to surprise to the upside. As we can see below, many of the US business cycle lead indicators I monitor are relatively robust. Though not outstanding, none appear to be signalling imminent recession. Even the ISM New Orders/Inventories spread has improved when measured on a smoothed three-month average.

The global easing cycle is also a supportive factor for the global business cycle on net. And as I have discussed, this is likely to continue trending higher in the short-term.

Likewise, the massive easing of financial conditions in the form of a weaker dollar, lower yields and weaker commodity prices has caused my Macro Conditions Lead Index to turn materially higher of late. When commodities, rates and the dollar are moving lower in unison, it is generally a very supportive outcome for both the economy and stock market.

One mechanism through which lower interest rates positively impacts the economy is through the housing market, which itself is one of the primary drivers of the business cycle. As we can see below, lower mortgage rates (inverted) inevitably leads to a pick-up in housing related activity, such as building permits. This should translate into an increase in residential investment over the medium-term.

Of course, from a global business cycle perspective, the elephant in the room remains the deflationary impulse coming out of China. Until we see a sufficient level of monetary and fiscal support for the Chinese economy, China will be mired in their balance sheet recession and constrain global growth as a result.

The medium-term outlook for the stock market remains positive

On the whole, these dynamics portend a relatively reasonable outlook for the stock market over the medium-term.

Stock market fundamentals have improved over the last month, and appear unlikely to fall off a cliff in the short-term.

While liquidity and financial conditions also remain relatively favourable for the stock market over the medium-term.

On the sentiment and positioning front, some of the shorter-term measure such as the AAII Bull/Bears spread are looking very extended, as are medium-term measures such as asset manager positioning, margin debt and the corporate insider sell/bull ratio. As a result, we might need to see further unwinding in long positions over the next month or two before the market can move higher.

But on the other hand, overall speculative positioning is still net-short the market and only at the 30% percentile of readings over the past decade.

Volatility targeting funds have also significantly de-levered as a result of August and September’s volatility, while hedge funds are currently heavily net-short the stock market.

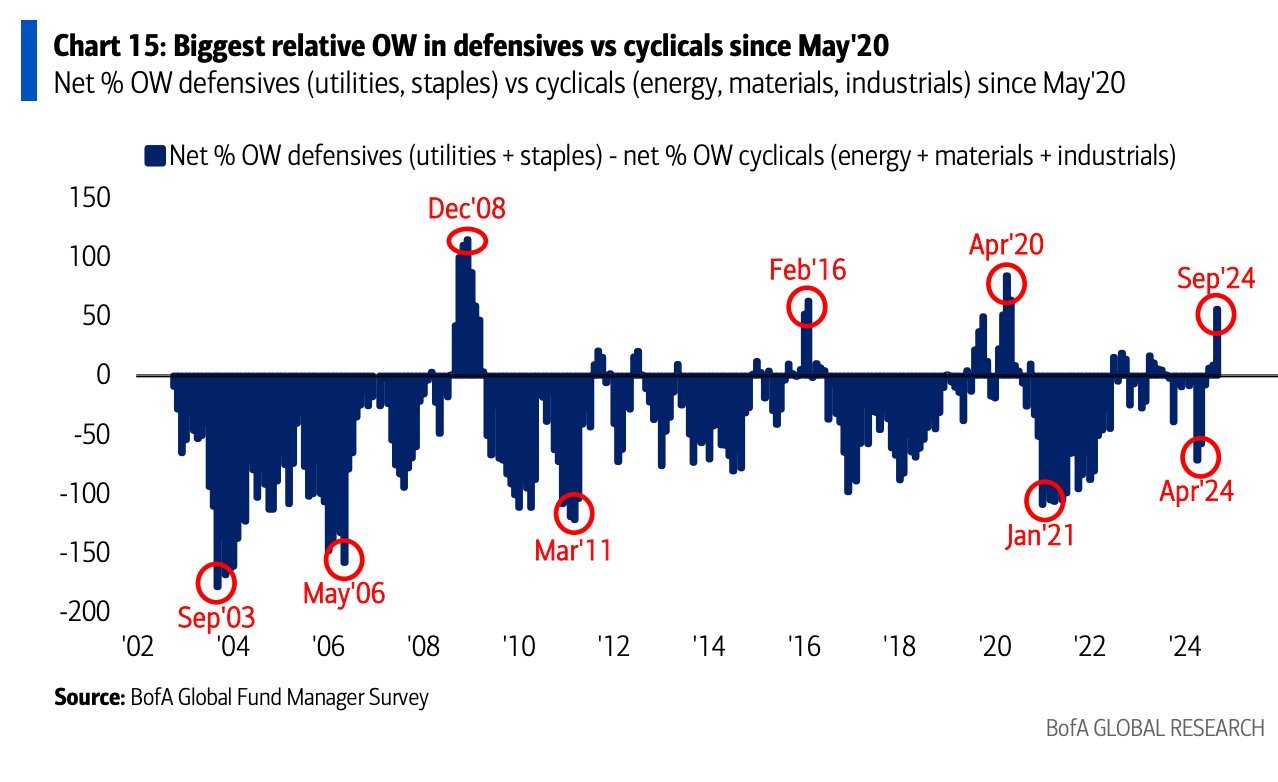

Active manager positioning has also shifted much more defensive over the past month. According Bank of America’s Global Fund Manager Survey, managers are the most overweight defensives (i.e. utilities and consumer staples) relative to cyclical sectors (i.e. energy, materials and industrials) since May 2020, with similar extremes in the past marking market bottoms, not tops.

In all, positioning does not appear to be a material heading for the market over the medium-term, though perhaps a short-term unwinding is required.

A few short-term factors to consider

While the outlook for the stock market appears relatively positive over the medium-term, we must keep in mind the long and medium-term are made up of short-term events. As such, I will finish this missive with a few short-term indicator’s investors should consider.

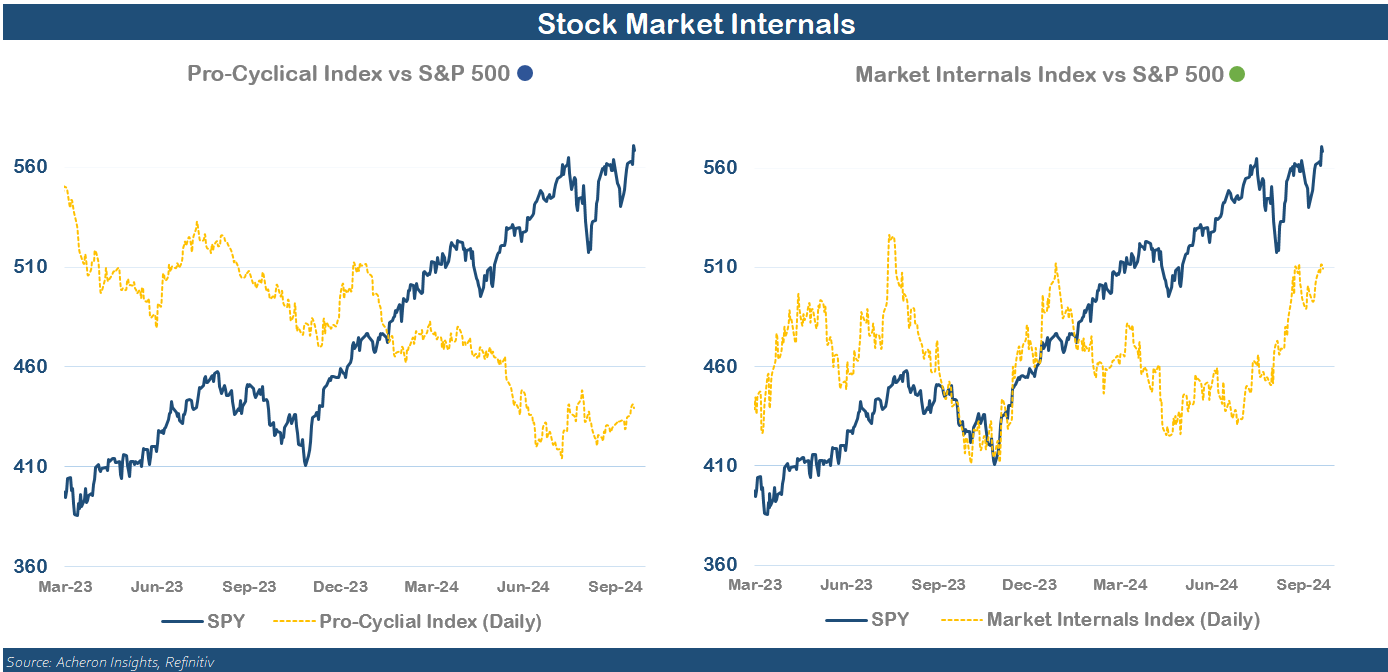

Firstly, market internals have improved dramatically over the past month, with both my Pro-Cyclical Index and Market Internals Index having trended higher through September.

But despite this improvement, other internals indicators such as short-term breadth have diverged lower this past week, suggest we may be in for some more chop.

Market seasonality is also suggesting further volatility may be on the cards in the short-term.

Supportive hedging flows from market makers are also likely to be much less prominent over the next two weeks, as is the corporate buy-back bid. What’s more, November’s election stands as a prominent upcoming event that is likely to keep volatility elevated in the short-term as traders hedge against any kind of event-risk, meaning there is plenty of room for the market to continue trending sideways until after the election. Unless the data were to change from now until then (which is entirely possible), my best guess is we see a strong post-election rally into year end and to kick off 2025.

. . .

Thanks for reading!

If you would like to support my work and continue to allow me to do what I love, feel free to buy me a coffee, which you can do here. It would be truly appreciated.

Regardless, feel free to share this with friends and around your network. Any and all exposure goes a long way and is very much appreciated. Thanks again.