We Are Close To A Bottom In Oil Prices

Summary & Key Takeaways:

Speculative positioning in oil has fallen back to levels generally associated with bottoms in the oil price.

Oil market fundamentals weakened notably throughout April and May, giving speculators a reason to sell. However, the outlook appears much more favourable over the medium-term as we enter the northern hemispheres driving season.

2024 is likely to be a rangebound year for oil prices. It appears we are now close to the bottom of that range.

Given we are in an election year, prices are likely going to be capped around the $90-$95 level, with triple digit oil not likely to be a realistic scenario until 2025. Longer-term energy bulls should continue to use view such pull-backs as buying opportunities.

A buying opportunity for energy bulls

Over the past month, oil has gone from a clear sell to what is now approaching an attractive buying opportunity for energy bulls. In my most recent oil write up, I made it fairly clear the obvious short-term path for oil and energy prices was to the downside. And, over the past month, WTI has pulled back around $10 from its peak in the type of moved that more or less aligned with my analysis.

The primary reason for my bearishness was how extended speculative positioning had spiked to the upside. Similar upside spikes in hedge fund and CTA buying are rarely associated with continued price appreciation, and with crack spreads having been falling since March, there was plenty of scope for prices to fall as inventories built.

Fading speculators has undoubtedly been the best way to play the oil markets in recent times. And, as speculative positioning has been unwound significantly these past few weeks, we are once again approaching levels associated with bottoms in the oil price.

However, investors should keep in mind positioning tends to overshoot to both the upside and downside. Thus, there is likely more unwinding of CTA and hedge fund longs/an increase in shorts that needs to play out, which could continue to push prices lower over the short-term. This seems the case in relation to trend following CTAs, who are still modelled as sellers over the coming weeks according to Bank of America.

Despite the geopolitical noise that is ever present in the oil market, the underlying fundamentals clearly worsened throughout April and May and have been very much supportive of lower prices.

Crude and total petroleum inventories have seen persistent builds over the past couple of months in the US, while refined products such as gasoline and distillate inventories have been trending sideways.

Importantly, global inventories have seen persistent builds since February.

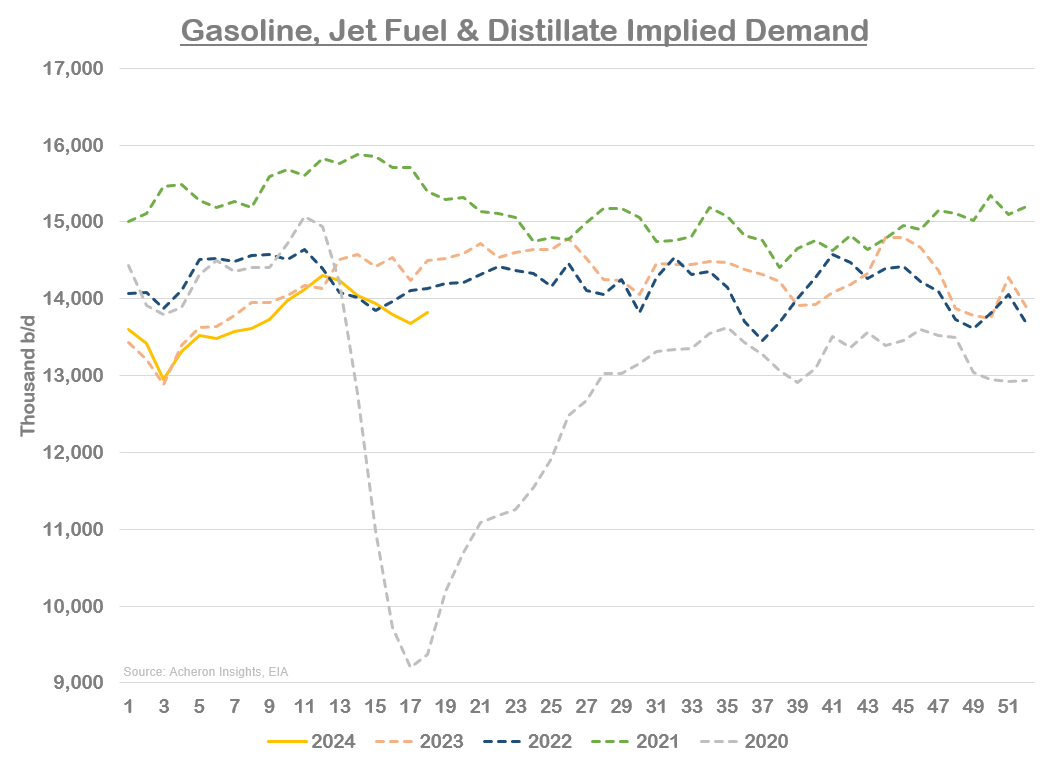

Refined product demand has also been below seasonal averages. While the EIA’s implied demand data should be taken with a grain of salt, demand has clearly been lacking over the past couple of months, which is fairly normal during this period of the year.

Weaker demand, along with refinery maintenance season and refinery outages in Europe have thus seen crude oil demand remain stagnant.

Fortunately, the outlook appears more favourable for both refinery product demand by consumers and crude oil demand by refineries. Morgan Stanley expects refinery runs to pick-up by 3.5m/d globally from April through August/September as we exit maintenance season and enter the northern hemisphere’s summer driving season, the period of the year associated with the strongest oil demand, as we can see below.

Unsurprisingly, the May through July period is generally the most favourable for oil prices.

In addition, we should start to see a pick-up in diesel demand as the global manufacturing cycle picks up. We can see below how close diesel consumption is linked to the business cycle.

The same relationship is true of oil prices themselves and the business cycle.

Regular readers will be aware of what the leading indicators of the business cycle are suggesting. My recent deep-dive into the outlook for the business cycle suggests economic growth should continue to move in the right direction through the remainder of 2024. The below dashboard highlights a number of these key lead indicators.

Importantly, lead indicators of the global business cycle are also pointing to supportive growth dynamics in 2024. As such, this trend should be supportive of global industrial activity over the medium-term, and thus supportive of oil demand.

The key to assessing when we do see a pick-up in demand and an improvement in the underlying fundamentals of the oil market are crack spreads. They have been the key driver of oil prices over the past 12 months. As such, should crack spreads begin to tick-up again, we should gain greater confidence this pull-back has run its course.

Whether this occurs at a bottom of $77-$78 for WTI that we are at currently, or lower around the $72-$75 area remains to be seen. Regardless, this zone represents a strong technical support level for WTI, and any dip below should be viewed as an attractive buying opportunity for energy bulls.

In summary, the fundamental picture for oil prices weakened throughout April and May, forcing speculators to de-risk and push prices lower. While there likely remains some downside from here over the coming few weeks, the fundamental outlook over the medium-term is constructive. But, as I have said in the past, 2024 is likely a year where oil prices are rangebound. Given we are in an election year, prices are likely going to be capped around the $90-$95 level, with triple digit oil not likely to be a realistic scenario until 2025.

. . .

Thanks for reading!

If you would like to support my work and continue to allow me to do what I love, feel free to buy me a coffee, which you can do here. It would be truly appreciated.

Regardless, feel free to share this with friends and around your network. Any and all exposure goes a long way and is very much appreciated. Thanks again.