The Stock Market Is The Economy

Summary & Key Takeaways

Due to decades of easy monetary policy, the economy is now tightly linked to the growth in asset prices. Namely the stock market and the housing market.

When the stock market and housing market falls, this has significant implications for employment, consumption, economic growth and government deficits.

It is through this precise channel the Fed is trying to quell inflation. They may get more than what they bargained for.

Welcome to a world of financialisation.

We Live In A Financialised Economy

Through decades of easy monetary policy and asset price appreciation at the expense of wages and growth, we have witnessed an undeniable shift in the nature of the economy to one where perhaps the greatest influence is through the movements in the financial economy. Specifically, I am referring to the growth in financial assets, primarily stock market and house prices.

The near four-decade long trend of rising corporate profits and stagnant wage growth has seen those who have been able to accumulate financial assets benefit at the expense of those who have not.

Wealth inequality has ensued. And with that, a financialisation of the economy has resulted.

This process of an increased reliance on financial asset appreciation as nearly the only means to generate wealth has left much of the developed world in a situation where the economy is now closely tied to the growth in financial assets. For those who believe the stock market is not the economy (a statement which has been true for much of history), in today’s world, the evidence now suggests otherwise. A period of economic stagnation and a reliance on easy financial conditions have changed the game. Financial assets, namely stocks and housing, are responsible for much of the trends in not just economic growth, but employment, corporate capital expenditures and even the Federal deficit.

The financialisation of the economy is thus is an integral dynamic all investors should be aware of and appreciate.

Financial Assets & Employment

First and foremost, over recent decades there has been an increasing correlation between the performance of the stock market and the labour market, namely in the form of job openings. The growth rate of the S&P 500 mirrors that of the growth rate in job openings.

The relationship here is fairly intuitive, and starts with the actions of the Fed.

Easy monetary policy leads to higher stocks; higher stocks lead to more job openings; more job openings lead to higher inflation and low unemployment; higher inflation and low unemployment lead to tighter monetary policy; tighter monetary policy leads to falling stocks; falling stocks lead to falling job openings; falling job openings leads to falling inflation and rising unemployment; falling inflation and unemployment lead to easy monetary policy; easy monetary policy leads to higher stocks. And so the cycle goes.

What’s more, with the continued rise in passive investing and how these systematic flows are linked to employment, there is a level of self-reflexivity to this dynamic. As greater employment equates to greater total wages being paid, this subsequently results in greater passive flows into retirements accounts and thus monies into the stock market.

For a Federal Reserve intent on continuing down its path of tighter financial conditions for longer, the extreme financialisation of the US economy means that it will be nigh on impossible for the Fed to cool the employment market without a continued correction in equities, as well as lower house prices.

Financial Assets, Consumption & Economic Growth

Perhaps the most important consideration of how financialisation influences the economy is through the impact financial asset growth has on consumption and in turn, the business cycle. Financial assets growth - primarily a combination of equity and housing - are tightly linked to consumption. Given that consumption itself comprises roughly 70% of GDP, the implications are clear.

Clearly, much of the trends in consumption in recent years have been fueled by the growth in financial assets. This works both ways, and as a result the wealth destruction that has taken place in 2022 is likely to continue to weigh on consumption and economic growth throughout 2023. We saw just how powerful this wealth effect was to the upside during 2020 and 2021. Going forward however, this may to lead to the largest negative wealth effect since the global financial crisis.

Financial Assets & Government Tax Receipts

It’s not just the business cycle and employment impacted by financial assets, but government tax receipts are also reliant on asset price growth.

As we can see above, as stock prices, house prices and household net worth fall, tax receipts generally follow suit, and vice-versa. This dynamic has been increasingly apparent since 1995, when the US government made a change to the tax laws which incentivised companies to use stock-based compensation over cash-based compensation for sums over $1m. As a result, stock market related capital gains have become an increasing part of government tax receipts.

Should this relationship continue, then unless any drop in tax receipts is offset by a commensurate reduction in government outlays, further Treasury issuance will be required. This will only worsen the demand/supply imbalances already present in the markets and is a reason being pointed out by many why the Fed’s QT program will have to end. When foreign investors are now longer buying Treasuries on net and the Fed, there is only so much Treasury issuance that can be absorbed by the private sector before something breaks.

Nowhere is this dynamic being felt more than in California, a state which represents roughly 15% of US GDP. Here is a recent statement by a California finance department spokesperson on the matter (emphasis added):

“We have a very progressive tax system in California, and our fortunes are very much tied to the financial markets.

If you look at all of the personal income tax returns that were filed in California in the year 2020, just 1% of the total number of income tax returns that were filed were responsible for more than 49% of all of the personal income tax that was paid in that year. And unlike most of us who get our income from wages and salaries, that very narrow band of taxpayers derives a lot of their income from things like capital gains, stock markets [and] bonuses that are tied to corporate or stock performance. So when the markets are doing very well, those individuals are doing very well and state revenues are doing very well. Conversely, when the markets go south, their fortunes don't do very well and the state's revenues decline as a result.”

Given the majority of financial assets are held by the top 10% and the top 10% pay the majority of federal taxes, California’s woes are likely telling for the country as a whole. We have already seen November’s Federal tax receipts fall by $29b, or 10%, so unless we see a recovery in markets, future federal tax income looks to be particularly vulnerable.

Financial Assets & Corporate Capital Expenditures

Another consideration that has become dependent on the movements in asset prices is corporate capital expenditures. Corporate capex, is now largely a function of earnings and asset prices.

Financialisation has led us to the point whereby CEO’s these days are effectively paid to inflate earnings and boost stock prices. When the stock prices falters, their first point of call is to cut capital expenditures and employment. Decades of easy monetary policy have created a world where so much of the economy is linked to stock prices.

Implications Of Financialisation

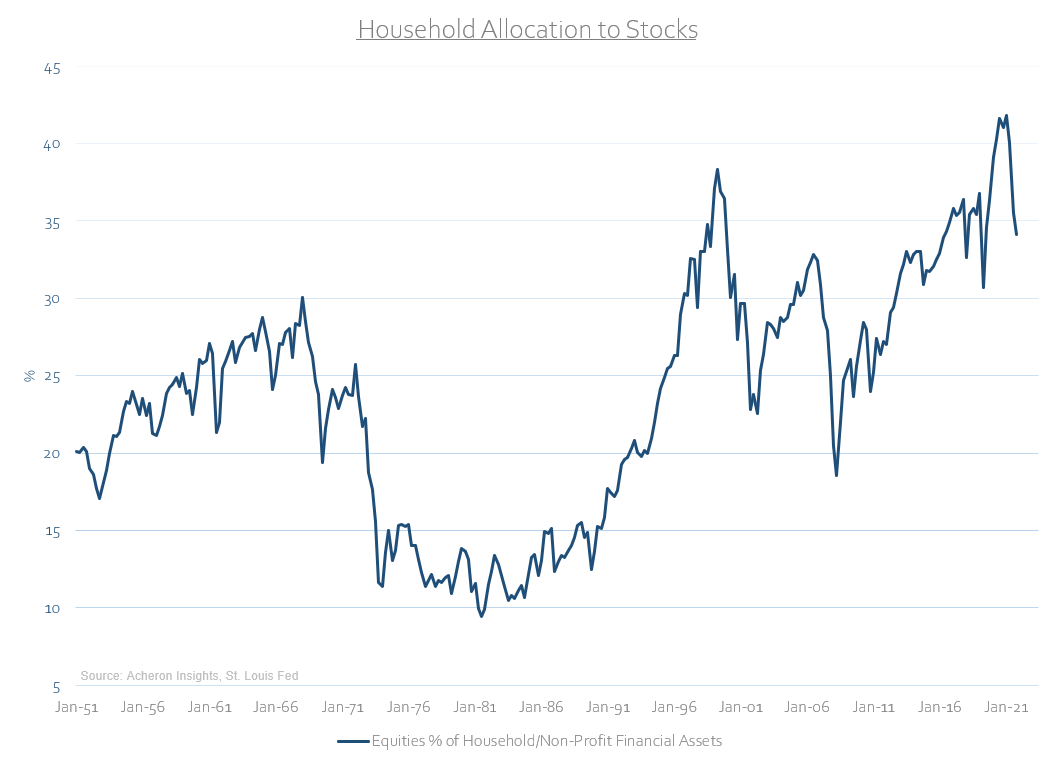

As we can see, further weakness in both the stock markets and housing market do not bode well for economic growth, employment or the Federal budget. Financialisation makes these areas of the economy particularly vulnerable to a falling stock market, especially when we consider the fact that households still have the highest exposure to stocks as a percentage of net worth of all time. Households could be subject to the most extreme negative wealth effect in history, of which the consequences will be felt throughout the entire economy.

Every time in the past decade the Fed has tried to step back and ease policy, things have broken. Due to inflation, this time around that is exactly what the Fed is trying to achieve. Powell and the Fed appear well aware of how financialised the economy has become. It is through the channel of tighter financial conditions and subsequent destruction of asset prices the Fed is trying to quell inflation. This very dynamic was noted recently by the Wall Street Journal’s Fed whisperer, Nick Timiraos:

“Fed officials say they combat inflation primarily by slowing the economy through tighter financial conditions—such as higher borrowing costs, lower stock prices and a stronger dollar—that curb demand. As a result, any easing of financial conditions while the Fed continues to battle inflation could raise the risk of a deeper or longer downturn if it prompts the central bank to keep lifting rates. As a result, any easing of financial conditions while the Fed continues to battle inflation could raise the risk of a deeper or longer downturn if it prompts the central bank to keep lifting rates.

Mr. Powell suggested the Fed would raise rates to higher levels for longer if broader financial conditions don’t “reflect the policy restraint that we’re putting in place to bring inflation down.”

It’s because of financialisation that Powell doesn’t want a big time equity rally. The Fed has so far achieved their goals of deflating asset bubbles with an economic crash. But, thanks to financialisation, this will soon change.

Indeed, so long as the stock market and the housing market continue to wane, economic growth will suffer.

We live in a time where asset price appreciation and economic growth and inherently intertwined. Welcome to a world of financialisation.

. . .

Thanks for reading!

If you enjoyed this article, feel free to share this with friends and around your network. Any and all exposure goes a long way and is very much appreciated. Thanks again.