The Stock Market Is At An Important Inflection Point

Within my latest piece discussing the merits of deflation, I briefly touched on how several leading economic indicators appear to be signally growth may have peaked for the time being. Whilst these business cycle and growth metrics are not necessarily useful on their own, when the price action of equities appear to be confirming the macro message; it may be time to pay attention. Such at time appears imminent.

Looking at two of my preferred leading macro indicators of the business cycle, the ERCI weekly leading index and global credit impulse, both are signaling peak growth may be in the rear view mirror.

Confirming this message are the most economically sensitive sectors of the stock market. Retail, transports, metals/mining, materials and the industrials sectors have all underperformed these last few months relative to the S&P 500. When the markets goes on the make a new high and all economically sensitive sectors such as these do not confirm the new high, it is a clear signal the new highs are not being supported by economic fundamentals.

Indeed, these recent highs have seen a significant rotation out of the reflation and value type sectors back into the growth darlings. Market breadth, another excellent measure of market internals, has too not confirmed the recent highs. We are seeing significant bearish divergences in almost all measures of breadth, and the recent rally is almost solely being driven by the likes of Apple and Amazon.

In the past, periods of poor breadth amid new highs in the major indices have generally lead to at least some form of correction or consolidation. It is perhaps unsurprising then to see that small-caps and emerging markets have gone nowhere over the past six months (in a similar manner to the economically sensitive sectors illustrated above) whilst the broad market has continued to march higher.

The market is now almost entirely being driven by a rotation out of cyclical sectors and back into tech, FAANG and defensive stocks.

Such periods of tech outperformance coinciding with the market cap weighted S&P 500 outperforming the equal weighted S&P 500 have been reminiscent of market tops in recent months.

Continuing this theme of non-confirmation are investor risk-appetites. Firstly, the pro-cyclical currency pair of AUD/JPY and AUD/USD both appear to be rolling over. The strength of the Aussie dollar is generally a good proxy for risk-on and risk-off type environments.

Extending this out to a longer-term perspective, another chart I referenced within my deflation article was the long-term AUD/JPY FX pair, which looks to have broken out of its bearish rising wedge pattern at the top of its near decade trading range.

Continuing with risk appetites via the VIX, which is effectively investors expectations of volatility over the coming month, the VIX has not made new lows over recent months as the market has gone on to make new highs. Such divergences between the two have typically preceded periods of market turmoil in the past.

Turning now to the technicals, they too are bear a similar message. On the weekly chart, we are seeing slight negative divergences in RSI and money flow, accompanied by a 9-13-9 weekly DeMark sequential sell signal.

What’s more, we are amidst a seasonally weak period of stocks, almost indicative of what I have detailed above. Clearly, we can see on many different measures that stocks are seemingly at risk of some form of correction, or at the very least, a period of consolidation.

In isolation, these indicators and measures are not of much use, but, in the case where they align to tell a similar story at once, it is important to take heed. I personally tend to favor trades and investment opportunities whereby fundamentals, technicals, sentiment and macro all align. For the most part, now appears to potentially be such a time.

However, I shall stress I am by no means predicting a significant risk-off event is imminent. For fear of being labelled a “perma bear”, let met be clear I am merely presenting a number of important measures investors should take heed of as part of their own due diligence and risk management. The clear takeaway from what I have presented above is that the risk-reward set-up for equities is not overly favorable at present. Nevertheless, there does remain pockets of value and opportunity still to be found within these markets.

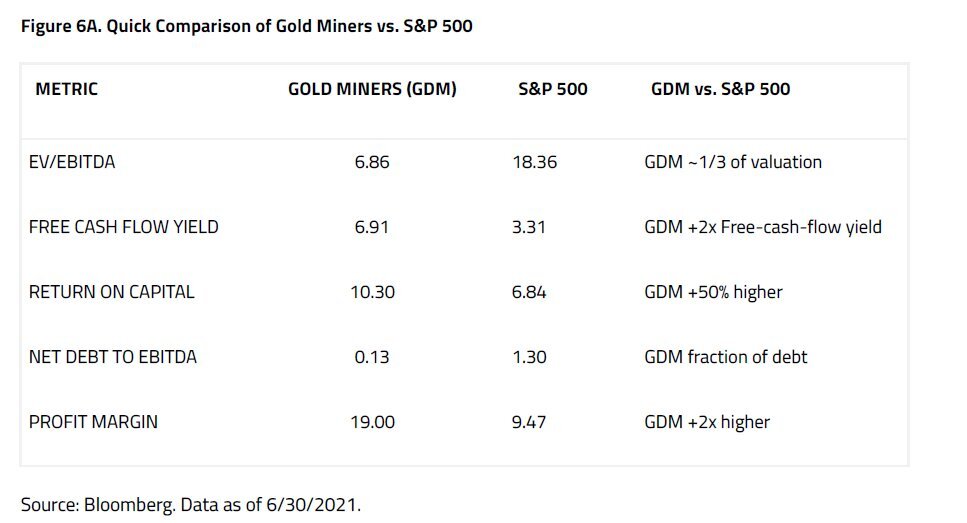

Those who have been readers of my previous writings will be well aware of how I have deemed there to be several decent buying opportunities in the gold and precious metals market of late. At the risk of repeating myself once more, dare I say it but today stands as another such opportunity for investors seeking to deploy capital. In terms of valuations and fundamentals, the gold miners are clear standouts.

Source: Sprott via Ronnie Stoeferle

However, fundamentals in isolation may not necessarily be meaningful if they are already priced in. It does however appear this is not the case. We can see this by comparing the divergence between the gold price and real interest rates. This is an inverse relationship that has historically nearly always held up, and is a key driver of the gold price. Given how real rates remain deeply negative today, it seems only a matter of time before the gold price catches up to real rates. One way to view this is by using TIPs as a proxy for real rates relative to gold.

Will gold follow real rates? Seasonality suggests it will.

To conclude, the market appears to be running our of gas. I for one would use a potential pull-back as a buying opportunity for several sectors and assets I am bullish on. I love the green-energy trades in uranium, copper and carbon credits, but, given how far these sectors and assets have come in the past year I would love to see further weakness before I begin buying. Again, that does not mean opportunities are not present right now, gold is perhaps the perfect example, and it looks like it may be an excellent time for investors to take profits out of the favored and deploy capital into the unfavored.