Once Again, It Is Time To Sell Bonds

Summary & Key Takeaways:

The outlook for the US economic is reasonable and inflation has likely bottomed. These are fundamental headwinds for the bond market.

Given inflation is set to bottom above target, long-term bonds are a useless buy and hold investment outside of a recession. There is unlikely to be a US recession anytime soon.

Not only that, but long-term bonds have already priced in most of the Fed’s easing cycle and the torrid outlook for the US fiscal and debt positions paints an unfavourable supply and demand imbalance moving forward.

Simply put, there is very little fundamental reason for a sustained duration rally, and the risk/reward will continue to be skewed to the downside for long-term bonds. Rallies should be sold, not bought. After all, why take on duration risk when you can utilise high yielding investment at the front end of the curve.

No recession on the horizon, so don’t bet on a bond rally

Since 2021, investors have primarily focused on the inflation side of the equation when assessing the outlook for bonds. Rightfully so. However, now that inflation has fallen back to the 2.5-3% range, the growth side of the equation appears to be back in the driver’s seat for bonds.

For bond bulls this has been a positive outcome over the past quarter. The US economy has largely surprised to the downside during this period, particularly on the employment front. With the monetary easing cycle now well underway, bonds aggressively priced in this economic weakness, pushing yields lower. Moving forward, I suspect this negative growth impulse is behind us. Expect economic growth to surprise to the upside over the medium-term.

Indeed, when we look at some of the short-term leading indicators of the business cycle such as ECRI’s Weekly Leading Index, along with the Economic Surprise Index for the US, this is the very message we are seeing.

The growth impulse is now to the upside, as are economic surprises. This explains much of the recent back-up in yields we have seen over the past couple of weeks.

Importantly, most of the leading indicators of the US business continue to suggest economic robustness moving forward. Yes, there will be short periods where growth disappoints and bonds can rally, but, with inflation still well above target, unless we get a recession, expect yields to continue to trend higher.

The recent fall in yields itself is likely to set the stage for them to reprice higher should these easier financial conditions translate into increased economic activity. We generally see this via the housing market (one of the primary cyclical drivers of the economy) as falling mortgage rates translate into increased mortgage applications and building permits.

Inflation risks on the horizon

On the inflation front, as mentioned, the picture has been relatively neutral for bonds in recent times. Although inflation remains above target, inflation volatility has largely disappeared as most inflation measures have hovered around 2.5%-3.5% with a slightly downward bias for much of the past 18 months.

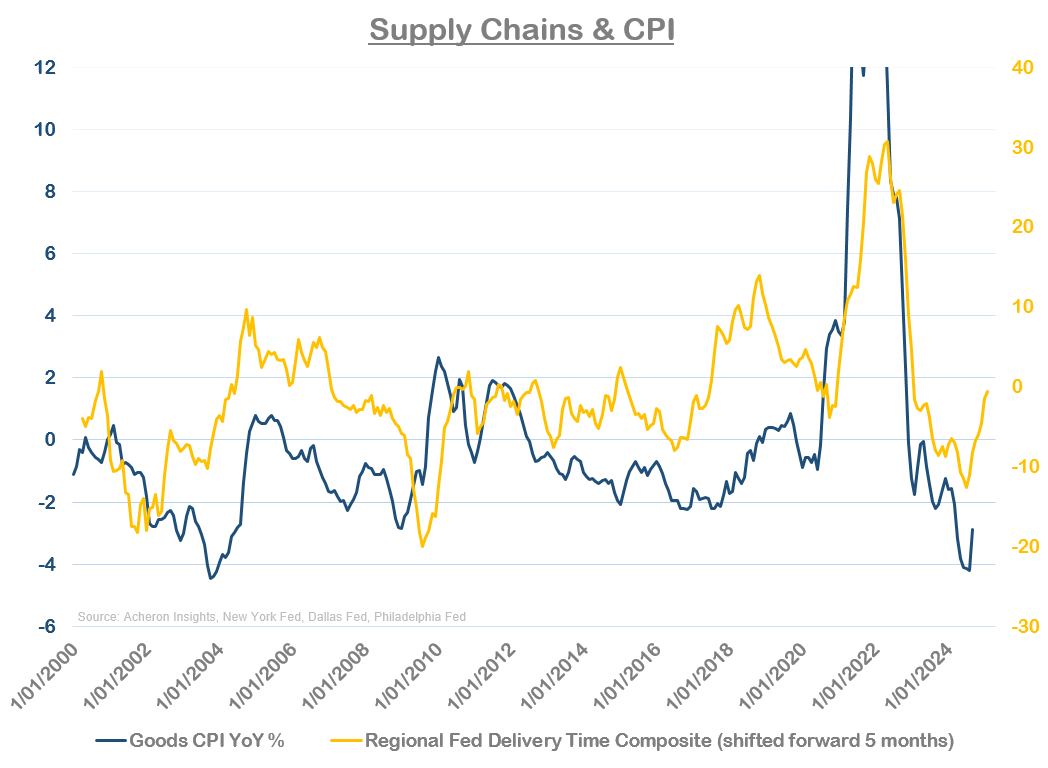

The three primary drivers of inflation (ex-food and energy) are Core Goods CPI, Shelter CPI and Services ex-Shelter CPI. Much of the decline in core inflation has been a result of a steady decline in Shelter CPI (both Rent and Owners’ Equivalent Rent CPI) and Core Goods CPI, the latter of which has been outright deflationary for some time now. On the other hand, Services ex-Shelter CPI - which is driven in large part by energy services - has been far stickier.

We now appear to be entering a time where Goods CPI is heading higher in addition to the downside move in OER CPI having largely exhausted itself. In contrast, Rent CPI and Services ex-Shelter CPI should continue to offer downside pressures for at least a little while longer.

The key takeaways from the inflation lead indicators above are that although we aren’t likely to see a significant move higher in the short-term, there is little evidence that inflation is going to move lower from here.

The outlook for Goods CPI may be the most important factor moving forward. Although it only contributes to around 18% of the Headline basket, the downside impact from Core Goods deflation to CPI cannot be overstated. Now, this deflationary impulse is likely behind us.

There are a number of other inflation lead indicators which also continue to point to moderate upside pressures ahead.

The dollar is one. It suggests that in six-months time CPI will be at least equal to where it was 12 months ago (which is nearly 1% higher than the current 2.4% YoY figure).

Financial conditions are also sending a similar message.

In summary, as I have stated numerous times recently, though not yet material, upside inflation pressures are returning and are likely to result in a higher inflation number in the next six to 12 months than we have at present.

Robust economic growth and upside inflation pressures are not an ideal combination for long-term bonds, particularly when yields are already lower than where they should be relative to current inflation figures.

Bonds are overvalued

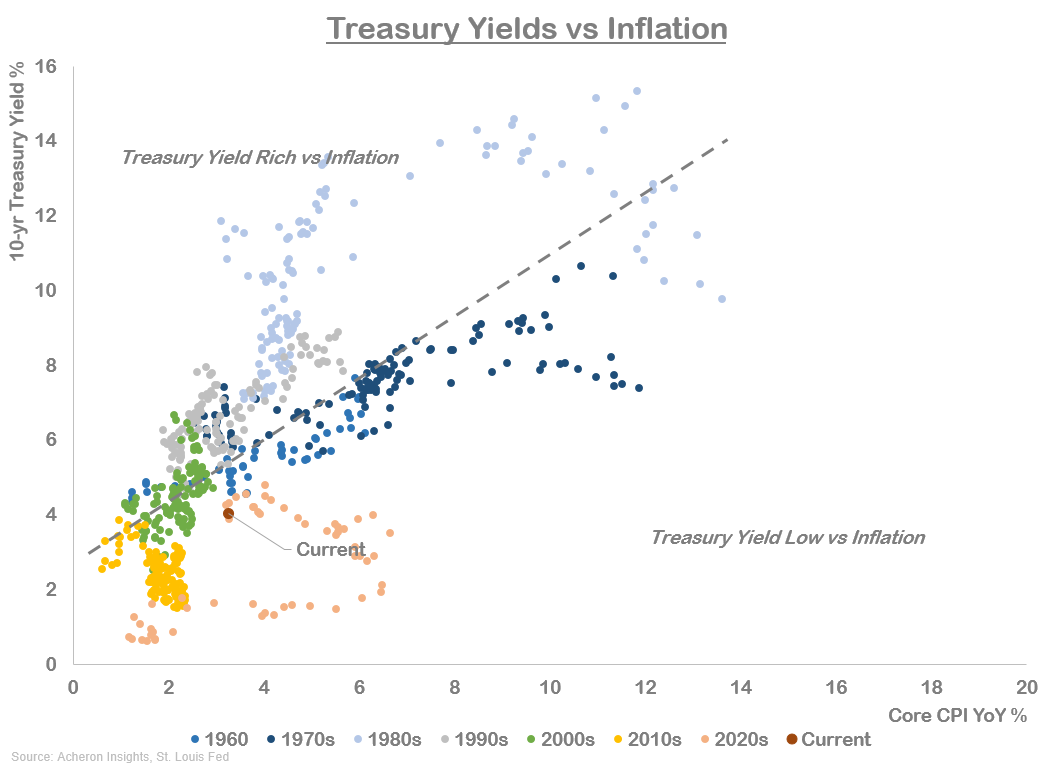

So far, we have established the outlook for the economy remains robust and the outlook for inflation is also skewed slightly to the upside. We have also seen that relative to current inflation figures, yields are seemingly lower than where they should be based on the historical relationship between the two.

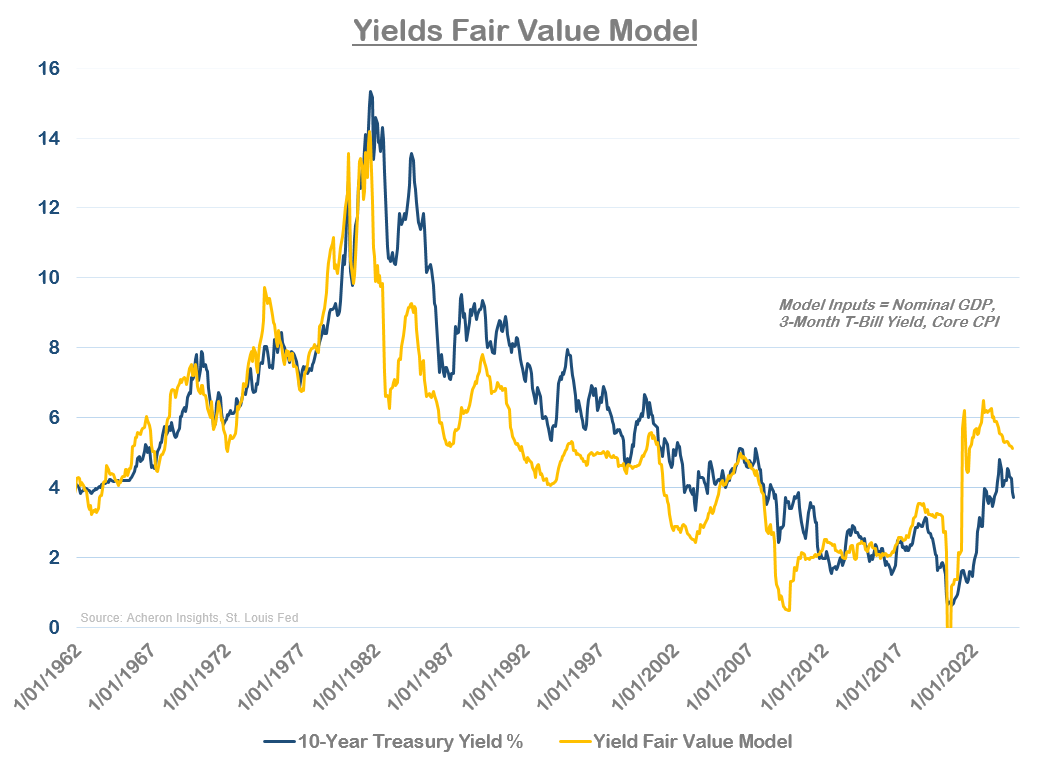

If we extend this analysis further and compare current yields to a combination of fundamental data points (GDP, Core CPI and T-Bill yields), bonds appear as overvalued now as they were at any point from the mid-1980’s to the early 2020s.

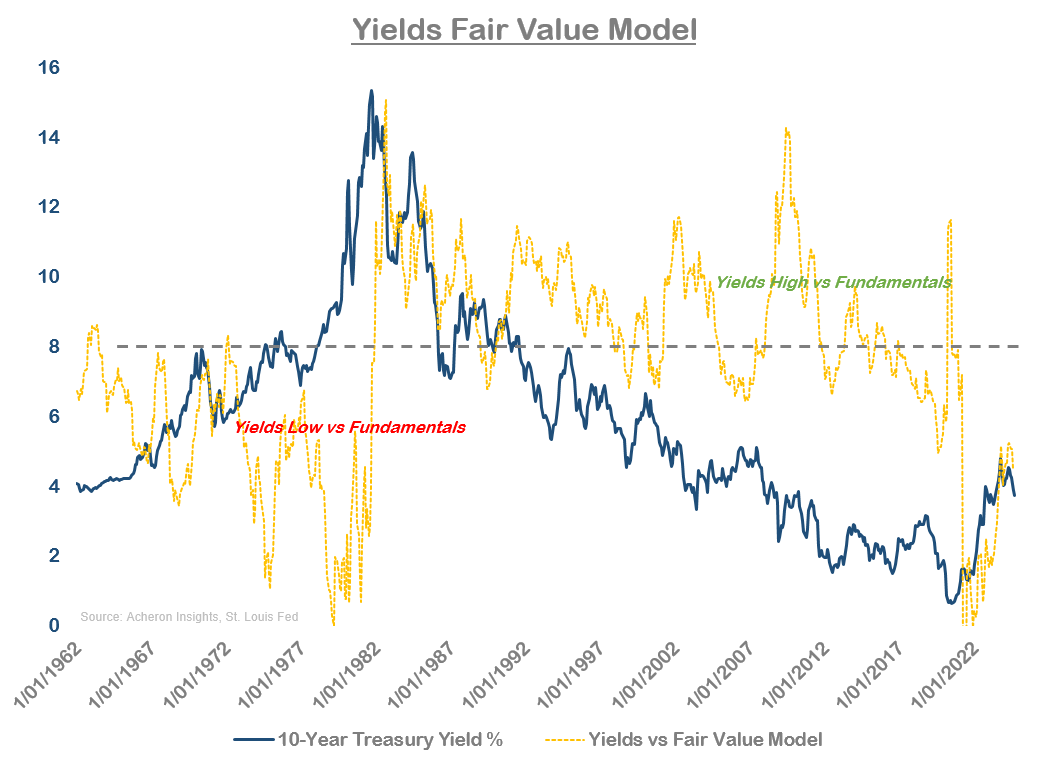

Not only are long-term bonds overvalued versus fundamental data, but versus the Fed Funds rate, long-term yields still appear too low.

Perhaps a more meaningful comparison is Treasury yields and mortgage yields. Mortgage yields generally trade at a slight premium to Treasury yields, but, as we can see below, this premium appears too low at present. Clearly, Treasury yields are either too low relative to mortgages or vice versa.

Too much supply and not enough demand

Adding to the bearish outlook for bonds is the structural supply and demand imbalance stemming from the US governments worrying debt and deficit position.

What has been a significant driver of debt issuance from the US Treasury in recent times has been falling tax receipts and rising interest costs, as we can see below. Although tax receipts have rebounded in 2024, the Federal Government’s interest expense is yet to move lower despite the recent drop in yields. If you want to understand why the Fed is easing monetary policy despite little supportive fundamental data, look no further than the yellow line below.

While we should see the government interest expense move lower to some degree as a result of the recent decline in yields, the fact it has yet to do so is telling.

However, the Federal Government should see some relief on the tax receipts front for the rest of 2024 as a result of the recent bull market in equities and appreciation in household net worth (given capital gains taxes are a large portion of total tax receipts).

And yet, despite these seemingly positive developments for the Treasury Department, forecasted quarterly borrowing needs continue to be upwards of $500b.

This is the world we seemingly live in. One of fiscal spending unlikely to change anytime soon.

With foreign investors no longer buying US Treasury’s on net, until the Fed starts up QT once again the burden falls on the private sector to fund the deficits. So long as this trend goes on, they will demand a higher premium for doing so.

One reason as to why long-term bond yields did not re-rate higher to the extent they should have over the past two years given these dynamics is a result of the US Treasury Department favouring the issuing of short-term debt securities over long-term bonds. This was undertaken in order to make use of the Fed’s Reverse Repo (RRP) facility that was flush with cash following the COVID QE period, and has been an excellent move by the Treasury.

Now, the Fed’s RRP facility is nearly depleted, meaning the US Treasury is increasingly required to issue longer-dated bonds as opposed to short-dated T-Bills, which has started to occur throughout 2024. Again, the longer this goes on, the more pressure long-term yields will have to the upside, especially when both growth and inflation are far from fundamental tailwinds.

A consensus investment

Although the fundamental bear case for bonds is not as strong now as it was in 2021 and 2022, there clearly remains very little upside for taking on material duration risk over the medium-term.

What’s more, owning bonds remains a pretty consensus trade among investors. While TLT short interest is not at the lows it was in 2023, fund flows into TLT over the past quarter have been significant.

There remains a consensus view bonds are going to rally significantly at some point, and investors have been happy to pile into duration risk accordingly. While this has worked modestly over the past quarter, I don’t expect it to continue.

When we look at other survey-based sentiment measures such as the Conference Board Bond Survey (which measures the net percentage of consumers expecting bond prices to rise), we can see there is presently an extreme bias toward bond bullishness.

Does this mean bonds are going to crash in the immediate future? No. I actually expect bonds to hold up modestly over the medium-term. The point it, there is very little fundamental reason for a sustained duration rally, and the risk/reward will continue to be skewed to the downside. Rallies should be sold, not bought. After all, why take on duration risk when you can invest in low duration yield ETFs with little or no duration risk? Seems like a no brainer to me.

. . .

Thanks for reading!

If you would like to support my work and continue to allow me to do what I love, feel free to buy me a coffee, which you can do here. It would be truly appreciated.

Regardless, feel free to share this with friends and around your network. Any and all exposure goes a long way and is very much appreciated. Thanks again.