Oil: The Top Is Likely In For Now

Summary & Key Takeaways:

Elevated positioning, bullish sentiment and falling refinery margins continue to suggest this move higher in oil prices is probably done.

However, prices should be well supported on the downside, with OPEC+ supply greater than consensus believes and a pick-up in global growth underway.

As such, we are likely to see a rangebound market for the foreseeable future, one that is well supported on the downside but capped on the upside. We may well be at the top of that range right now.

Don’t expect much upside in oil prices from here

Back in March, I penned an article opining why oil prices are probably at or near a local high. WTI was around $82 at the time and has since moved marginally higher to the $85 level we sit at today (down from a high of $87 last week). At the time, my argument was based on a number of fundamental and positioning indicators which were suggesting oil prices would struggle to move meaningfully higher. I was never expecting an imminent correction (nor am I at presently), but instead continue to hold the opinion oil prices are probably at the top of their range for the time being.

Central to this thesis is positioning. Measuring positioning in WTI via managed money net longs as a percentage of total managed money open interest, we can see the hedge funds and CTAs who make up this category of the futures market are currently bullishly positioned to such an extent it often coincides with intermediate market tops.

Can positioning become more extreme from here? Sure. But historically, when managed money is positioned as bullishly as they are today, future returns are generally limited. This notion is particularly noteworthy when we consider how frothy oil market sentiment has become. Forecasts and predictions of $100+ oil are popping up left right and center, particularly from the institutional coverage side of things.

What is perhaps even more notable however is refining margins (i.e. crack spreads) peaked some weeks ago and have been moving lower amidst the latest rally in crude. This is true of WTI cracks…

And importantly, is also true of European and Singapore cracks, which are represented by the blue and green lines below.

Refining margins have been an important driver of oil prices in recent times, with the rise and subsequent fall in WTI cracks leading price throughout much of 2023 and 2024. In a supply constrained market, refinery demand is key.

On the inventory front, the picture has been largely supportive of oil prices over the past few weeks. Total crude and petroleum inventories as well as just crude inventories have seen persistent bullish inventory changes of late. That is, either builds below seasonal averages or draws greater than seasonal averages.

The last couple of weeks however have seen a couple of unfavourable crude inventory changes. As such, the inventory picture has now moved back toward neutral territory, with both total crude and petroleum inventories as well as crude inventories sitting in-line with their five-year seasonal averages. Though it’s worth noting distillate and gasoline stocks remain well below seasonal norms, as has been the case for some time now, hence why gasoline and diesel prices have been well supported.

Moving forward, we may be entering a period in which crude oil inventories build. Oil demand from refineries has now returned to seasonal norms on the back of elevated crack spreads following maintenance season, but we do tend to see a lull in the second half of April and throughout May as refined product demand lessens during this period of the year. And, with crack spreads also moving lower, the incentive for refiners to increase crude oil throughput is lower than it was a month or two ago.

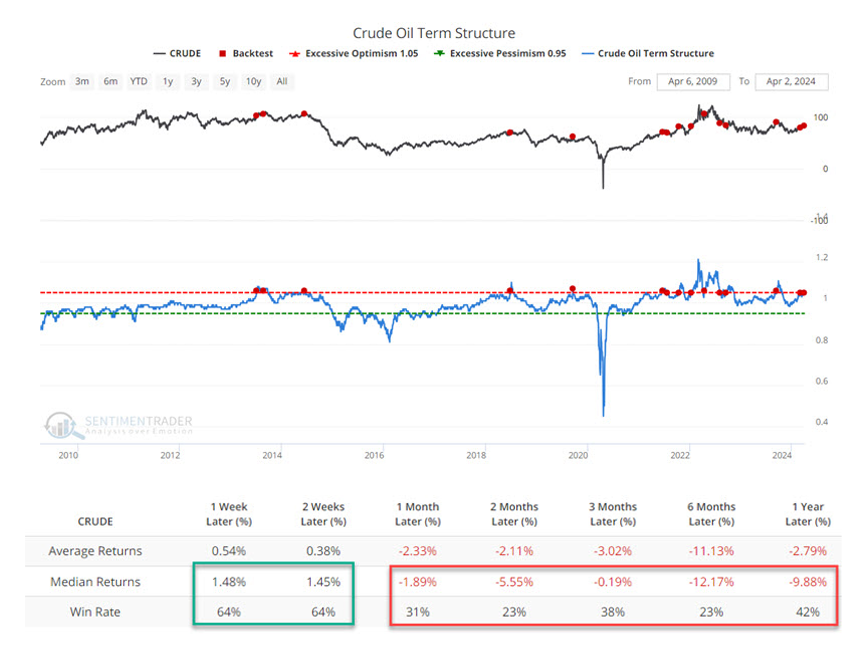

Elsewhere in the physical market, the prompt futures spreads continue to be heavily backwardated, very much signaling a tight market. However, while backwardation is indeed a bullish signal, extreme spikes in prompt spreads are generally associated with intermediate tops in price, as we can see below.

Source: SentimenTrader

Putting it all together, there is no doubt oil prices can rally further from here. But, with positioning and sentiment reaching levels not seen since the October highs, the market would need to significantly tighten to move materially higher. And, with refining margins moving lower and not supporting the recent highs, it is likely this move higher in oil prices is probably done.

A quick word on OPEC and the outlook for the rest of 2024

Having said that, it is also worth reiterating the strong underlying fundamentals which should support prices fairly well for the rest of 2024 and put a solid floor under the market.

At the centre of these favourable fundamentals is OPEC+. The general consensus is OPEC+ is driving prices higher through their production cuts. While they are indeed cutting production, we must remember production does not equal supply. As we can see below, actual OPEC+ crude exports are close to five-year highs, while production is close to five-year lows. OPEC+ continues to supply plenty of oil to the market.

The fact we have an oil market as tight as it currently is while OPEC+ is actually exporting almost as much oil as it has at any point over the past five years is bullish. While it is still a risk for the oil market if Saudi Arabia decides to regain market share and boost production (this will happen at some point), this dynamic seemingly becomes much less of a headwind when we understand that OPEC+ and Saudi Arabia are actually exporting as much oil as they are, despite the drop in production. The risk of OPEC+ supply surprising to the upside is not as great as many believe.

In addition to OPEC+ supply being greater than expected, other factors that should put a floor under oil prices are as follows:

US oil production may be slightly overstated as a result of the EIA’s adjustment factor, meaning US production could surprise to the downside from here;

Chinese inventories have moved appreciably lower over the past quarter; and,

Demand is on solid footing, with global growth likely to pick-up in 2024 and the northern hemisphere’s driving season just around the corner.

With these ongoing dynamics in mind, oil prices are likely to be well supported for much of 2024. But we are in an election year, so there is likely also a ceiling on prices. Thus, we are likely to see a rangebound market for the foreseeable future, one that is well supported on the downside but capped on the upside. We may well be at the top of that range right now.

. . .

Thanks for reading!

If you would like to support my work and continue to allow me to do what I love, feel free to buy me a coffee, which you can do here. It would be truly appreciated.

Regardless, feel free to share this with friends and around your network. Any and all exposure goes a long way and is very much appreciated. Thanks again.