Crypto Market Outlook: Nearing A Make Or Break Moment

After what has been a torrid few weeks for crypto and traditional risk assets alike, we are beginning to enter what could be an important make or break point in time for crypto markets. Whilst the euphoric sentiment towards Bitcoin has been largely washed out amid this pullback and on-chain data is beginning to appear more favourable, we are nearing some very important key technical levels for both Bitcoin and Ethereum. Furthermore, the apparent slowing economy is unlikely to bode well for risk assets in 2022, especially crypto, and thus represents the big headwind facing the market for the foreseeable future. Though we could see positive price appreciation within the early months of 2022, for those betting on $100k bitcoin and $20k Ethereum in December 2021, it is time to reign in your expectations.

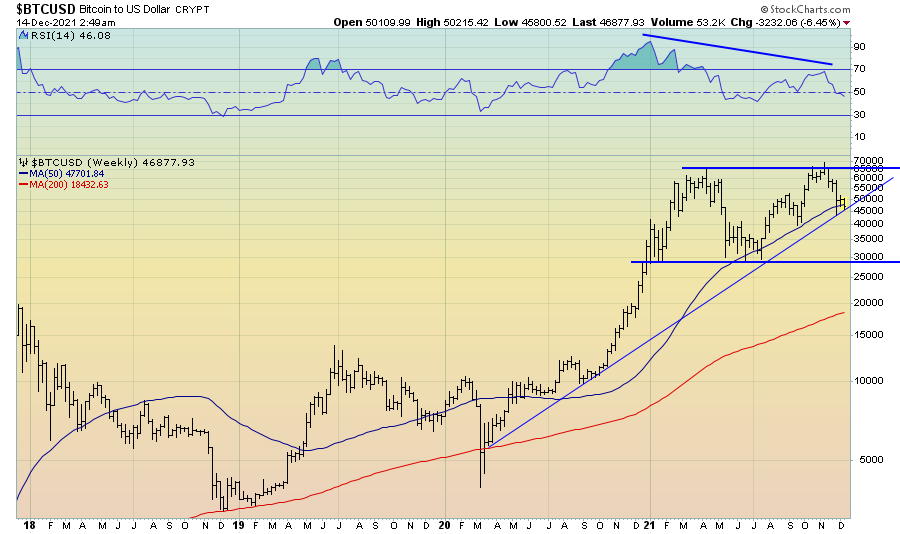

After what proved to be a false breakout attempt to new all-time highs in early November, BTC now lies right at the confluence of the 50-period moving average on the weekly chart and the ascending trendline that has held up well thus far since the March 2020 lows.

This 50-period moving average on the weekly chart (blue line above) has been an incredibly important resistance level throughout 2022, and if broken, could see BTC retrace back down to the $30k level in short order, an area that appears to be the lower resistance level in what has been a large consolidation range.

On the daily chart, the 200-day moving average is the key area to watch. Should this level continue to hold, we could potentially see the psychological $50k level retaken and presage a nice bounce into January, though if the 200-day moving average does not hold, a further flush to the $40k-42k seems likely.

Ethereum meanwhile has shown significant relative strength over recent months. Key support lies around the $3,600 area which the price has bounced off nicely in recent days. Below that, $2,900 looks to be the next key level along with the 200-day moving average; not a bad area to go long.

What remains in ETH’s favour for now is the recent breakout of the ETH/BTC spread. This ratio looks to be trying to turn the key 0.08 level that was once resistance into support.

If this level holds, we should expect ETH outperformance to continue. Should the market indeed bounce over the next month or two, ETH could well be the place to be relative to Bitcoin.

Turning now to investor sentiment, we have seen this recent correction wash out much of the bullish sentiment towards the crypto markets that was evident in November. The Bitcoin Fear & Greed Index has now fallen to levels reminiscent of decent long-term buying opportunities in the past.

Confirming the wash-out in sentiment is the Bitcoin Optix, which too has reached levels supportive of a potential short-term bottom possibility forming.

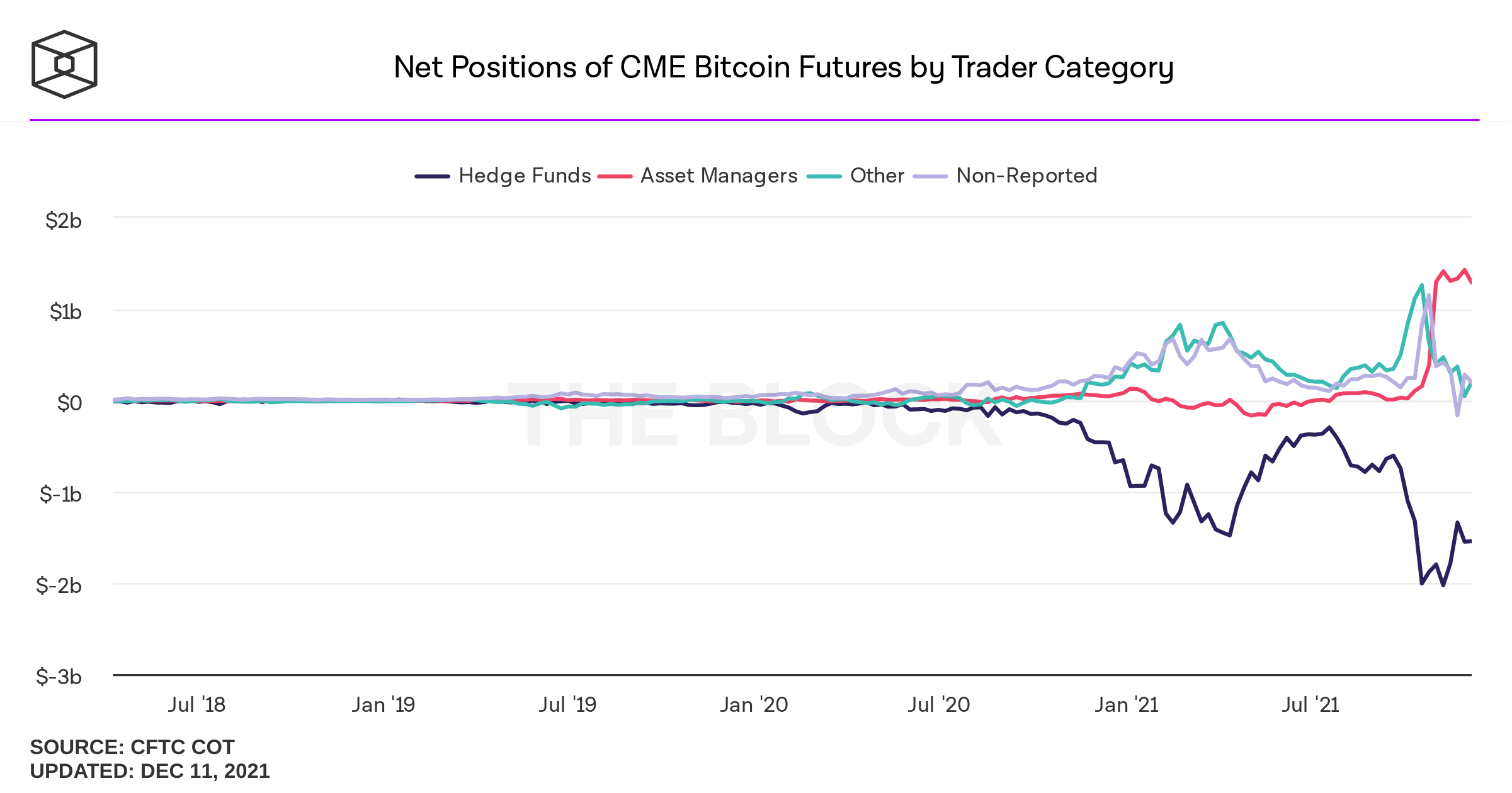

Positioning in the futures market is also beginning to look somewhat more constructive for BTC. If we look at the Other and Non-Reported categories below, representative of small speculators within the futures market (i.e. the dumb money), both have significantly reduced their net-long positions to a level similar to the May to July lows. Speculators in the futures market tend to be long at the tops and short and the bottoms.

Source: Crypto Quant

Conversely, hedge funds, who in the BTC futures market tend to be long (or less short) at the bottoms and heavily short at the tops, have reduced their short positions to a certain extent amid this current pullback, though not nearly to the level seen at the July lows earlier this year.

Whilst not pictured, we are yet to see a washout in speculative positioning in the futures market for ETH, which is unsurprising given its recent relative strength. This does however lead me to believe ETH has more downside potential relative to BTC at present, and if this market were to continue lower then ETH could play catch up to downside. We are seeing similar messages for ETH relative to BTC in the futures open interest data and perpetual funding rates.

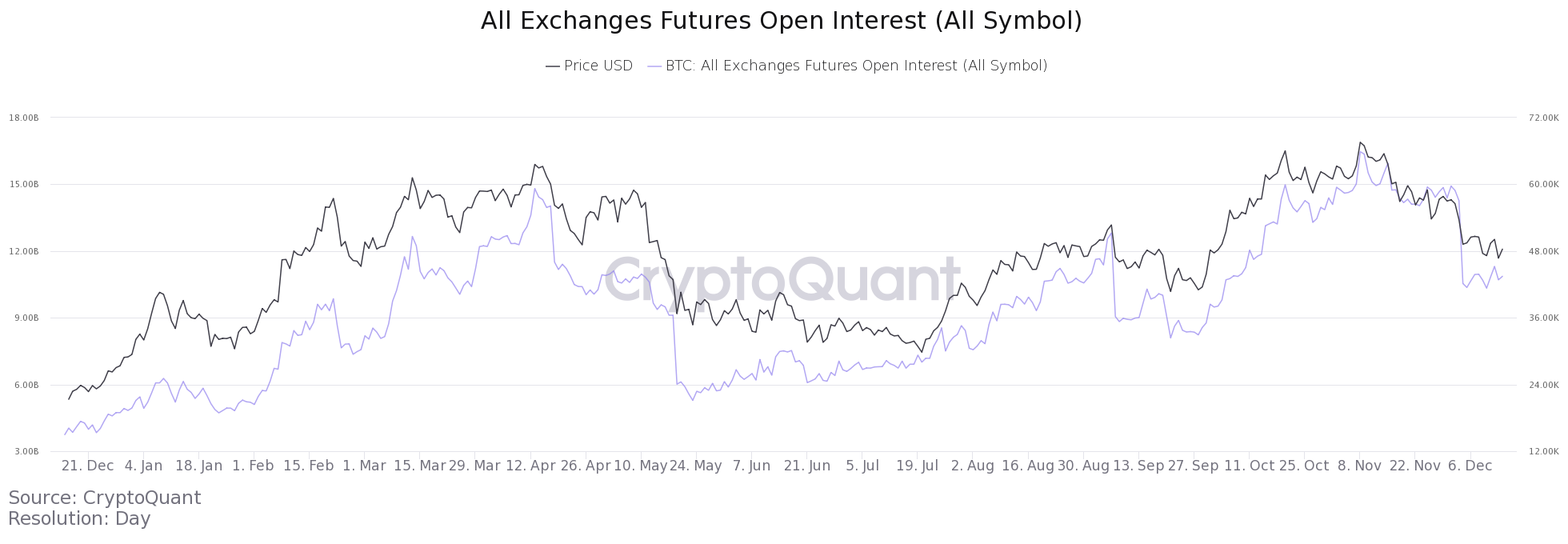

Indeed, we have seen a significant reduction in open interest in BTC futures of late, indicating a reduction in the excess leverage in the system, though the total open interest still remains at elevated levels relative to what we have seen during 2021. However, it is important to consider how this open interest data is being effected by the introduction of the Bitcoin futures ETFs in recent months. As the futures market is generally used for traders of a short-term time frame due to the excessive roll costs associated with holdings futures contracts for long time periods, buyers of the Bitcoin futures ETF who intend to hold for the long-term would cause the open interest data being skewed to the upside.

Source: Crypto Quant

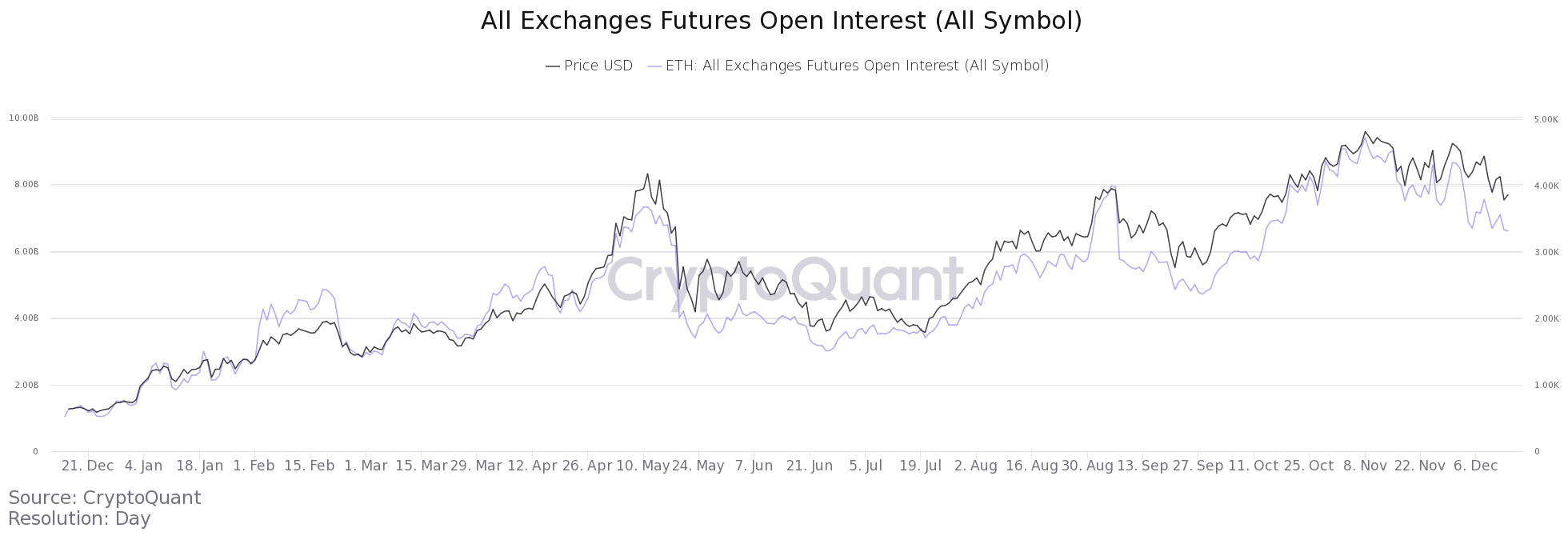

This does not mean we should dismiss the open interest data completely, particularly when ETH open interest remains at particularly excessive levels, as we can see below.

Source: Crypto Quant

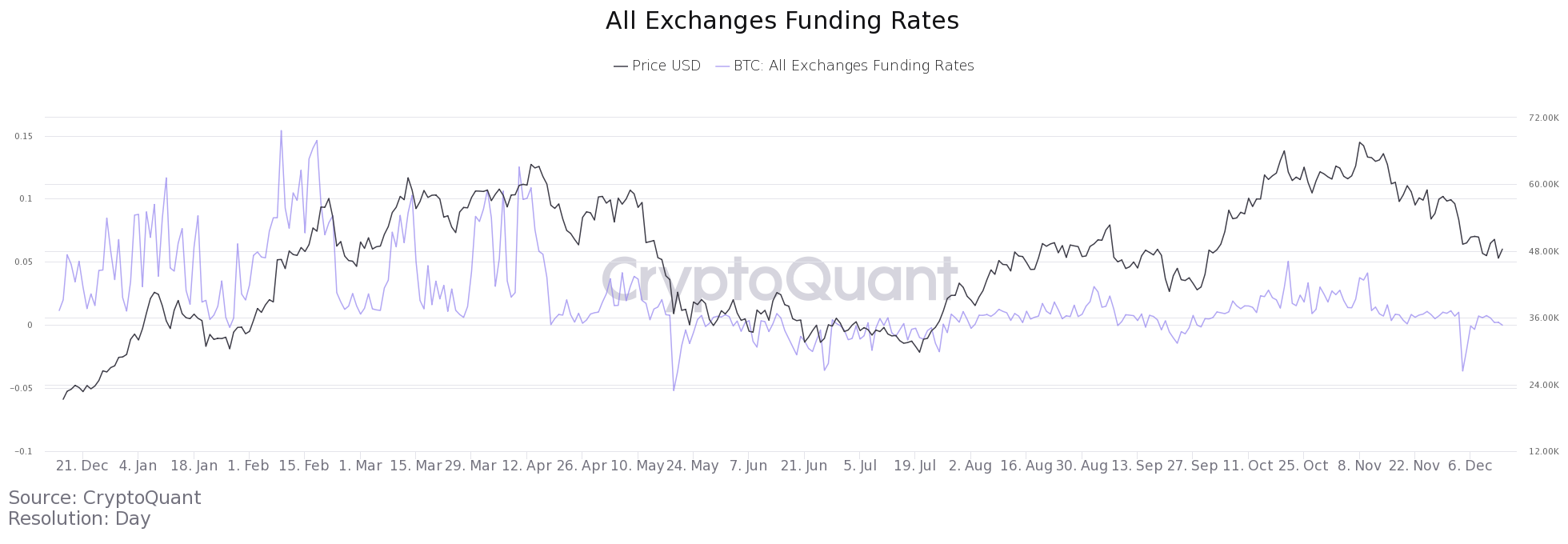

Perhaps a better measure of leverage within the system however are the futures funding rates. Funding rates are indicative of the directional bias of leveraged positioning. When positive, long traders pay premiums to shorts, and when negative, shorts pay premiums to longs. Positive spikes generally indicate extreme optimism whilst negative spikes often indicate extreme pessimism.

We saw BTC futures funding rates go heavily negative in early December and have since stabilised around neutral territory. This is certainly positive, clearly telling us that much of the leveraged long BTC positions have been wiped out, though this does not necessarily mean further downside is not a possibility.

Source: Crypto Quant

Turning now to some of the On-Chain analytics, what is interesting is the precarious position we currently reside in for several of these metrics and how they are aligning with the important technical levels highlighted above.

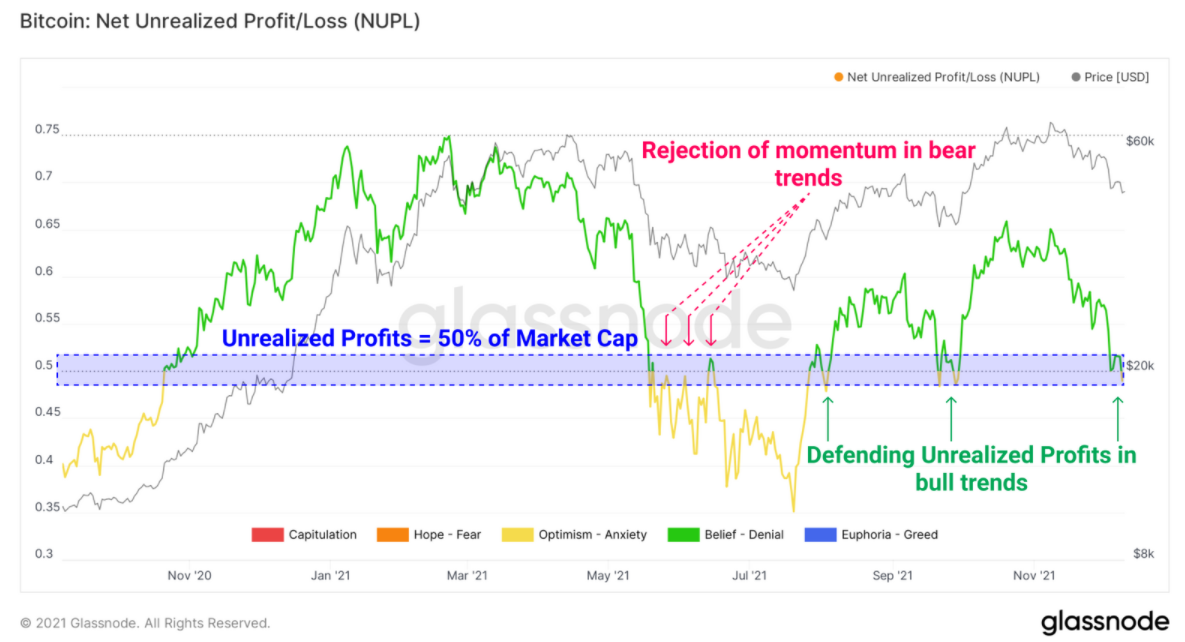

As noted this week by Glassnode, the net unrealised profit/loss (NUPL) metric for BTC has established a clear level of resistance around the 0.5 area.

Source: Glassnode

Should this level fail to hold, it would presumably coincide with a break of the 200-day moving average and would likely presage another move lower. Should it hold, then those who have bought this dip are likely to be rewarded.

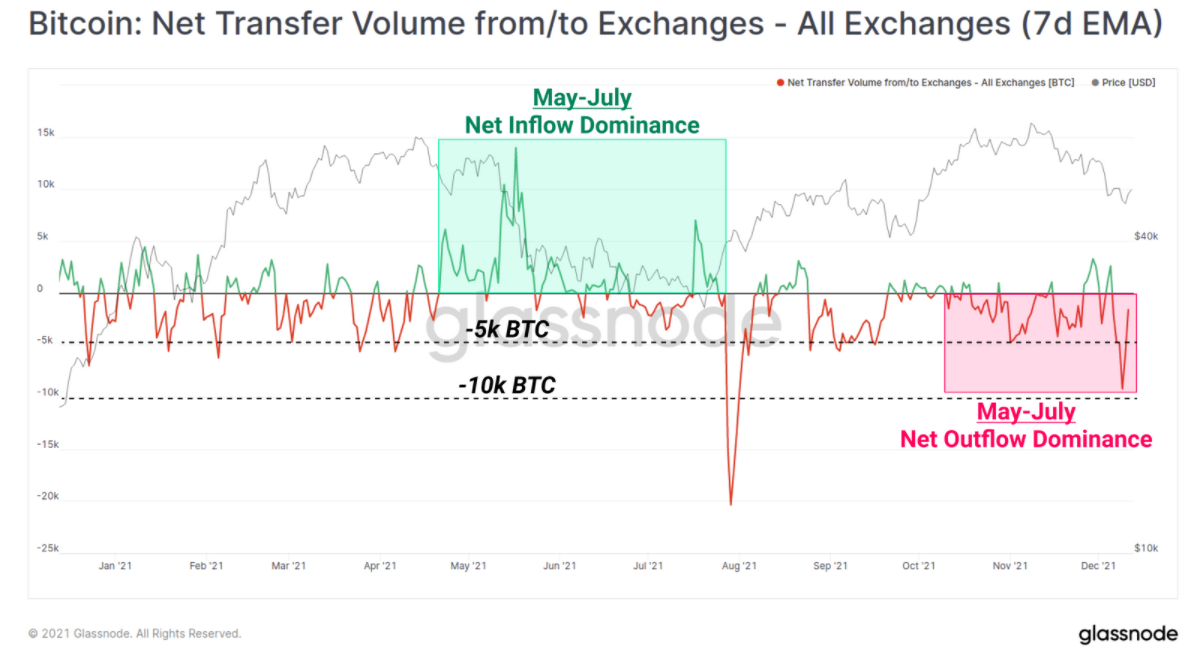

Encouraging though from an on-chain perspective is that we are witnessing BTC holdings being transferring from on-exchanges to off-exchanges. Falling exchange balances could indicate accumulation by long-term holders, whereas transfers on-exchange are generally indicative of selling pressure.

Source: Glassnode

To me, the signal form the on/off-exchange movement is twofold; first, long-term holders are buying this dip in earnest and locking away their holdings off-exchange without the intent to panic-sell; and second, we are yet to see a true capitulation from these long-term holders that would indicate a true market bottom, similar to what we saw during the July bottom. As such, I find difficultly in extrapolating a clear message from the exchange-flows activity, so take from it what you will.

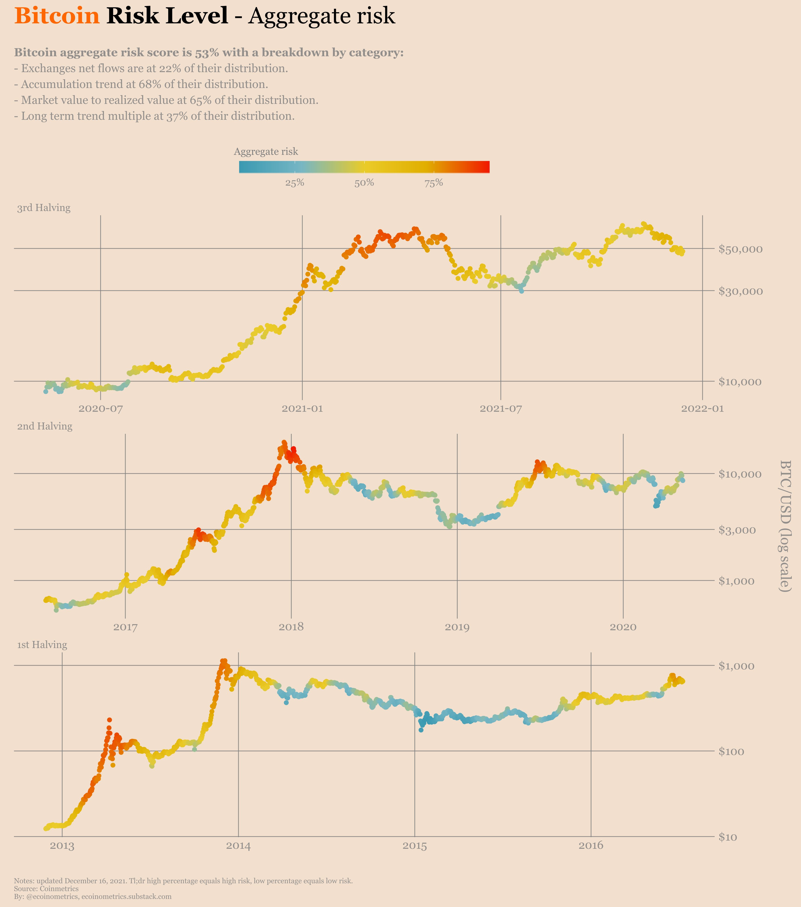

From an aggregate on-chain risk perspective, the market is still far from overheated, but neither are we near an aggregate risk level seen at past long-term market bottoms, as per Ecoinometrics.

Source: Ecoinometrics

Looking towards the macro and economic growth cycle and their implication on crypto; I believe the potential resumption of the deceleration of growth in early 2022 to be a significant headwind for all crypto markets over the medium-term, particularly given how retail driven and pro-cyclical crypto has become of late.

As I detailed within my most recent Growth Cycle Outlook, a deceleration in the rate of change of growth and inflation, monetary tightening into an economic slowdown, a fiscal cliff and diminishing liquidity conditions all have the potential to rear their ugly heads as early as Q1 2022. Throw in strong dollar and we have the ingredients for a lull in risk assets.

Indeed, what we do know certain is historically, BTC has not performed well in environments whereby both growth and inflation decelerate on a rate-of-change basis in tandem, courtesy of the great work by Darius Dale of 42Macro.

Source: Darius Dale - Bitcoin historical performance vis-à-vis macro regime.

For reference, the above macro regimes as per the work of 42Macro are categorised by the direction of the rate-of-change of both growth and inflation. Goldilocks represents periods whereby growth accelerates and inflation decelerates, Reflation where both growth and inflation accelerate together, Inflation whereby growth decelerates and inflation accelerates, and Deflation whereby both growth and inflation decelerate. It is always important to remember, what primarily impacts asset prices and financial markets is the direction of the rate-of-change in growth and inflation.

Additionally, given how much discretionary spending has played a part in the crypto run-up of late 2020 and early 2021, we are entering a period whereby these conditions are no longer present. Inflation is eating into demand and real income growth is negative. Though we have witnessed a small bounce in growth throughout Q4 relative to Q3 and one that may even extend into early 2022, said bounce is running out of fumes and defensive assets are now leading the charge in traditional financial markets. Investors cannot assume 2022 will be the same as 2021.

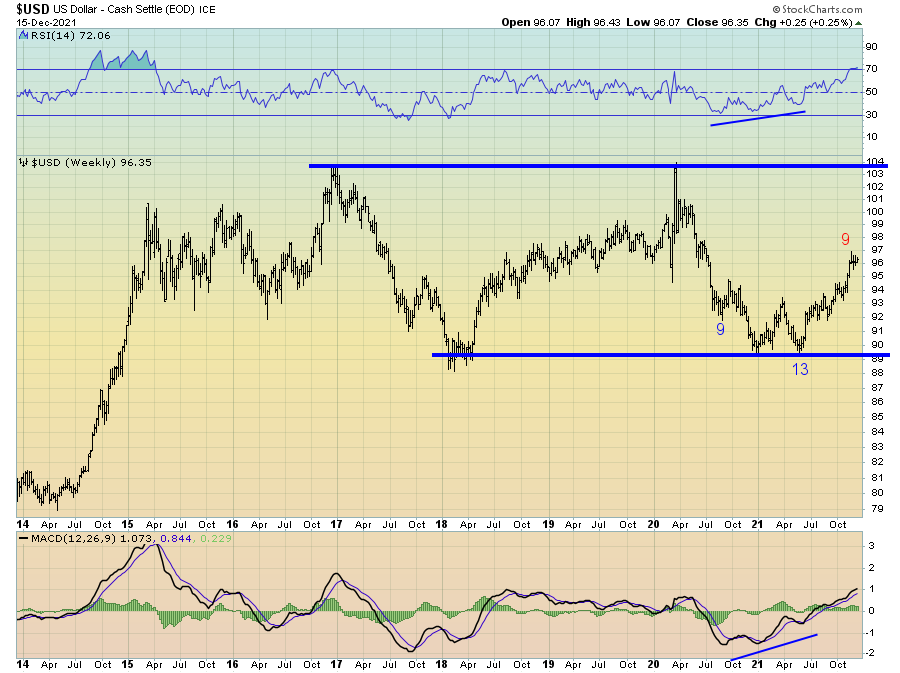

However, if we see the dollar correct somewhat in the coming month or two (or even continue to consolidate), as the weekly DeMark 9 sell count is suggesting it may, this scenario may ease some of the pressure on risk assets and potentially allow crypto to rally into January.

I do however expect to see the dollar to continue to move higher next year, potentially even as high as 103 on the dollar index. This is an area which has marked the top of what has largely been a rangebound market over the past half-decade.

In summary, both the bull case and the bear case have merit for crypto over the coming months. Investor sentiment has largely been washed and is beginning to look favourable, so too in regards to leverage within the futures market. Additionally, we are not seeing any major red flags from the on-chain data. However, the macro headwinds could cause some pain in the next quarter or two. Will we see the market rally into January and February? Quite possibly, particularly so if hedge funds and institutions enter the market as they reset their books for the new calendar year.

What is certain is risk management has never been as important as it is now.