A Buying Opportunity In Energy

Summary & Key Takeaways:

Sentiment towards energy and oil is as bad as it gets.

But, a number of fundamental indicators of the oil market are slowly turning bullish.

Therefore, with speculative positioning as bearish as it’s been in years and geopolitical risks again on the rise, we look to be setting up for a meaningful rally in oil prices.

Slowly but surely, the oil market is taking a bullish turn

One of the things I like most about commodities and energy in particular is their volatility, as volatility brings opportunity. Oil prices fell roughly 30% from their peak in October to the December lows, while energy stocks did not fare much better. But, as I detailed a couple of weeks ago, the oil market has been in a process of recovery, and now, with sentiment as bearish as you will ever see, a bullish setup seems to be developing.

Dare I say it but it looks increasingly likely the lows are in.

First and foremost, the collapse in gasoline crack spreads that unlimitedly proved to undo the Q3 rally amid a period of horrid seasonal demand continue to recover off their early November lows. This is true of both US gasoline cracks as well as those in Europe and Asia, and is a key ingredient to both providing a floor for oil and driving a move higher.

This is exactly what bulls want to see as rising gasoline cracks (in addition to still elevated diesel cracks) should help encourage refineries to continues to increase crude throughput as they make the most of higher potential profit margins. This is indeed what has happened in recent weeks as refinery throughput and utilisation rates have been on the rise.

While deteriorating fundamentals played a role in the recent rout in oil prices, seasonality was also a major factor. October and November are historically the most bearish months for oil and energy prices as this period follows the northern hemisphere summer driving season that sees refinery runs drop as refinery maintenance picks up (as we can see below).

Other bearish factors such as the annual Mexican oil producers Hacienda hedge also take place during this period. Now, these seasonal headwinds look to be turning to tailwinds as we enter a more favourable time of the year for both demand and prices.

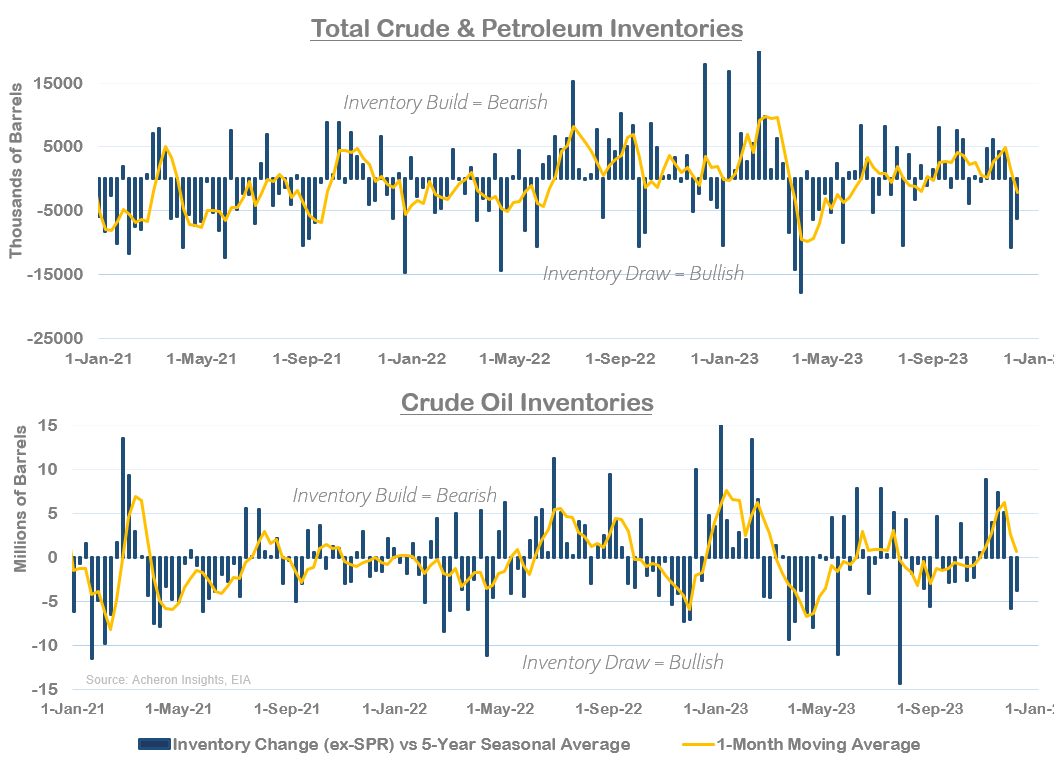

Thus, with gasoline cracks on the rise and refinery demand following suit, to confirm any kind of tightness in the market these dynamics should bring, we need to see crude and total petroleum inventories experiencing draws below seasonal averages. Fortunately, this is exactly what has occurred in recent weeks, with total crude and petroleum inventories seeing their largest consecutive inventory draws relative to seasonal averages since Q2.

However, for any kind of sustained rally to ensue, we need to see a period of persistent inventory draws such that total crude and petroleum inventories move materially lower. After all, inventory levels are roughly equal to where we started the year. But the signs are there. Should OPEC+ compliance by applied more diligently through Q1, we will likely see the market shift once again into deficit and thus see a period of ongoing inventory draws take place.

Encapsulating this thesis for a rally in oil prices is the current state of positioning in the market. To me, the primary driver of oil prices this year has been the speculators. After reaching their most bullish level of positioning in October, hedge funds and CTA’s have since sold oil futures these past couple of months as aggressively as they bought during August and September. Now, this group of paper traders find themselves equal to their most bearish levels of exposure that we have seen in over a decade.

Such levels of extreme bearishness are rarely followed by further lows in price, and, should the underlying fundamentals within the market continue to trend in a positive direction, there is plenty of scope for significant buying power from both hedge funds and CTAs to drive prices higher.

Of course, what we really need to see in order for any kind of rally to materialise is the front end of the futures term structure shift into backwardation from the current state of contango. Indeed, of all the oil market indicators I monitor, this remains the most bearish. Not only does contango signal the market is not overly tight (at least on the margin), but it also disincentivises inventory drawdowns and makes it more profitable for speculators to sell futures via the negative roll yield. The opposite is generally true in backwardation.

What has been the driving factor in alleviating the tightness in the oil market over recent months have been the continued upside surprise in US production, in addition to other production surprises in areas such as Iran.

Not only is US oil production well-above pre-COVID levels, but it has reached all-time highs while rig counts have been moving lower, thanks largely to private producers boosting consumption. I suspect the growth in production in 2024 will struggle to match that of 2023 (particularly given that private producers look to be boosting production to increase their appeal as acquisition targets).

And, while Saudi Arabia and OPEC+ remain committed to trying to offset the growth in non-OPEC production via the extension of their own cuts through Q1 of next year as well as better enforcement of these cuts, a significant (though low probability) risk facing oil prices is a situation where Saudi opts to reverse their cuts and boost production, which would bring a significant amount of additional supply onto a market that is likely to be fairly balanced for much of next year.

Whether this is caused by OPEC+ dissent, continued upside surprises in US oil production forcing the Saudi’s to try and regain market share or prices appreciating to an acceptable level in which the Saudi’s are happy to open the spigots, this looks to be a significant tail risk facing oil markets that investors should be aware of, though has little bearing for the time being.

For now, the oil market looks to be regaining its footing, and, should we continue to see crack spreads hold firm, refinery demand increase and sustained inventory drawdowns be met with a futures curve shifting into backwardation at a time where speculators are the most bearish oil they have been in years, the recipe for another rally in to the low $90s looks to be a distinct possibility over the coming months. That these bullish developments are unfolding at a time when geopolitical risks for the oil market are again coming to the fore via the continued Houthi attacks in the Red Sea (prompting several tanker companies to suspend travel through the Bab al-Mandab), means the bullish setup for crude oil and energy is looking increasingly attractive.

For energy investors, this looks to be an opportune time to add to long term equity holdings, and for traders to look to hedge upside price risk.

. . .

Thanks for reading!

If you would like to support my work and continue to allow me to do what I love, feel free to buy me a coffee, which you can do here. It would be truly appreciated.

Regardless, feel free to share this with friends and around your network. Any and all exposure goes a long way and is very much appreciated. Thanks again.